Avaan uuden ketjun keskustelulle UB Pohjoismaiset Liikekiinteistöt -rahaston ympärille. Kuluneella viikolla avasimme rahastolle rahastosivun, joka kokoaa vastedes yhteen kvartaalikatsauksia ja muita rahastoon liittyviä sisältöjä, mukaan lukien inderesTV:n säännölliset haastattelut, joista ensimmäinen kuvattiin muutama päivä sitten. Tässä kohtaa on hyvä todeta, että UB Rahastoyhtiö on Inderesin asiakas.

Jatkossa tarkoituksena on kerätä myös täältä kysymyksiä ja ideoita haastatteluihin. Olen kannustanut myös UB:n salkunhoitajia jalkautumaan Foorumille osallistumaan keskusteluun. Omasta puolestani mikään ei estä puimasta myös yleisellä tasolla tässä ketjussa Pohjoismaiden kiinteistömarkkinoita liippaavia kysymyksiä.

Salkunhoitajat kävivät haastattelussa. Sopivaa kuunneltavaa varmasti myös kiinteistösektorista yleisesti kiinnostuneille.

Aiheet kellotettuna

00:00 Aloitus

00:25 Ruotsin asuntomarkkinoiden tyrsky

02:40 Ulkomaiset sijoittajat pitävät kiinni Pohjoismaista

04:20 Pohjoismaissa kiinteistöltä vaaditaan enemmän tuottoa

06:00 Kiinteistökohteiden uudelleenhinnoittelu

08:58 Uutta tietoa saadaan alati lisää

10:27 Inflaation merkitys

13:48 Uusi sijoitus Oslossa

16:53 Käteinen on kuningas

UB:n salkunhoidolta ilmestyi tammi-maaliskuun kvartaalikatsaus. Kiinnostavaa luettavaa myös yleisesti kiinteistömarkkinoista kiinnostuneelle. Kauppaa tehdään merkittävästi vähemmän kuin aiemmin, mutta aivan kohmeessa markkina ei ole.

Moni kiinteistösijoittaja tuntuu käyttävän kaupankäynnistä vapautuneen ajan nykyisten kiinteistöomistusten parantamiseen ja optimointiin. - - Näin ollen monet kiinteistöt tulevat olemaan entistä paremmassa kunnossa markkinan kääntyessä.

Inflaatio on osoittanut ensimmäisiä merkkejä taittumisesta, mikä voisi tarkoittaa koronnostojen loppumista lähitulevaisuudessa. - - koronnostojen loppuminen ja viimeistään korkojen lasku tulee palauttamaan aktiviteetin kiinteistömarkkinaan.

Monella sijoittajalla vaikuttaa olevan edelleen hyvin käteistä käytettäväksi heti, kun talousnäkymät hieman selkenevät. Hyvänä esimerkkinä mainittakoon Blackstone, joka ilmoitti huhtikuussa keränneensä uuteen kiinteistörahastoonsa ennätykselliset 30 miljardia dollaria. Isoilla sijoittajilla näyttää siis löytyvän uskoa kiinteistömarkkinan elpymiseen lähitulevaisuudessa.

Tässä salkunhoitajien uusin haastattelu. Puhuttiin aluksi markkinatilanteesta ja sitten mm. siitä, miksi listattu ja listaamaton kiinteistömarkkina vaikuttavan elävän aivan eri elämää.

UB:n salkunhoitajat tulevat inderesTV:n haastatteluun lähipäivinä. Tässä jo joitakin näkemyksiä sieltä suunnasta kiinteistösektorin tilanteesta ja markkinanäkymistä.

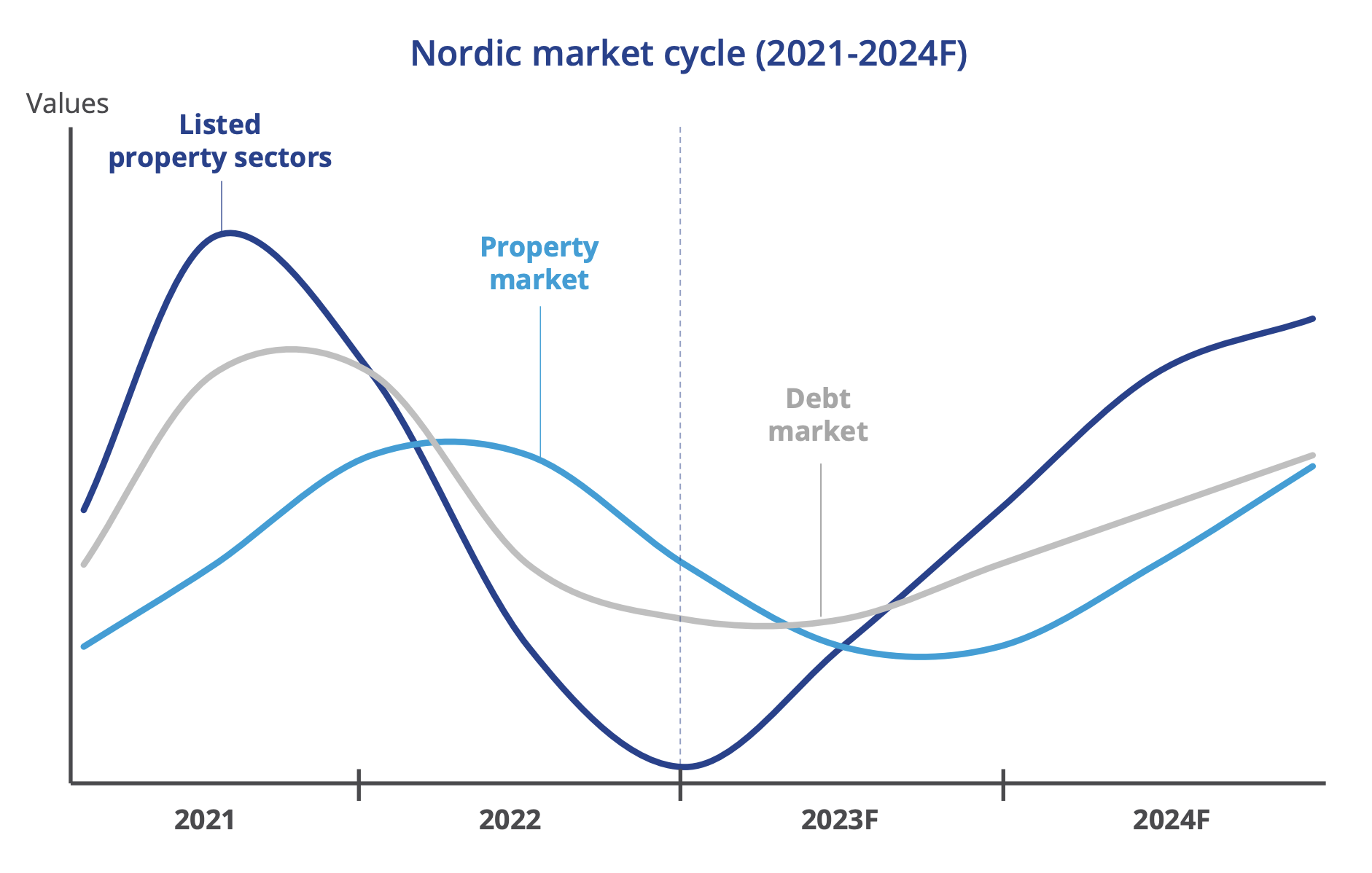

Ensimmäisiä signaaleita kiinteistösijoitusmarkkinan elpymisestä on jo nähty listatussa kiinteistömarkkinassa, joka näyttää saavuttaneen pohjansa lokakuussa 2023. Historiassa suorat kiinteistösijoitukset ovat seuranneet listattua kiinteistömarkkinaa noin 6–12 kuukauden viiveellä.

Tässä luvattu haastattelu. Hyödyllistä kuunneltavaa varmasti kaikille, keitä kiinteistömanagerien ja -sektorin tilanne yleisestikin kiinnostaa.

Kellotukset:

00:00 Aloitus

00:16 Vuosi 2023

01:30 “Sekundääritoimistot kärsivät eniten”

02:24 Listatun markkinan käänne

03:23 Koroista käänteen tekijä

05:38 Tuottovaateet ja arvonlaskut

08:57 Markkinastressi ja lunastukset

10:55 Yield gap ja reaalikorot

12:25 Rahastojen tuottoerot

14:12 Tuotonlaskennan mekaniikka

20:03 Norjan merkitys

22:11 Miten “uusi normaali” on muuttanut kiinteistösijoittamista?

Tässä on UB:n Jaakko Onalin ja Mikko Hentisen tuore katsaus.

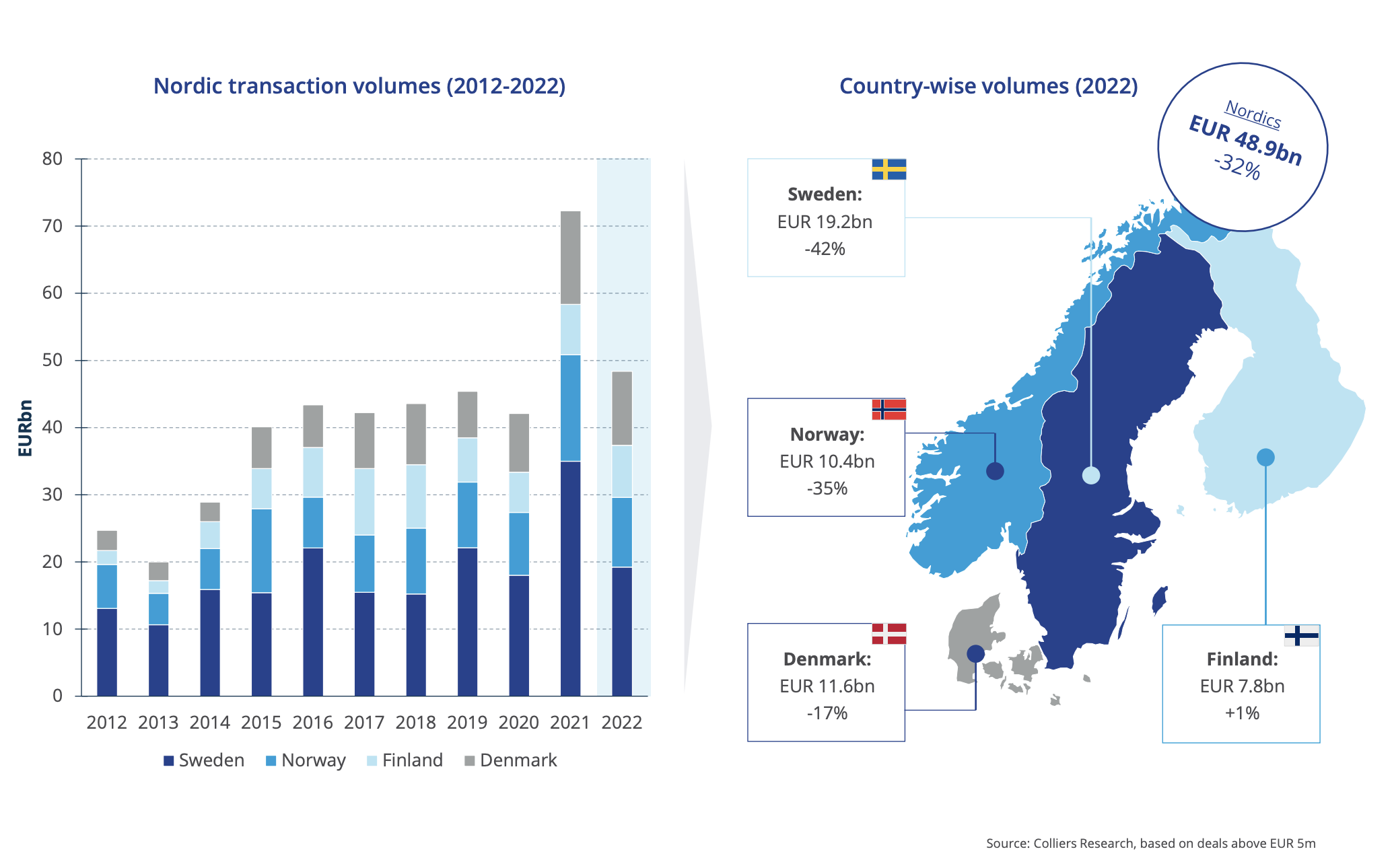

Edellisessä kvartaaliraportissa kirjoitimme, että kiinteistömarkkinan transaktiovolyymi näyttää kvartaalitasolla vakiintuneen 4–5 miljardiin euroon Pohjoismaissa. Monet varmasti toivoivat, että vuoden loppuun olisi kiinteistömarkkinassa saatu pörssitermein “joulupukkiralli”, ja vaikka pientä kiriä nähtiinkin, jäi vuoden 2023 transaktiovolyymi Pohjoismaissa ennustetusti vajaaseen 20 miljardiin euroon. Kyseessä oli hiljaisin vuosi sitten finanssikriisin.

Newsecin kevään 2024 markkinakatsaus Suomen kiinteistömarkkinoihin julkaistiin alkuviikosta. Sen voi ladata täältä. Lataaminen edellyttää yhteystietojen jättämistä. Ellei sitä halua tehdä, voin tarvittaessa laittaa tulemaan sähköpostitse.

Vaikka raportti keskittyy Suomeen, mutta ajurit ovat käytännössä yhteneväiset maasta riippumatta: inflaatio, korot-rahapolitiikka, vaisu taloustilanne ja yleinen epävarmuus. Mitä unohdin luetteloida?

Kiinteistömarkkinoiden odotetaan normalisoituvan ja turbulenssin vähenevän loppuvuotta kohti mentäessä, kunhan inflaatio laskee ja korot seuraavat: "Suurin riski nykyisessä skenaariossa on se, että inflaatio ei suostu laskemaan ‘viimeistä mailia’. Tämä voi johtua geopoliittisten häiriöiden aiheuttamista uusista tarjonnan häiriöistä. Inflaatio voi kieltäytyä laskemasta myös siksi, että talouskasvu on odotettua voimakkaampaa ja palkankorotukset ennakoitua suurempia.

Markkinassa on Newsecin mukaan aiempaa enemmän potentiaalisia ostajia. Ostohalukkuus ei kuitenkaan takaa transaktioaktiviteetin nousua. Kaikki odottavat korkojen laskua.

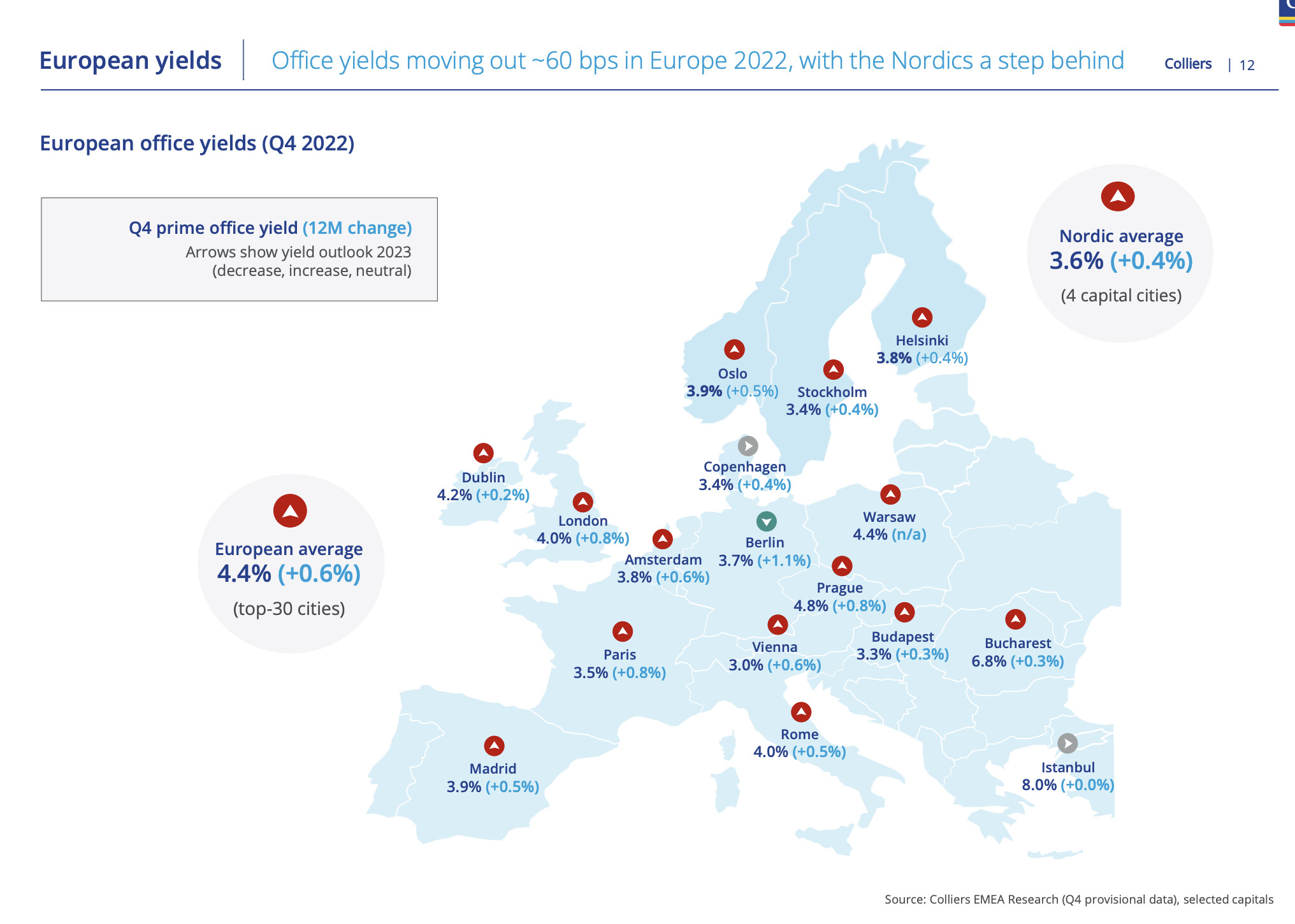

Toisaalta: “Vaikka prime-tuottovaatimukset ovat kuluvan syklin aikana nousseet 70-170 peruspistettä, nousu on silti pienempi kuin Suomen valtion joukkolainan tuoton 320 peruspisteen nousu” – “kiinteistömarkkinoiden epävarmuuksien vuoksi on epäselvää, riittääkö nykyinen kaventunut riskipreemio markkinan elvyttämiseen.”

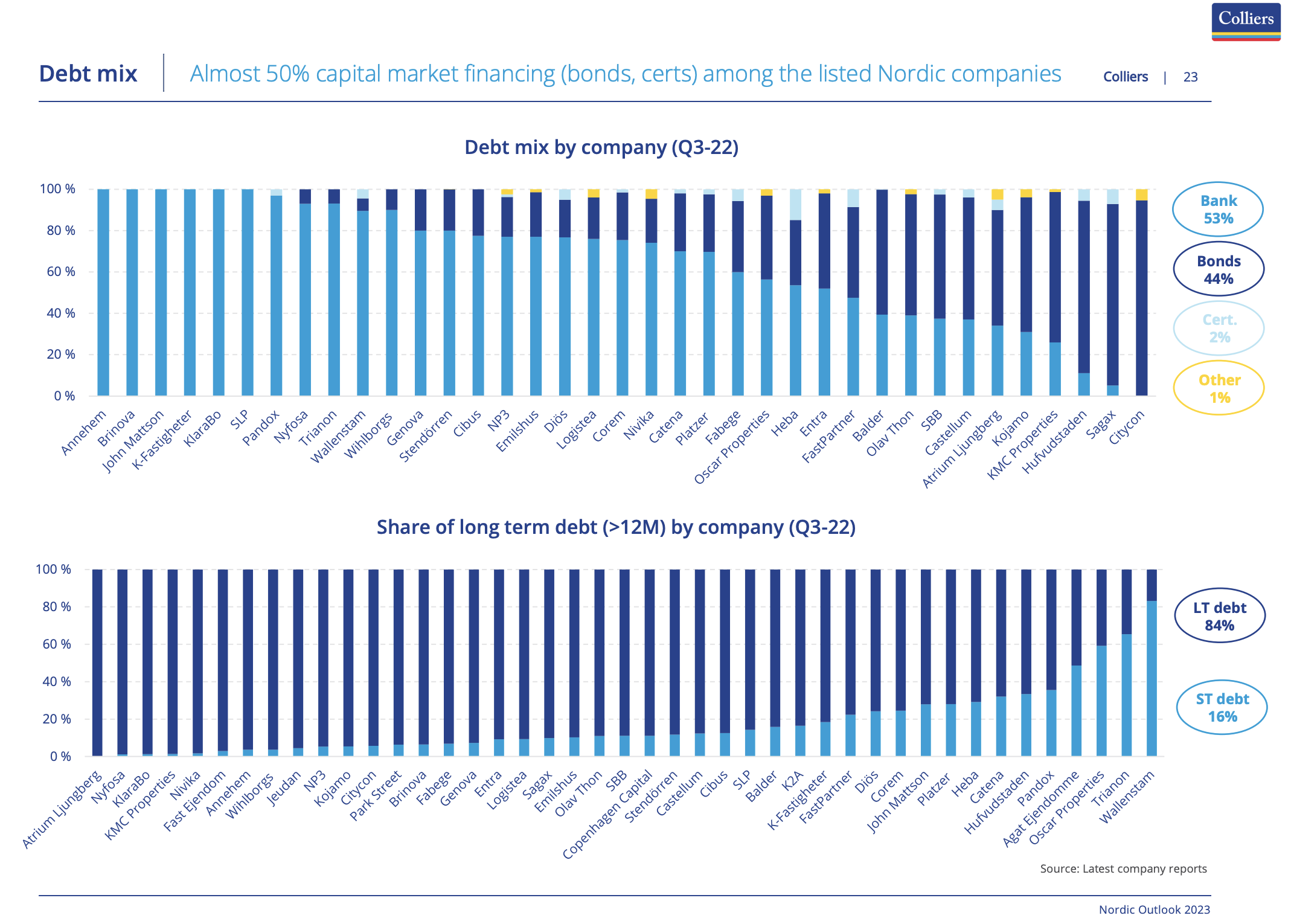

Muutama hyödyllinen graafi raportista poimittuna. Kiinteistöluokittain (asunnot, toimistot, teollisuus ja logistiikka, liiketilat, yhteiskuntakiinteistöt, hotellit) raportissa on erikseen omat osiot.

Tässä on mielenkiintoinen kirjoitus UB:N Jaakko Onalilta ja Mikko Hentiseltä.

Kirjoitimme vuoden alussa julkaistussa Q4/2023-kvartaaliraportissa, että kiinteistöjen arvot löytänevät uuden tasapainon kuluvan vuoden aikana. Tarkasteltaessa muutoksia kiinteistöjemme arvoissa vuoden ensimmäisellä kvartaalilla huomaamme, että suurimmat arvonlaskut näyttäisivät olevan näillä näkymin takanapäin. Kiinteistöarvioitsijat saavat toivottavasti kuluvan vuoden aikana lisää transaktioiden tuomaa näyttöä kiinteistöjen arvoista, joten pienempiä säätöjä kiinteistöjen arvoihin varmasti vielä tehdään toteutuneiden transaktioiden perusteella.

UB:n salkunhoitajat Jaakko Onali ja Mikko Hentinen olivat @Antti_Jarvenpaa:n haastattelussa.

Aiheet:

00:00 Aloitus

00:22 Markkinatilanne

05:50 Kaikki ei ole kiinni koroista

11:25 Ongelmat keskittyvät toimistoihin

15:19 Pääomien allokointi keskittyy uudelleenallokointiin

19:52 Kohteiden kehitys korostuu aiempaa enemmän

23:37 Arvonmuutokset edelleen maltillisia

27:27 Loppuvuoden näkymät

Alla on UB:n salkunhoitajien Jaakko Onalin ja Mikko Hentisen rahastokatsaus.

Rahaston edellisissä kvartaalikatsauksissa ja materiaaleissa olemme näyttäneet kansainvälisten konsulttitalojen graafia, jonka mukaan suoran kiinteistömarkkinan käänne tulisi tapahtumaan kuluvan kesän aikana. Euroopan keskuspankin, EKP:n, kesäkuussa tekemä ensimmäinen koronlasku tuleekin todennäköisesti helpottamaan kiinteistöjen arvojen määritystä ja siten tuottojen ennustamista. Jatkossa koronlaskujen vaikutus kiinteistöjen arvoihin voikin olla jo varovaisen positiivinen. Kiinteistömarkkinassa vaikutukset näkyvät hitaiden transaktioprosessien vuoksi verkkaisesti, joten olemme tällä saralla viisaampia todennäköisesti vasta syksyllä.

UB:n salkunhoitajan Jaakko Onali oli Antin haastateltavana.

Aiheet:

00:00 Aloitus

01:34 Kaupankäynti vilkastumaan päin

02:36 Ruotsi näyttää suuntaa, Suomi seuraa perässä

03:25 Markkina-ajurit ja suosituimmat kiinteistöluokat

06:35 Toimistomarkkinan haasteet painottuvat Suomeen

08:18 “Vuosikymmenen parhaat ostopaikat”

14:05 Onko vastuullisuus viherpesua?

17:12 Kiinteistöjen kehitys

19:02 Strategisesti tärkeät kiiinteistösijainnit

21:42 Vuokrausasteessa varaa parantaa

23:45 Lunastukset ja nettomerkinnät

Antin tentissä oli UB:n salkunhoitaja Jaakko Onali.

Useiden asunto- ja kiinteistörahastojen päätökset keskeyttää rahasto-osuuksien lunastukset ovat herättäneet alkuvuonna runsaasti keskustelua markkinoilla. Mikä tilanteeseen on johtanut? UB:n salkunhoitaja Jaakko Onali avaa kiinteistörahastojen ja -markkinan tilannetta.

Aiheet:

00:00 Aloitus

00:40 “Likviditeetti on todella heikko”

04:40 Ongelmat keskittyvät Suomeen

05:37 Asuntomarkkinat

06:45 Miksei osuudenomistajat saa rahojaan?

09:46 Ovatko avoimet kiinteistörahastot todella “likvidejä”?

11:53 Kuka tai ketkä määrittelevät osuudenomistajien edut?

12:35 Voisiko lunastuksia rahoittaa velkarahalla?

14:39 Millaiset käteispainot ovat tyypillisiä kiinteistörahastoille?

16:03 Miksi kohteita ei pakkomyydä, ja mitä siitä seuraisi?

19:27 Kiinteistöjen arvonmääritys ja päämies–agentti-ongelma (intressiristiriita)

22:30 Miten seurata ja arvioida kiinteistömarkkinaa ja -rahastoja?

24:03 UB Pohjoismaiset Liikekiinteistöt -rahaston tilanne

26:08 Markkinatilanne Pohjoismaissa maittain

28:30 Miksi rakennusmarkkinan hyytyminen ei ole tukenut vanhaa kiinteistökantaa?

30:35 Pitkät korot, inflaatio ja reaalikorko

32:40 Odotukset vuodelle 2025