Based on the December future, that is indeed possible. Not with the August future. But a couple of questions arise:

- How does Nordea justify linking to the December contract, when the August contract is much more liquid, at least based on today’s volume, and according to the prospectus, the contract should be linked to the nearest liquid future. The August future’s volume is almost five times higher even today. And before July 8th, the December future’s volume was negligible, a few thousand contracts per day, which is a few percent of the August future’s typical daily volume during June and July.

- How can a casual investor even find out which future the price is currently linked to?

- Is it in accordance with investor protection that the information is not explicitly presented anywhere, and that an investor cannot easily see a reference price anywhere on which the product’s expiry is based?

- Is it in accordance with investor protection that Nordnet markets products by directly referring to the spot price, which gives a false impression of the underlying asset’s spread relative to the knock-out price?

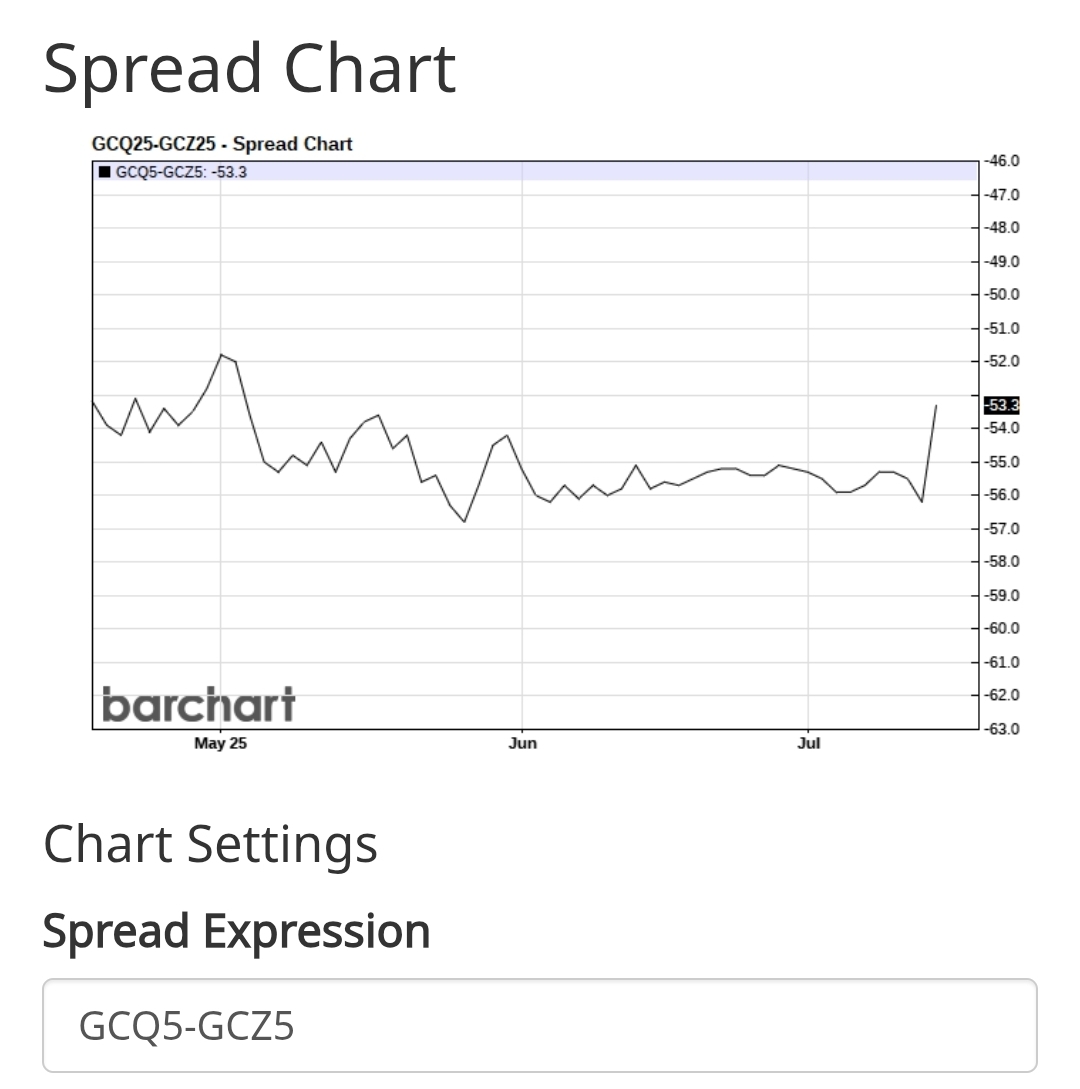

Furthermore, if this is based on the December future, the product should have been knocked out already on July 3rd, when the financing level was also lower and the price reached over 3430.

In principle, it would be possible that a rollover to later futures has occurred in the interim, which changes the financing level, but shouldn’t that have only raised the stop loss by the amount of the futures spread? According to the prospectus, rollover can occur:

"Any day from and including the fifth Scheduled Trading Day in the month prior to expiration of the relevant futures contract."

So, presumably, the contract could have been linked to the August future until at least the 5th, and then rolled over to December. The volumes for December futures are at zero until the 8th, so the transfer likely happened between the 8th and 11th.

However, the financing level does not support this. The original financing level was 3390. If we assume an average gold price of 3300, the daily margin accumulated between 26.6-8.7 is (3300*(1+0.03/365)^13-3300) = ~3.5 USD. On top of that comes the futures spread, which has been over 50 USD all along. Thus, the financing level should be over 3440 after the rollover.