The story continues: Telia Company signs MoU to divest Latvian operations

Less than 4% of revenue and over 7% of EBITDA came from Latvia. Hopefully the price is right, as it was in Denmark.

Telia’s strategy used to be to be an operator in the Nordics and Baltics, or something to that effect. Now the strategy states that Telia operates in markets where it is number one or a clear challenger right behind in second place. Perhaps even the Finnish operations will be sold if the three-letter competitor starts to pull ahead…

One can only hope that these divestments will eventually lead to a smaller but more agile and developing Telia, so that earnings can also eventually grow.

2 Likes

Also some discussions regarding Valokuitunen (Telia 40%).

7 Likes

Telia acquiring Swedish company Bredband2, price approx. €275 million. Premium to yesterday’s share price 34.9%

3 Likes

Regarding Q2

5 Likes

And here are Joni’s comments.

Telia’s Q2 report was broadly in line with our expectations. Comparable revenue grew, but was slightly below our expectations. Earnings grew clearly driven by cost savings, which was in line with our forecasts. However, the focus today is on the corporate transactions announced by the company yesterday evening and this morning. The company, as expected, reiterated its guidance for 2025, which anticipates good earnings growth.

4 Likes

Without delving deeper into the matter, Telia’s interest in these fiber optic companies is a bit puzzling. This Bredband2 is an open network, which means, as I understand it, Telia’s business would be to maintain and build a fiber optic network whose users can get an actual connection from other operators besides Telia. Recently, Telia divested its “Tower” business, and now, in its place, it’s acquiring highly competitive fiber optic networks.

Perhaps the acquisition of fiber networks is related to the development of the security situation in recent years. Telia’s largest owner, the Swedish state, may well have an interest in increasing its ownership/control in Swedish telecommunications networks, and this can be achieved by buying such networks with the money that is freed up when they withdraw from markets where their market share is small.

That “open network” is a bit misleading, because in this case, the network is still owned by Telia, which leases it to other service providers. These providers, in turn, pay Telia rent for using the network if they get a customer to take their subscription.

So, in practice, because of this rent, the prices of other service providers rise to such an extent that, from the customer’s perspective, the subscription is likely cheapest to get from Telia in the end.

3 Likes

Here is Joni’s drafted company report on Telia right after its Q2 report. ![]()

We raise Telia’s share target price to SEK 35.0 (previously SEK 34.0) reflecting forecast changes and reiterate our ‘reduce’ recommendation for the stock. Telia’s Q2 report was overall relatively well in line with our expectations. However, the focus was on the recent M&A news. We forecast the company to grow exactly in line with guidance, which is a good level compared to historical performance. The stock’s valuation (2025e P/E and EV/EBIT 16x and 15x) remains neutral, considering the already stretched earnings growth expectations.

5 Likes

Here are Joni Grönqvist’s comments from Telia’s pre-quiet period analyst call. ![]()

Telia organized an analyst call before the quiet period began. During the analyst call, the company went through group-level and geographical observations. In the big picture, Q3 will, as previously communicated, have slower earnings growth than the full year (5%). Market-wise, there were no major changes in trends compared to before. Below are observations related to Q3.

5 Likes

Here are Joni’s pre-report thoughts as Telia releases its Q3 report on Thursday. ![]()

We estimate revenue to have grown slightly and profitability to have improved, driven by cost savings. Combined, we expect slightly slower earnings growth for Q3 compared to the full year. For the full year, we forecast the company’s operational performance to be at the very low end of its guidance. Additionally, we will be monitoring comments on how earnings growth could be maintained at a brisk pace next year as well, when the effects of the extensive cost-saving program diminish.

1 Like

Here are @Joni_Gronqvist’s quick comments on Telia’s Q3 results. ![]()

Telia’s Q3 report was in line with our expectations in terms of figures. Comparable revenue grew but was slightly below our forecasts. Earnings grew driven by cost savings, which was in line with our forecasts, but geographically there were significant differences. The company slightly raised its cash flow guidance for 2025, driven by lower investments.

3 Likes

Here is a fresh company report from Joni on Telia after Q3. ![]()

We reiterate our target price of SEK 35.0 and a Reduce recommendation for Telia’s share. Telia’s Q3 figures were in line with our expectations. A positive surprise was the slight increase in cash flow guidance. However, the big picture challenge in the coming years remains how to maintain good earnings growth once the effects of the extensive cost-saving program diminish. The share’s valuation (2025e P/E and EV/EBIT 17x and 15x) remains neutral, considering the challenging earnings growth in the coming years.

Bank of America raised Telia’s target price to 46 SEK. Finally, things are happening.

7 Likes

Here are Joni’s comments from the Telia analyst call. ![]()

Telia held an analyst call before the start of the silent period. During the call, the company reviewed group-level and geographical observations. In the big picture, Q4 earnings growth will be at the level of Q3, as previously communicated, meaning slightly slower than the full year (5%). There were no major changes by market; Sweden and the Baltics have performed well, while Norway and Finland have been weaker. Below are observations related to Q4.

3 Likes

Goldman Sachs raised Telia’s recommendation.

Goldman Sachs raises target price for Telia to 50 kronor (47), reiterates buy - BN | Placera.se

3 Likes

Elisa reduced its workforce by about 400 people around Christmas, and it seems Telia has similar plans this spring:

”Telia Finland continues to build a simpler and more efficient organization. The company is initiating change negotiations that may lead to the reduction of approximately 200 roles in Telia’s Finnish operations.”

So, this news only concerns the Finnish operations, but even 200 roles can have a small visible EBITDA impact at the group level.

Here are Joni’s preview comments as Telia reports its results on Thursday. ![]()

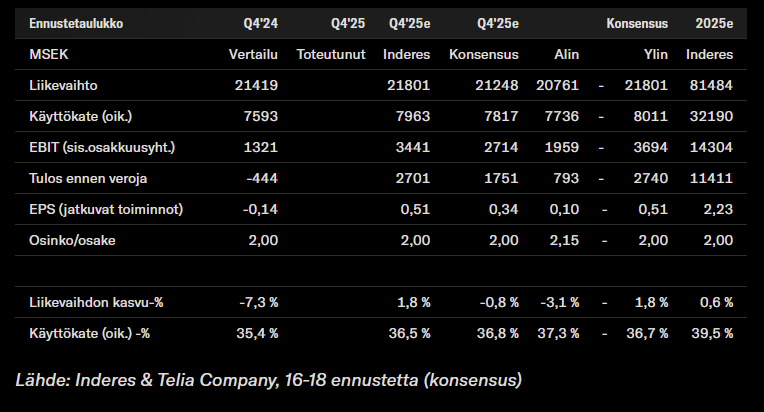

We forecast that revenue grew slightly and profitability improved, driven by cost savings. Combined, we expect earnings growth to be at the Q3 level in line with previous communications, meaning slightly slower than for the full year (5%). Like the consensus, we expect earnings growth to slow down in 2026 as the impact of major cost savings fades. Thus, we are following comments on how earnings growth could be kept brisk this year as well. Additionally, we expect the company to guide cash flow to be at a level of at least 8 billion, which is the minimum required level for returning to a sustainable dividend distribution base.

1 Like

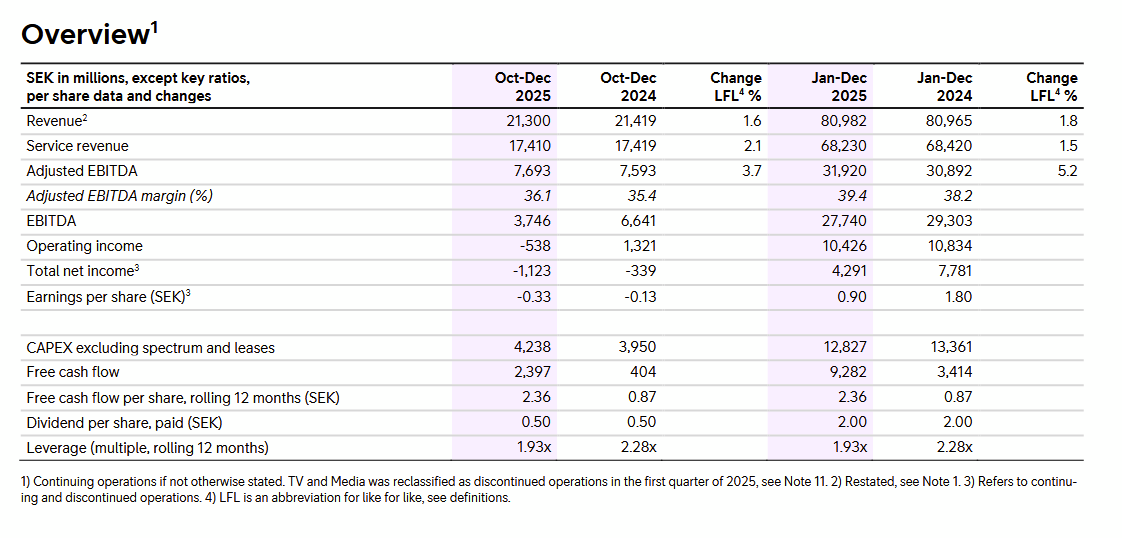

Results are out:

vs expectations (per Inderes). A bit sluggish, and revenue, adj EBITDA, and EPS were below consensus.

No rocket-like growth is guided, and the dividend is being hiked cautiously.

Outlook 2026: Service revenue growth, like for like, around 2%, adjusted EBITDA growth, like for like, around 3%, CAPEX excluding spectrum and leases below SEK 13 billion and free cash flow around SEK 9 billion.

- For 2025, the Board of Directors proposes to the Annual General Meeting a dividend of SEK 2.05 per share (2.00).

5 Likes

Here are Joni’s quick comments on Telia’s results. ![]()

Telia’s Q4 report was slightly softer than our expectations in terms of figures, but the guidance was better than expected. Comparable revenue grew but fell slightly short of our forecasts. Earnings grew driven by cost savings, but earnings growth nevertheless slowed more than we expected. Cash flow was good in Q4 and throughout 2025, on the back of which the company proposed a dividend increase for the first time in a long while. The company’s operational guidance for 2026 was above our and consensus expectations. We are thus monitoring what gives confidence in the growth trajectory in line with the guidance. Additionally, the cash flow guidance for 2026 is positive and clearly covers the dividend.

4 Likes