Creating a thread and company page for this IPO company.

Tamtron is one of the world’s leading providers of weighing solutions. Our product and service selection is among the widest on the market. Tamtron offers innovative weighing solutions, their lifecycle services, and modern cloud-based weighing data management solutions for the needs of several industries. Reliable, accurate, and intelligent weighing solutions facilitate and enhance customers’ daily operations in earthmoving, recycling, energy, forest, process, and manufacturing industries, as well as in logistics and ports. With Tamtron’s solutions, weighing data can be utilized in all company operations.

Welcome to follow Tamtron’s virtual press conference today, October 28, 2022, starting at 10:00 AM from the following link: Info (the press conference will be held in Finnish).

It doesn’t matter, based on last year’s results, a pretty nice slope can be drawn for the curves in the IPO material

The industry seems fairly stable, so where did last year’s improved result come from?

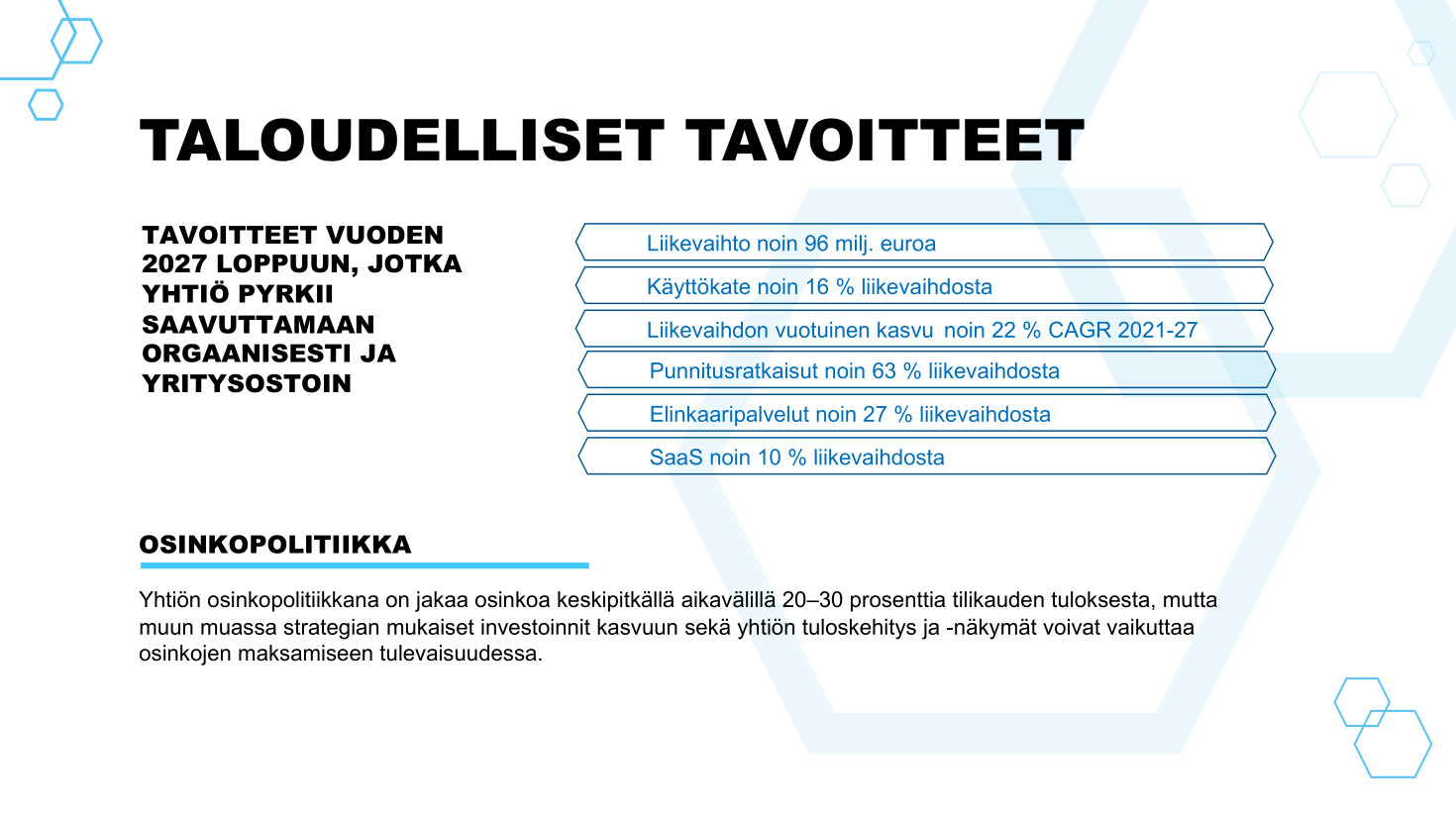

In accordance with the company’s strategy, Tamtron aims to more than triple its net sales by the end of 2027 compared to 2021 net sales. The company estimates that a significant portion of the net sales growth will come from acquisitions.

It’s worth considering which figures you are looking at. I’m guessing these are the parent company’s figures? The company’s release contains the most recent figures. (Edit: it seems that 1) the audit reference is now adding ones after those figures in that release…).

Tamtron has good products. Tamtron’s loader scales can be seen, for example, in timber trucks or John Deere (John Deeren) manufactured forest machines. Tamtron’s international sales share is also high, at 71 percent of revenue in 2021.

Perhaps it is worth looking at the company’s history first. There you will find a quite interesting development. Throughout its history, Tamtron has sought growth, but it has not always materialized.

In 2001:

Just over 20 years ago, Tamtron’s management was interviewed in Taloussanomat. In the newspaper article, the company’s management saw the long-term growth platform as being in export markets. At that time, exports already went to a total of 40 countries. In Finland, competition in the sector was reported to be tough. Under its new owner, the company had grown quite rapidly in 8 years. In 1993, Tamtron’s revenue was 6.7 million Finnish marks.

In October 2001, Tecnomen Oyj and Tamtron Oy made a deal in which the entire share capital of Tecnomen System Solutions Oy, which produces data collection, time tracking, and access control systems, was transferred to the newly established Tamtron Solution Oy.

As a result of the deal, the Tamtron group’s revenue rose to approximately 100 million Finnish marks in 2001. → Tecnomen sells its subsidiary to Tamtron

In 2011:

10 years later, Talouselämä reported that Intera had invested in Tamtron. Tamtron now had exports to 50 countries and a revenue of 25 million euros. According to the newspaper article, the company had a strong market position in some Eastern European countries. The interview stated that Intera’s involvement would ensure continued growth. The company’s goal was a revenue of 50-60 million euros in five years.

According to Intera Partners’ own acquisition announcement, it bought a majority stake in Tamtron in 2011. The announcement stated that "the conditions for accelerating international growth are excellent”.

→ Intera Partners - Etusivu

For some reason, Tamtron’s growth fell short of its targets. Revenue did not rise from 25 million euros to the targeted 50-60 million under Intera’s leadership. Growth did not materialize, and Intera sold its shares to Aito Capital Oy in 2017. → Intera Partners - Etusivu

During Intera’s tenure, Tamtron did, however, make acquisitions. In 2013, it acquired the German scale service company D+G. In recent years, Tamtron has also made acquisitions of small companies specializing in the resale, installation, calibration, and maintenance services of weighing solutions. In 2021, the acquisition target was the Norwegian ScaleIT, and last year, the Danish Jydsk Vægtfabrik A/S was acquired.

As mentioned in previous newspaper articles, competition in the industry is tough both in Finland and abroad. There are many players in the market. This is also indicated by Tamtron’s statement that it aims to complete 1-2 acquisitions each year in addition to organic growth.

Tamtron’s Weighing-as-a-Service has competitors. For example, Lahti Precision Oy (https://lahtiprecision.com/) has a range of weighing equipment for various industries and a digital weighing service, mScales.

It will be interesting to see how Tamtron describes the markets and competition in its upcoming IPO prospectus. The company will probably position itself in Northern Europe, as many large companies are competing in Central Europe, such as Intercomp (www.intercompcompany.com/), Pfreundt (Pfreundt - Products) and the Coop Bilanciai (Coop Bilanciai) group (Coop Bilanciai: weighing systems, scales, and industrial scales). In North America, there are its own large companies such as Mettler-Toledo (ticker MTD), Avery Weigh-Tronix, owned by Illinois Tool Works (ticker ITW), Fairbanks Scales Inc (Fairbanks Scales Inc), and Rice Lake Weighing Systems (Rice Lake Weighing Systems).

Another scam IPO where the numbers have been cooked to look good, and then after a year on the stock exchange, things return to normal and the stock drops 70%, just like other listed companies.

There hasn’t been a bulletin about the start of Tamtron’s IPO yet. Hopefully, investor research will also be available for reading in connection with the listing.

Tamtron’s anchor investors have committed to subscribing for 66.80 percent of the shares offered in the IPO, so they seem to have confidence. Also, Tamtron’s current owners are not selling the company’s shares in the IPO according to the announcement.

Tamtron’s product portfolio is quite broad, so it’s difficult to get a more precise understanding of their market position. It likely varies by scale type.

Perhaps one interesting case example of Tamtron’s offering could be the One Timber crane scale. This product is unlikely to be the most central driver for the company, but it can be a successful product in its own segment.

Here is a brief summary of the product in question based on various sources.

Crane scales

Wood procurement development company Metsäteho Oy published a comparison of crane scales on the market a good 10 years ago. Metsäteho’s owners include a group of forest companies, sawmills, and Metsähallitus (the Finnish state forest management body). Metsäteho aims to support the development of its shareholders’ wood procurement through research.

→ 3 crane scales based on hydraulic pressure sensors: (Tamtron TBS200, LoadMaster, and Komatsu)

→ 4 crane scales based on strain gauge sensors (Intermercato, Epec, Ponsse’s LoadOptimizer, and John Deere’s Timbermatic manufactured by Tamtron)

Tamtron manufactured the scale based on a strain gauge sensor for John Deere, and their own scale was based on a hydraulic pressure sensor. More detailed information on the TBS200 scale can be found here. Even here, the weighing accuracy declared by the manufacturer is marked as ±0.25–2.0%. → https://puuhuolto.fi/mittaus-ja-laatu/wp-content/uploads/sites/9/TamtronTBS200.pdf

Tamtron acquires LoadMaster scales (2010)

In 2010, Tamtron made an acquisition by buying a Swedish company that manufactures LoadMaster 2000 crane scales. According to Tamtron’s website, Loadmaster scales were the predecessors of Tamtron Timber and the current intelligent ONE Timber scales. → Tamtron Ruotsi - mobiilipunnituksen edelläkävijä | Tamtron

→ So, Tamtron’s current crane scale is not entirely based on the company’s own product development, but the foundation came to the company through an acquisition.

Need for more accurate measurement

From the table above, it can be noted that the weighing accuracy of crane scales varied between ±0.25–4.0%. From the perspective of forest companies, there was room for improvement in weighing accuracy. More accurate measurement was needed because:

Crane scale measurement replaced pile measurement. During harvesting, both industrial and energy wood are harvested simultaneously, which increases crane scale measurement.

The costs of timber road transport increased. This forces the optimization of loads to utilize transport capacity efficiently. More details on costs can be found in, for example, the Timber harvesting and long-distance transport annual statistics.

This development has led to the fact that nowadays, a crane scale can be found in most timber trucks. The number of crane scales installed on forwarders also seems to be on the rise.

Tamtron One Timber (2020)

Tamtron launched the new Tamtron One Timber crane scale in 2020

Scale based on strain gauge sensors, accompanied by the Tamtron One touchscreen display

Weighing data is transferred wirelessly from the scale to the display and the OneCloud cloud service

Measurement accuracy: According to the introductory video published by Tamtron, the weighing accuracy of the new One Timber crane scale has been ± 0.25–1.0% or even better in test sites.

In addition to measurement accuracy, a scale based on a strain gauge sensor has other advantages compared to a hydraulic scale.

I will highlight a couple of related theses from Tampere University of Applied Sciences as information sources. Both theses were done for Tamtron Group Oy, which acted as the client for the theses.

The thesis lists shortcomings of Tamtron’s previous hydraulic scale, which included:

The hydraulic scale is slightly non-linear, causing discrepancies when weighing logs or pulpwood

The hydraulic scale requires more maintenance and adjustment. Oil must be added to the link as needed, and clearance must be adjusted according to seasons and temperatures

A scale based on a hydraulic link is challenging to type-approve for commercial use. The weaknesses of the hydraulic scale occur precisely at the points tested in type-approval tests

The maximum capacity for the link body was dimensioned at 10,000 kg because that is the maximum weight Tamtron’s test bench can reach. More detailed information on the testing of Tamtron’s weighing sensors can be found in the following thesis.

According to the thesis, Tamtron noticed that there were deficiencies in the practical testing of crane scales.

Tamtron uses five different test platforms.

There was a desire to develop a new type of forest machine scale for the market because operational measurements showed a need for a new product and existing products on the market had shortcomings.

Crane scale market size

Tamtron likely has sales at least to other Nordic countries, but let’s consider the market size of the product in Finland. Today, crane scales are found in almost all timber trucks and also in most forwarders.

There are roughly about 1,600 timber trucks in Finland. The truck fleet has remained around 1,550 trucks over the last decade. With the exception of 2019, the number of trucks has been 1,550 +/- 20 cars. → Metsätrans-Lehti Oy

First registrations of forwarders vary more, perhaps between 150-250 annually. Metsätrans-Lehti Oy

From this, one could estimate that about 300-450 timber trucks and forwarders are registered for the first time in Finland annually. Most of them also acquire a crane scale.

Tamtron also sells One Timber update packages, which include the One display and the necessary sensors. The range includes update packages for hose-type hydraulic links as well as wireless hydraulic links. → Hvordan implementerer man en effektiv og nøjagtig Big bag-station? | Tamtron new model has been on the market for a relatively short time. At least in terms of measurement accuracy, the scale appears promising. User experiences also seem to be positive. This link leads to a video published by Tamtron, which briefly covers user experiences with the scale. → https://www.youtube.com/watch?v=fULC9Tk1Cvg

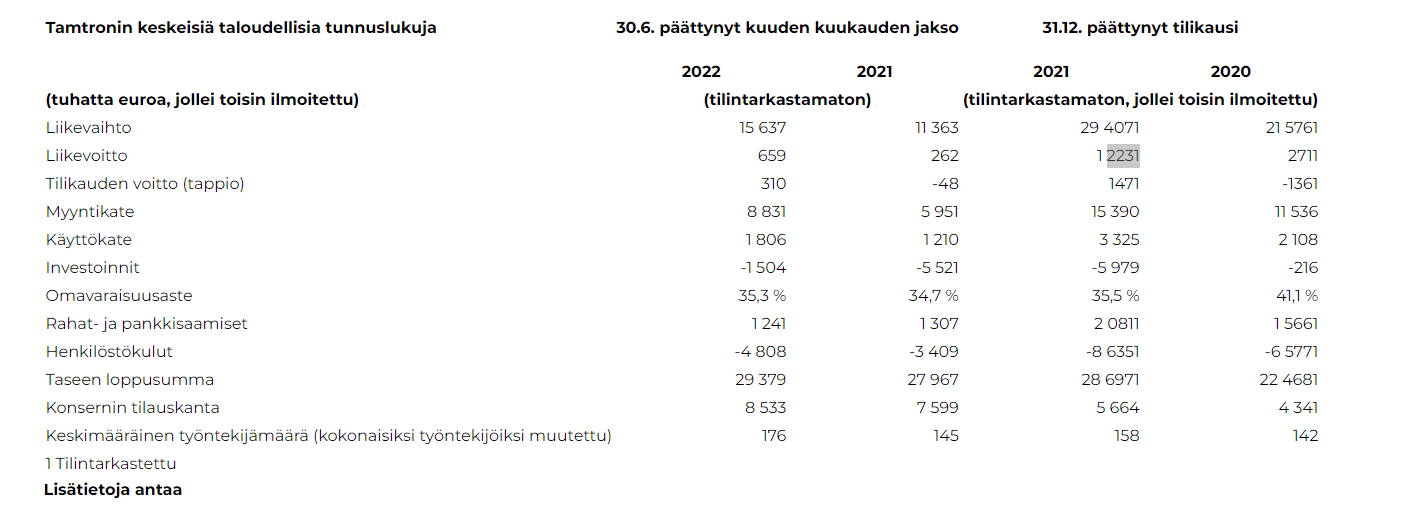

It’s listing in a challenging market situation. However, the company forecasts reasonably good growth (+23%) for the 2022 financial year, and the operating profit is developing in the right direction (EBITDA 13%). For fiscal year 2023, revenue growth seems to remain a bit sluggish (CAGR percentage 14-19% for 2021-2023), but the operating profit continues to improve. Pricing based on 2022 figures is about P/B <1.2. Contrafun also brought up the history and some risks (realization of growth, etc.).

The anchor investor(s) are investing quite significantly, and there are no share sales.

The offering is arranged by Translink Corporate Finance, which at least for me, gives a stamp of quality to the offering and is one factor in deciding whether to participate or not.

There’s very little buzz around the offering. I haven’t looked into it in detail, but it seems like an interesting and sufficiently specific market. Could this be a boring but reliable investment outside of all the hype?

Yesterday, Tamtron held a company presentation event.

Here’s a direct link to the recording of the company presentation event:

Here are some brief highlights from Tamtron’s IPO content, based on both the company presentation event and the listing prospectus. This is primarily a shortened table of contents from the prospectus.

Tamtron aims to raise approximately 9.7 million euros in net proceeds from the IPO (p. 7).

Tamtron expects to incur costs of no more than approximately 0.8 million euros in connection with the offering (p. 6).

The funds raised from the IPO are intended to support the company’s organic and inorganic business growth and internationalization, as well as to repay certain shareholder and other loans, to invest in product development and the development and commercialization of new technologies, and to build production capacity and marketing channels (p. 7).

Financial Targets

Tamtron aims to more than triple its revenue by the end of 2027.

Target: SaaS solution share of 10 percent of the Company’s revenue (9.6 million euros)

96 million euros in revenue by the end of 2027, of which 44 million euros will be achieved through acquisitions.

The financial targets were presented on page 19 of the company presentation event:

Tamtron’s Earnings Forecast 2022 and 2023 (p. 35)

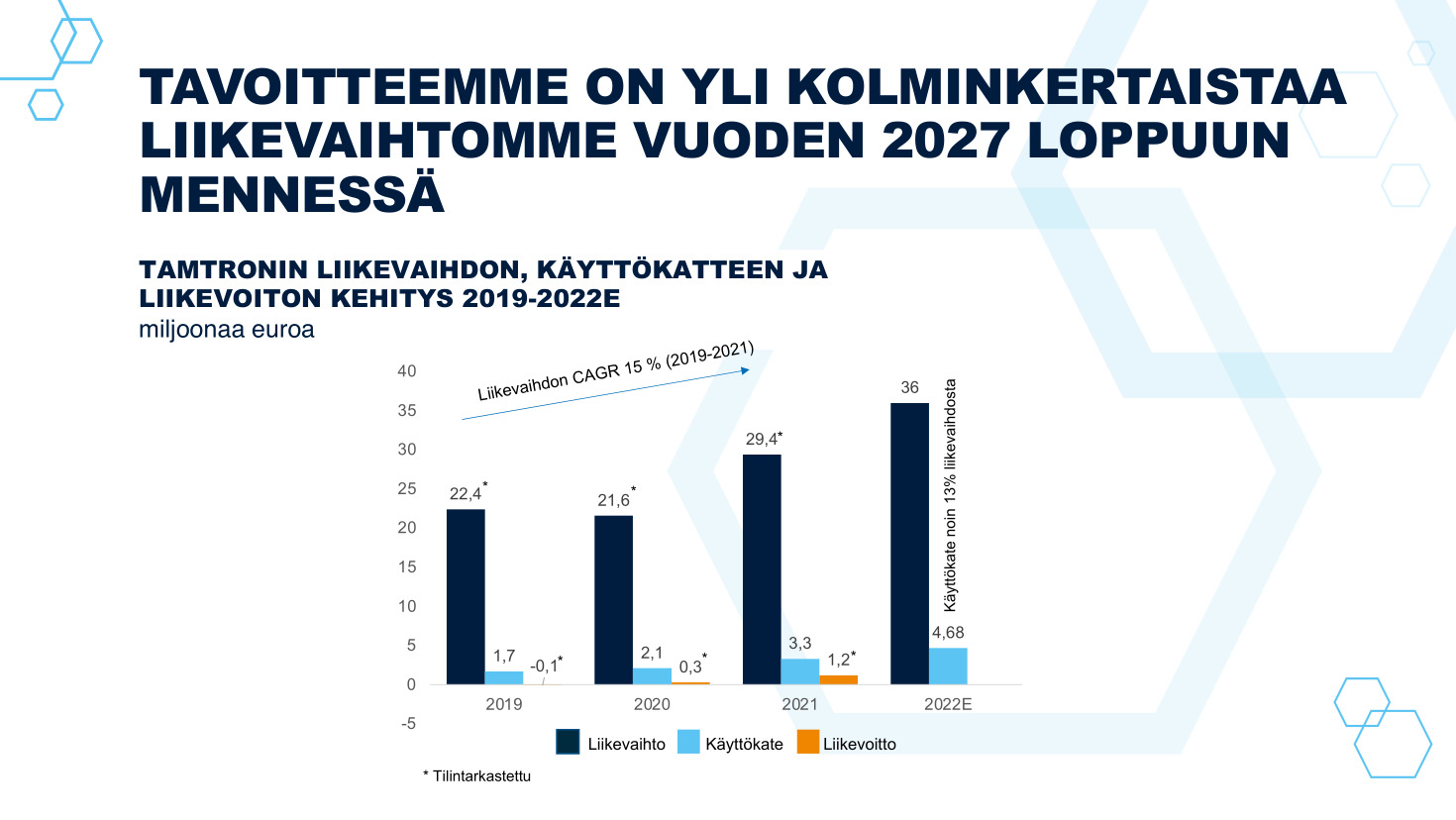

For the fiscal year 2022, revenue is approximately 36 million euros and EBITDA approximately 13% of revenue.

→ EBITDA of 4.68 million euros

For the fiscal year 2023, revenue is 38–42 million euros and EBITDA 14-15% of revenue.

→ EBITDA is estimated to be 5.3–6.3 million euros

By 2027, the target is 96 million euros in revenue and EBITDA of approximately 16% of revenue.

→ Thus, EBITDA in 2027 would be approximately 15.4 million euros

– Tamtron achieved an average annual growth of 15 percent between 2019-2021. Tamtron aims to achieve an average annual growth (CAGR) of approximately 22 percent between 2021-2027. I refer to page 14 of the company presentation event here:

Revenue Distribution (from page 32 of the prospectus) Revenue by business area:

Mobile equipment scales 29%

Heavy equipment scales 27%

Lifecycle services 31%

SaaS services 5%

Resale of scales 8%

Revenue by country:

Finland 29%

International sales 71%, of which

other European Union countries 53%

rest of the world 18%

Subscription Commitments

The minimum subscription in the public offering is 100 shares (6.28 x 100 = 628 euros) and the maximum subscription is 15,923 shares (99,996 euros) (p. 74). In the institutional offering, the minimum subscription is at least 15,924 shares (p. 77). Nordnet serves as the subscription venue for the offering.

According to the company presentation, at least 840,000 euros (8%) has been allocated to the public offering. This means the public offering would be fully subscribed if 1337 individuals made the minimum subscription in the public offering.

→ (840,000 € / 628 € = 1337)

Number of Conversion Shares

Tamtron has a total of approximately 6.3 million euros in shareholder loans raised from shareholders (p. 89).

Tamtron’s main financier has granted the company a 2.5 million euro bond loan, which the company will use to repay shareholder loans, purchase price debt, and Olsen’s receivables.

Scaleit AS CEO Olsen is selling his minority stake in the company, and the purchase price will be paid partly in shares. In Olsen’s conversion, Olsen will be issued 75,276 conversion shares (1.17% of the shares).

Part of Asikainen’s and Keskinen’s shareholder loans will be converted into shares upon completion of the IPO.

Other shareholders’ loans will be repaid (p. 89). The same subscription price as in the public offering, i.e., 6.28 euros per share, will be used in the shareholder loan conversion:

→ Thus, conversion creditors will be issued at least 239,854 shares (3.72% of the number of shares after the offering) or a maximum of 600,330 shares if the minimum number of shares is subscribed in the offering.

Strong Main Owner

Tamtron will have a very strong main owner. The main owner’s ownership will be significantly diluted in the offering but will remain clearly above 50%. As of the prospectus date, Tamtron’s Chairman of the Board owns approximately 88.71 percent of Tamtron’s shares (p. 3). If the IPO proceeds as planned, the Chairman of the Board will own approximately 63.59 percent of all Tamtron shares (p. 56).

Ensto Invest Oy will be another significant shareholder. According to the prospectus, Ensto’s subscription commitment covers a total of approximately 6.25 million euros worth of shares offered. Ensto will subscribe to shares in the institutional offering at a subscription price of 6.28 euros per share.

(6,250,000 / 6.28 = approximately 995,000 shares)

According to the prospectus, as a result of the IPO and share conversion, the number of Tamtron shares may increase to a maximum of 6,446,457 shares. Thus, Ensto’s ownership stake would be approximately 15%.

Tero Luoma, CEO of Ensto Invest Oy, will become a new member of Tamtron’s Board of Directors. This decision is conditional on the completion of the IPO and will become effective immediately upon the commencement of trading in the shares on First North (p. 74).

Transfer Restrictions

Tamtron’s Board members and certain members of the management team have committed to a share transfer restriction agreement (p. 73). The transfer restriction ends 365 days after the first trading day of the shares on First North.

Market Making

Due to the strong main owner and the transfer restriction agreement, the liquidity of Tamtron’s share will remain low, and the share price will experience volatility. Therefore, Tamtron has entered into an agreement with Lago Kapital Oy for market making services for its shares.

Page 74 of the listing prospectus states that

Lago Kapital has committed to provide bid and ask quotes for the shares on First North on every trading day for at least 85 percent of the continuous trading time. The market-making agreement is valid for a fixed period of 6 months from the listing and continues thereafter with a 2-month notice period (p. 74).

Valuation

According to the listing prospectus, the pre-offering valuation of the company’s entire share capital is 28.5 million euros.

According to the prospectus, Tamtron has interest-bearing net debt of 17,575,000 euros. Thus, Tamtron’s enterprise value (EV) is 28.5 + 17.5 = 46 million euros.

According to Tamtron’s listing prospectus, the EBITDA for the fiscal year 2022 will be 4.68 million euros.

→ The EV/EBITDA multiple is therefore 46 / 4.68 = 9.8

I would compare this multiple, for example, to the peer group of Norrhydro, which was listed last year. According to Inderes’ investment research on Norrhydro, page 33, Norrhydro’s peer group’s 2022 EV/EBITDA multiple was at a median level of 11x.

Tamtron’s peer group is naturally somewhat different. According to page 32 of the investment research, Norrhydro’s peer group consisted of small domestic listed engineering companies (Kesla, Robit), Norrhydro’s customers (Ponsse, Cargotec, Metso Outotec, Sandvik, Kongsberg), and hydraulic industry players.

Tamtron’s customer base is listed on pages 23, 34 of the prospectus.

Several multi-year cooperation agreements have been signed → sales are estimated to account for approximately 10% of the revenue generated from scale sales

The company aims for growth and is seeking funding from the stock market. Perhaps when seeking funding earlier, banks may have taken issue with the concentrated ownership base, relatively weak equity level, and ambitious growth targets. Now Ensto is partly guaranteeing that the main owner will not step on the toes of the operative management.The valuation seems okay, but the small size of the public offering will surely decrease interest. I doubt many hundreds of shares will be obtained from the public offering. We probably won’t see the same interest as in Norrhydro’s offering. However, a broader product range than its main competitors provides support.

If you look at the EBITDA (earnings before interest, taxes, depreciation, and amortization), as the management communicates, the company’s profitability is good, but due to acquisition depreciations, not much has been left on the bottom line in recent years. The company has quite ambitious goals because while the entire category is intended to be tripled, they also aim to accelerate the growth rate even more than when they were smaller.

Tamtron’s market only grows by 1-2% annually, and in my opinion, there was surprisingly little talk about gaining market share or a track record in the management’s presentation, even though it is a prerequisite for achieving the goals.

All in all, I think the offering is quite okay, but I will personally wait and see if Tamtron can accelerate its growth according to its goals – the 9 million funding raised in the offering alone is not enough for this; instead, high-quality strategy execution is needed, where there is not much room for missteps.

Sijoitusasunnot canceled its own listing, and this thread is quieter than a graveyard. The subscription ends tomorrow at 4:00 PM; hopefully, with the help of large anchors, the offering will go through. I’d gladly scoop this up from the discount bin later for my portfolio, as I have an emotional connection to the company from the past () and the industry is suitably boring to fill a portfolio.

They intend to grow at a fairly rapid pace. On the other hand, the next couple of years might be very suitable for acquisitions, as valuations could be more moderate during a recession than at other times.

The chairman of the board, former CEO Asikainen, apparently originally bought the company for himself back in 1993. Points for long-term commitment.

I skimmed the company’s financials and it even looked a little interesting. Then I saw all the talk about a “WaaS company,” and I’m not getting involved in that kind of nonsense. Investment journalism could also address how excessive marketing-speak can drive investors away: it makes it feel like a scam. This also brings to mind the overly sweet social media presence of a certain IPO that was canceled.

I’d be surprised if the share price doesn’t drop once trading begins. There’s no stabilizer, and some people will want to get rid of their shares immediately. A week after trading starts, the price will have dropped by at least 10%. I hope I’m wrong!