I became interested in Tamtron; the growth story looks attractive and, in my view, it is still attractively priced relative to that. So I started going through the company’s 2024 annual report.

Potential red flags that stood out to me:

Chairman of the Board Pentti Asikainen owns a significant majority of the shares (60%). In the 2024 Annual Report, there was also a mention in the section on related-party transactions:

- The company leases real estate from the Chairman of the Board, Pentti Asikainen, for €275k.

- The company purchases services worth €425k from a company fully controlled by Pentti Asikainen.

There is nothing inherently wrong with these as such, but of course, a person exercising significant power in the company could misuse their position in these ways if they wanted to.

Does @Pauli_Lohi or others on the forum have information regarding these transactions? What services are being purchased from Pentti Asikainen’s company, or why has the decision been made for Pentti Asikainen to sell services to Tamtron through another of his companies? Or the lease agreement where the company rents premises from Pentti Asikainen? Perhaps there is nothing more mysterious or wrong about it, but I thought I’d ask if anyone here has more information or opinions on the matter.

15 Likes

Relevant questions @quartercompounder! I discussed the topic with the company as well before replying here on the forum.

-

The company leases properties from the Chairman of the Board, Pentti Asikainen, to the value of €275k.

The leased property is Tamtron’s facility in Tampere, where, among other things, onboard scales are manufactured and the necessary cleanrooms for sensor production are located. Rental costs have decreased slightly compared to the pre-listing level (2020-21: 337-344 TEUR).

-

The company purchases services worth €425k from a company fully owned by Pentti Asikainen.

Purchases from Wuzhou City Tamtron Science and Technology Co, owned by Asikainen, consist of metal component procurement from the Chinese market (e.g., sensor frames and cast parts). Tamtron has several sources for these types of semi-bulk components, including in Europe. They are usually cheaper in China, but lead times are longer. In practice, these procurement sources are used depending on the situation and where it is most advantageous to purchase at any given time. The company is not specifically dependent on WCTST, but it offers an easy channel for the company, acting as an intermediary for a wider group of Chinese subcontractors. The company was founded about 20 years ago as a subsidiary of Tamtron (as part of a larger investment plan), but plans apparently changed, and the company remained under Asikainen’s ownership when Intera Partners acquired Tamtron in 2011.

As stated in the IPO prospectus, the company maintains that both of the aforementioned commercial relationships are based on standard commercial terms. For example, the rent level has been verified by external appraisers to be at market rates. However, it is practically impossible for a retail investor to accurately assess the profitability of these business relationships from Tamtron’s perspective. Concentrated ownership can generally be seen as a risk for minority shareholders, but in Tamtron’s case, I haven’t specifically sensed anything suspicious. The majority owner’s financial interest through Tamtron shareholdings is, however, clearly greater than the aforementioned business relationships.

18 Likes

Thanks @Pauli_Lohi for the excellent clarification! This removes the biggest concerns, at least for me.

3 Likes

Here are Pauli’s preview comments, as Tamtron reports its H2 results on Thursday.

Tamtron reports its H2 results on Thursday, March 5. We expect strong growth and earnings improvement from the company for H2, supported by a solid order book and acquisitions, among other factors. Our full-year 2025 forecasts are near the lower end of the guidance range due to a weaker H1. Key to the forecasts in the report is how much room the company sees for improvement in system sales, where 2025 was clearly better than previous years in terms of orders. We estimate that the slow recovery of the industrial cycle has continued in Europe recently, enabling the continuation of reasonable organic growth.

5 Likes

Tamtron’s earnings live stream starts today at 8:55

3 Likes

July–December 2025 in brief

- Revenue increased by 12.4% from the previous year to EUR 31,407 (27,936) thousand

- Operating profit (EBIT) was EUR 1,736 (1,163) thousand and the operating profit margin was 5.5% (4.2%)

- Operating profit adjusted for amortization of consolidated goodwill was EUR 2,880 (2,261) thousand, and the operating profit margin was 9.2% (7.9%)

- EBITDA was EUR 3,981 (3,020) thousand and the EBITDA margin was 12.7% (10.8%)

- Profit for the period was EUR 834 (10) thousand

- Return on equity (ROE) was 3.8% (0.1%) for the 6-month period ended 31 December 2025

- Return on equity (ROE) adjusted for amortization of consolidated goodwill was 9.0 (5.2)% for the 6-month period ended 31 December 2025.

January–December 2025 in brief

- Revenue increased by 5.5% from the previous year to EUR 55,666 (52,741) thousand

- Operating profit (EBIT) was EUR 1,868 (2,318) thousand and the operating profit margin was 3.4% (4.4%)

- Operating profit adjusted for amortization of consolidated goodwill was EUR 4,090 (4,433) thousand, and the operating profit margin was 7.3% (8.4%)

- EBITDA was EUR 5,931 (5,916) thousand and the EBITDA margin was 10.7% (11.2%)

- Profit for the period was EUR 471 (597) thousand

- Return on equity (ROE) was 2.2% (3.0%) for the 12-month period ended 31 December 2025

- Return on equity (ROE) adjusted for amortization of consolidated goodwill was 12.6% (13.5%) for the 12-month period ended 31 December 2025

- Equity ratio at the end of the financial year was 51.6% (51.1%)

- The Group’s order backlog at the end of the financial year was EUR 8,193 (6,857) thousand

The Board of Directors proposes to the Annual General Meeting that a dividend of EUR 0.15 per share be paid.

GUIDANCE FOR 2026 (PUBLISHED 5 MARCH 2026)

Tamtron expects revenue and EBITDA to increase compared to 2025.

https://tamtrongroup.com/fi/mfn_news/tamtron-group-oyjn-tilinpaatostiedote-1-1-31-12-2025-liikevaihto-uuteen-ennatykseen-vuonna-2025-toinen-vuosipuolisko-historian-vahvin/

5 Likes

The company misses its guidance for the second year in a row and doesn’t issue a profit warning in either year. What’s even the point of providing guidance?

12 Likes

Guidance for 2025 (published 12 March 2025) was that Tamtron estimated revenue to exceed EUR 58 million and EBITDA to exceed EUR 6 million. The actual result was revenue of EUR 55.6 million and EBITDA of EUR 5.9 million.

The actual EBITDA was so close to the guidance that I’m not bothered by the lack of a profit warning. Since earnings per share also improved from last year’s €0.08 to €0.11, I am quite satisfied with the performance, especially considering the general market situation.

11 Likes

Pauli interviewed CEO Mikko Keskinen regarding H2

Topics:

00:00 Introduction

00:20 Development in H2

01:54 Why the guidance was not updated

03:20 Development of the on-board business

05:12 Development of digital services

06:53 Guidance for 2026

08:43 Impact of growth investments on profitability

10:08 Acquisitions

12:50 Updated financial targets

5 Likes

Pauli has written a new company report following Tamtron’s H2 results

The weaker-than-expected H2 report led to moderate forecast changes for the coming years, but in the big picture, the story remains unchanged. Strategic growth work, including the internationalization of SaaS and system sales, continues. We expect earnings performance to pick up in the current year, driven by both reasonable revenue growth and the conclusion of the ERP project last year. In our view, the valuation is attractive relative to the company’s value creation profile even with the lowered forecasts. We lower our recommendation to Accumulate (prev. Buy) and the target price to EUR 6.0 (prev. EUR 6.4).

Quoted from the report:

Relative profitability strengthened significantly

H2 EBITDA was EUR 4.0 million and improved by EUR 1 million relative to a weak comparison period. Relative profitability was supported particularly by favorable development in the gross margin, influenced by successful system deliveries and the gradual positive impact of SaaS growth on the company’s margin profile. Adjusted EBIT was EUR 2.9 million (H2’24: EUR 2.2 million, forecast: EUR 3.5 million).

2 Likes

Hi @Pauli_Lohi and have a nice weekend.

I have been a Tamtron shareholder since the IPO and I’m fairly satisfied with the performance. I consider the dividend now announced to be high in relation to the company’s growth targets and cash flow. What do you think yourself, and am I on the right track with the approach below?

According to my calculations, the 2022–2025 free cash flow (adjusted for acquisitions from investments) has been about half of Inderes’ adjusted EPS. In the table below, 2022–2025 FCF is 0.69 / EPS (adj.) is 1.35.

If Tamtron’s annual EPS capability is now around €0.4 and half of that, i.e., €0.2, remains as free cash flow, then after a €0.15 dividend, only 1/4 of the free cash flow (€0.05/share) is left to be used for growth? So, is the company’s growth intended to be funded mainly through debt and its own shares?

On the other hand, could the free cash flow be higher relative to the result? Or is my thinking flawed in that the cash flow from investments also includes growth investments? Do you have a breakdown of the ratio of maintenance investments and growth investments within the total?

2022 2023 2024 2025

Cumulative EPS (adj.)

0.29 0.62 0.99 1.35

Cumulative OCF/Share

0.14 0.32 1.14 1.63

Cumulative FCF/Share

−0.10 −0.09 0.47 0.69

6 Likes

Good question, and now is a fitting moment to look at this topic as the company, through its dividend payment, is shifting its capital allocation compared to the line we have seen in recent years.

I wouldn’t draw conclusions purely based on the average cash flows of previous years because, for instance, in 2023, the amount of net working capital on the balance sheet increased significantly (presumably following the Lahti Precision acquisition), which weighed on the cash flow. However, a similar increase in net working capital is not expected in the future.

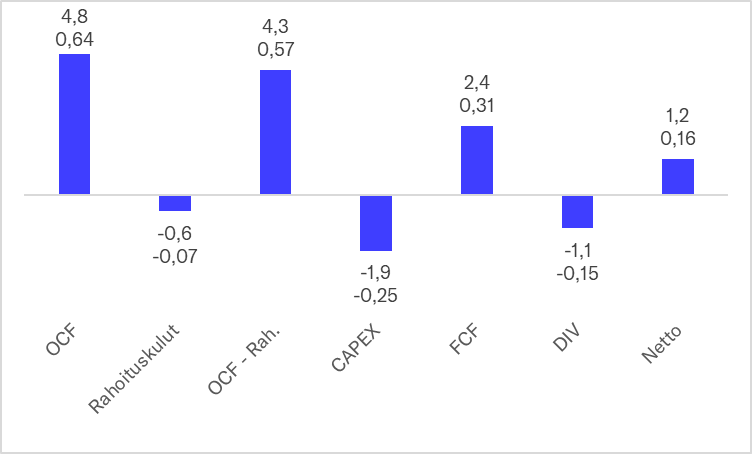

I did my own calculation of the company’s cash flow profile based on 2026 forecasts. According to the forecast, dividends would account for about half of the free cash flow (FCF: 2.4 MEUR or €0.31/share), leaving approximately 1.2 MEUR (€0.16/share) for debt repayments or acquisitions. Regarding working capital, the forecast assumes that the net working capital-to-revenue ratio will grow to 15.1% (2025: 14.9%), so in that sense, the forecast is relatively moderate regarding cash flow.

In addition to cash flow, the current leverage on the balance sheet is moderate (2025 net debt/EBITDA: 1.3x), so acquisitions can be partially debt-financed. The company has also frequently conducted small share issues in connection with acquisitions, directed at least to the seller of the acquired business or potentially also to existing shareholders. Thus, in addition to internal cash flow and debt, share issues are also utilized to fund acquisitions.

Tamtron’s cash flows 2026e (upper figure MEUR, lower EUR per share)

OCF: Operating cash flow

OCF - Rah.: Operating cash flow after financing costs

CAPEX: Organic investments

FCF: Free cash flow

DIV: Dividend

Netto: Net amount remaining for debt repayment or acquisitions

12 Likes

Thank you for the response!

I wasn’t surprised myself that dividend payments were initiated, but I would have expected a more moderate level to start with. For now, I have to believe and trust that the company makes all the necessary investments and investments with a good return on capital before the distribution decision, so that the tail doesn’t start wagging the dog. As a shareholder, I will follow with interest how the company develops.

In the case of this company in particular, I prefer per-share figures because the company actively uses its own shares for growth.

1 Like

Pauli has written an excellent comprehensive report on Tamtron

Tamtron, a company producing industrial weighing solutions, is a relatively stable and profitable company, as its solutions are critical for the smooth continuation of customer processes, and services account for over a third of the company’s revenue. In recent years, the company has significantly invested in growth in SaaS solutions and in expanding the sales of industrial dosing systems outside of Finland, which should support earnings growth in the medium term. The weak economic cycle in the industrial sector has hindered organic development in recent years, and revenue growth has primarily relied on acquisitions. We slightly cut our current year forecasts as the Iran war causes downward pressure on economic growth expectations, and we lower our target price to 6.0 euros (previously 6.2 €). We still consider the valuation to be favorable in the big picture, so we reiterate our Add recommendation.

Capex investment needs are moderate

We forecast organic investments to be 1.9-2.2 MEUR/year for 2026-30, which is in line with our forecasted normal depreciation level. In our view, the company currently has no need to increase capex investments, so the forecasted earnings growth will be reflected as clear free cash flow growth. Investments may even decrease in the short term after the completion of the ERP project and as mScales development work potentially becomes more efficient with AI. Intangible amortizations related to acquisitions are 2.3 MEUR in our forecasts for 2026e but decrease to 1.5 MEUR by 2030e, assuming the company does not execute new acquisitions.

Quoted from the report:

7 Likes

Miksu and Pauli discussed Tamtron based on an extensive report

Topics:

00:00 Introduction

00:15 What problem does Tamtron solve?

02:13 Cloud-based data solutions

03:01 Development of the weighing equipment market

04:19 Forecasts for the coming years

05:19 Financial targets and acquisitions

06:58 Fragmented competitive landscape

10:04 Add recommendation

6 Likes

Here are Pauli’s comments regarding Tamtron’s small acquisition

Tamtron announced on Monday that it has acquired the entire share capital of the Finnish company Teknoscale Oy. We view the acquisition as a step in line with the company’s strategy that complements its product portfolio. Tamtron is financing part of the purchase price through a directed share issue, but the company did not disclose the full purchase price of the acquisition. Our initial stance on this small acquisition is neutral, and we will incorporate it into our forecasts in our next company report.

3 Likes