Thanks for the answer.

I am technically familiar with traditional and cloud-based SaaS solutions through my work.

Cloud-based SaaS solutions have many advantages compared to traditional solutions (on-premise servers).

Advantages include, for example, easier geographical expansion, scalability as load increases, security, dynamic pricing, IT infrastructure cost savings for the customer, system updates…

These advantages are particularly evident for a customer operating in multiple locations and countries, such as Tamtron’s announced deal.

In my opinion, it is crucial for Tamtron’s competitiveness to know how many potential competitors they have for the mScale system.

Especially since the large weighing markets in Central Europe are in some places untapped regarding SaaS systems.

Tamtron certainly knows its competitors well, and perhaps one could ask them about their key competitors at some point.

I promised in the episode that I would share this here too, and I spoke highly of Inderes’ discussion threads in general. Please give your comments on this: does it clarify the themes of IPOs and M&A-driven growth?

M&A growth after the IPO Mikko Keskinen Jari Lauriala neuvottelija 276 out now!

Tamtron Group CEO Mikko Keskinen and Translink Corporate Finance Managing Partner Jari Lauriala explain how Tamtron’s IPO has served as an effective enabler for M&A-driven growth. Mergers and acquisitions are an unnecessarily shunned way to grow, and even Finns can execute them successfully when implemented with the right strategy.

Tamtron’s weighing solutions took a huge leap forward just a few months after the December 2022 IPO when it acquired Lahti Precision. Its SaaS solution, mScales, also acts as a growth driver as an increasing number of customers use it for storing weighing and regulatory data.

Jari describes the two roles of a Certified Adviser – acting as the financial advisor for the IPO and providing ongoing assistance with the company’s disclosure and listing obligations as a Certified Adviser. The episode does not provide investment recommendations.

Even though capital is scarce in Finland, Tamtron has attracted investors like Ensto Invest and Hannu Kytölä, as well as Mika Heikkilä of Proprius Partners Oy, as the company has been able to deliver on its IPO targets through profitable M&A-driven growth following the listing.

Tamtron announced yesterday a share buyback program. In my opinion, the release does not state exactly for what purpose the shares are being purchased. The program’s relatively small scale (at most 0.4% of the total number of shares) would, in my estimation, suggest that the program is related to key personnel incentives. The company announced in the summer that it would implement a share-based incentive program, including for the management team and the CEO, which I think is a good way to engage and motivate key personnel.

Tamtron CEO Mikko Keskinen on Karon Grilli.

Tamtron’s financial targets for the end of 2027 include revenue of EUR 96 million. In Inderes’ forecasts, it is EUR 60 million.

To reach that, according to Mikko’s hints, there may be several acquisitions coming. At the 38-minute mark in the video.

The mScales service is being developed to support, among other things, preventive maintenance of equipment, and various other ways of utilizing data are being considered.

Interesting content overall, and Mikko remains confident in Tamtron’s growth.

Sijoittaja.fi identified three interesting companies from First North, and one of them was Tamtron. The rest of the article, which includes the so-called stock comparison table, is behind a paywall.

We analyzed all First North stocks and selected stocks we are willing to invest in ourselves. We first conducted a preliminary screening, examining the companies’ revenue and profit figures. We chose companies with positive revenue and earnings development. This excluded stocks in the development phase.

Next, we delved into the companies’ business operations and evaluated their business models, market situation, and future prospects. We also examined other important characteristics and key factors for investors, such as growth potential, key financial ratios, risks, and valuation.

Pauli has prepared a comprehensive report on Tamtron.

Like other comprehensive reports, this one is also available for everyone to read.

We estimate that Tamtron’s key growth projects will progress slightly faster in the coming years than in recent years, in the form of SaaS growth and system sales. According to our assessment, the recent weak industrial cycle could gradually ease starting from 2025. The company’s good profitability, favorable cash flow profile, and attractive valuation make the stock appealing in our opinion. We reiterate our Add recommendation and raise the target price to 6.2 euros (previously 6.0 euros).

Following the extensive report, Miksu and Pauli discussed Tamtron.

Tamtron, which offers comprehensive weighing and dosing services, has the development of high-margin SaaS solutions as its key growth driver. Analyst Pauli Lohi tells more about the company and its potential.

Topics:

00:00 Introduction

00:13 Tamtron’s Business

02:05 Finland as the Most Significant Market

02:35 Development of SaaS Solutions

04:32 Global Industrial Weighing Equipment Market

05:44 Tamtron’s Extensive Product Range

07:24 Company’s Growth Strategy

09:41 Moderate Valuation

Tamtron Group Plc | Press Release | 20.02.2025 at 09:00:00 EET

Tamtron Precision Oy, a subsidiary of Tamtron Group Plc, has received the largest order in Tamtron Group’s history from a significant European technology supplier. The order concerns the supply of weighing and dosing equipment for the metal and mining industry, and its value is over three million euros. The name of the customer will not be disclosed.

“Over the decades, Tamtron Precision has supplied weighing and dosing systems to numerous different industries. This realized deal is a testament to our long-term customer’s trust in our expertise and our ability to deliver system supplies serving a demanding industry,” says Niko Toimela, Sales and Marketing Director of Tamtron Precision.

Deliveries will mainly take place during 2025.

Order supports Tamtron’s growth strategy and internationalization

Economic uncertainty has overshadowed several industries last year. The heavy industry’s investments in new technology indicate nascent confidence in growth.

“Industrial companies are increasingly investing in production efficiency and technological solutions that improve process efficiency and help optimize resource utilization. This realized deal is a positive signal of development. At the same time, it excellently supports Tamtron’s growth strategy and strengthens our position in international markets,” states Sami Pekkola, CEO of Tamtron Precision.

Tamtron is one of the world’s leading providers of weighing solutions, and its extensive product and service portfolio covers precise and reliable weighing and dosing technology for various industries. Tamtron continues its internationalization according to its strategy and invests even more strongly in innovative solutions that support sustainable industrial growth.

Pauli has given his comments on Tamtron’s largest order in history.

System sales became part of Tamtron through an acquisition in 2023, and the aim is to systematically grow it by expanding distribution to the company’s other countries outside Finland. The recently announced large order supports the growth outlook for the current year. We will review the forecasts at the latest in connection with the company’s H2 report.

Today we published a preliminary comment, in connection with which the 2025 growth forecasts were slightly raised due to the previously announced EUR 3 million system order.

Please also note that we are organizing a results live stream next week at 8:55 AM!

I am interested in the growth of mScales SaaS services in the results.

This is because Mikko Keskinen has stated that if they manage to sell mScales to a customer, it increases the likelihood that the customer will also order weighing equipment from Tamtron in the future.

This, of course, also brings more service sales.

mScales can be connected to weighing equipment from other manufacturers than Tamtron.

So, mScales is a scalable business, brings stable revenue, and additionally partly increases the sales of weighing equipment and services.

Therefore, it would be interesting to know who Tamtron considers mScales’ competitors to be and what mScales’ strengths are in relation to them.

As no information is available on mScales sales, one has to settle for the Lead of Software Technology recruitment announcement.

It mentions there “We are growing strongly into international markets and continuously developing our service to be more scalable and efficient”

Well, on Wednesday we will hear whether strong growth into international markets has occurred or if it’s still just a dream.

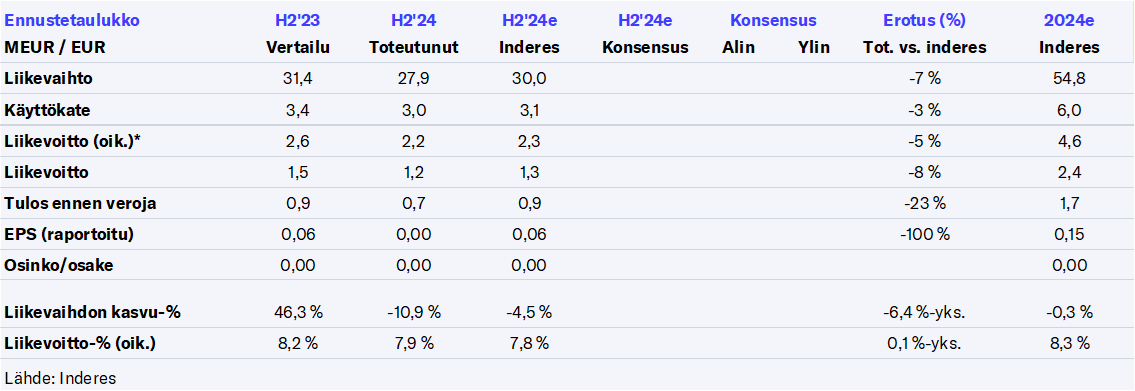

H2’s actual figures showed slight weakness, especially regarding revenue. Adjusted operating profit was 5% below our forecast. On the other hand, relative profitability withstood the cyclical weakness in revenue surprisingly well. Onboard sales and service revenue grew, but the weakness came from system sales.

The guidance for 2025 was in line with our forecasts. Revenue is expected to be over 58 MEUR and EBITDA over 6 MEUR (our forecasts 58.8 MEUR and 6.7 MEUR).

After watching Tamtron’s earnings release, these observations came to mind.

When discussing the decrease in order book from €9.4M in 2023 to €6.9M in 2024, Mikko Keskinen emphasized that 2025 has started well, order development has been strong, and 2025 looks stronger in terms of orders.

The gross margin percentage increased because Onboard and Digital services grew, which have a better gross margin. So, it wouldn’t matter if OnBoard and Digital continue to grow better than the Industrial segment.

Questions about mScales came up in the Q&A. Based on Mikko Keskinen’s answers, mScales has virtually no direct competitors, i.e., SaaS services to which one can connect their own and competitors’ weighing equipment.

From Mikko’s answer, I understood that Tamtron’s competitive advantage is also that they have both weighing equipment and the mScales service, and there are no direct competitors for this.

I understand that this combination provides a competitive advantage in cross-selling, meaning a customer might choose Tamtron’s weighing equipment because they can get the SaaS service from the same company.

On the other hand, once a customer has purchased the mScales service, they may more easily buy weighing equipment from Tamtron in the future as well.

Ambitious financial targets for 2027 were maintained, meaning an acquisition is coming because a €96M revenue cannot be achieved organically.

The result was a slight disappointment, but I still have faith.

Edit In Inderes’s interview video with Mikko Keskinen, it was stated that the growth of the high-margin OnBoard business was partly due to new OEM customers, meaning the growth in OnBoard revenue was not temporary but will bring fairly stable revenue growth in the future.

In addition to Services (incl. mScales), Tamtron has OEM customer relationships with long contracts that bring fairly stable revenue.

Pauli has made a new company report on Tamtron after H2.

The cyclicality of demand for large-scale systems materialized in the second half of 2024, and revenue fell short of expectations. However, development was good in more continuous and higher-margin segments, such as onboard product sales and services. Signs of a turnaround are visible in both the recovery of the order book and strategic advancements. We see the valuation as favorable relative to the quality of the business and reiterate our Add recommendation with a target price of 6.2 euros (unchanged).

The company has not commented on this matter. Typically, guidance policy includes a certain internally defined deviation that is allowed before issuing profit warnings. I don’t know the exact criteria applied by Tamtron in this case. One can also speculate whether other factors influenced the decision-making (e.g., profitability in line with guidance and relatively good for 2024, as well as a guidance outlook for 2025 in line with market expectations).

Looking at Tamtron’s stock market history, it can be seen that the company has given rather optimistic guidances and performed somewhat softer than expected. The high profitability guidance for 2024 (EBITDA: 14-15%) given at the time of listing in late 2022 was withdrawn, citing the impact of the Lahti Precision acquisition, and the realized operating profit (EBITDA) in 2023 was significantly lower (10.8%). The 2024 operating profit (EBITDA) guidance was 10-13% and the realization was 11.2%, but this time revenue fell short of guidance. In my opinion, the deviation for 2024 is more attributable to cyclical market weakness and the timing of customer demand. However, an investor can draw some conclusions from this when evaluating the company’s guidances.

I myself did not find a materiality threshold in Tamtron’s disclosure policy, below which a profit warning would be omitted:

The company communicates clearly and consistently about both positive and negative matters without delay and simultaneously to all stakeholders.

With quick thought, one would assume that in the 50-60 million euro revenue category, a suitable threshold would be around 0.5 - 0.6 million euros, below which a profit warning could be omitted. Now it was €52.7M when the midpoint of the range was €55M, and even the lower end was missed by €1.3M, so we are on rather shaky ground if one tries to claim that the miss was not significant.

Since the company is stonewalling on the matter, I sent an inquiry to the Financial Supervisory Authority to get some clarity on it