Good question, and now is a fitting moment to look at this topic as the company, through its dividend payment, is shifting its capital allocation compared to the line we have seen in recent years.

I wouldn’t draw conclusions purely based on the average cash flows of previous years because, for instance, in 2023, the amount of net working capital on the balance sheet increased significantly (presumably following the Lahti Precision acquisition), which weighed on the cash flow. However, a similar increase in net working capital is not expected in the future.

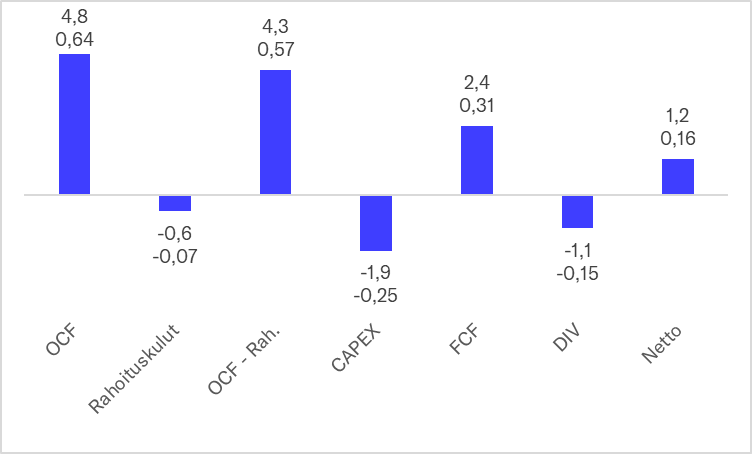

I did my own calculation of the company’s cash flow profile based on 2026 forecasts. According to the forecast, dividends would account for about half of the free cash flow (FCF: 2.4 MEUR or €0.31/share), leaving approximately 1.2 MEUR (€0.16/share) for debt repayments or acquisitions. Regarding working capital, the forecast assumes that the net working capital-to-revenue ratio will grow to 15.1% (2025: 14.9%), so in that sense, the forecast is relatively moderate regarding cash flow.

In addition to cash flow, the current leverage on the balance sheet is moderate (2025 net debt/EBITDA: 1.3x), so acquisitions can be partially debt-financed. The company has also frequently conducted small share issues in connection with acquisitions, directed at least to the seller of the acquired business or potentially also to existing shareholders. Thus, in addition to internal cash flow and debt, share issues are also utilized to fund acquisitions.

Tamtron’s cash flows 2026e (upper figure MEUR, lower EUR per share)

OCF: Operating cash flow

OCF - Rah.: Operating cash flow after financing costs

CAPEX: Organic investments

FCF: Free cash flow

DIV: Dividend

Netto: Net amount remaining for debt repayment or acquisitions