I thought so myself at first. But is it really just tinkering? According to Statistics Finland, the median portfolio size (including both listed shares and funds) was 5,770 euros at the end of 2023. As Finnish listed companies distribute approximately 14 billion euros annually and the market value of these companies is about 320 billion euros, the dividend yield is 4.38%. With a median portfolio, the dividend yield would be 253 euros per year if all investments were in shares. A 1000 euro deduction would mean that at least half (actually a much larger group) would receive dividends with 0% tax. In this sense, it’s not tinkering but a genuine incentive to move funds from bank accounts into shares. A 1000 euro dividend income requires a 22,831 euro share portfolio. But is this method needed?

The Finnish Shareholders’ Association justifies the 1000 euro deduction:

- It is simpler to implement and easier to understand than the current tax exemption for sales under 1000 euros.

- It encourages moving funds into shares from bank accounts, which have a 30% withholding tax.

- It would be indifferent whether capital gains are received as dividends or capital gains.

The Finnish Shareholders’ Association also proposes that

- dividends of listed and unlisted companies be harmonized so that the owner’s total tax rate in both listed and unlisted companies would be 30% (or 34%), and

- the right of unlisted companies to receive dividends from listed companies tax-free, if the company owns more than 10% of the share capital, be abolished.

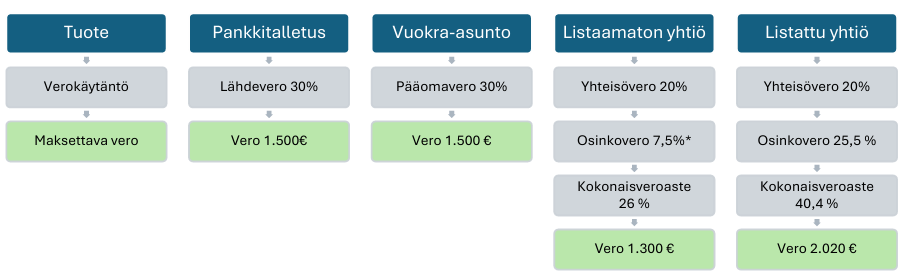

Below is an overview of how direct returns on a hypothetical 100,000 euro asset are taxed.

NOW:

According to the Finnish Shareholders’ Association, the current tax relief for unlisted companies is an obstacle to listing a limited company on the stock exchange. I agree. Of course, there are other obstacles, but removing each obstacle is good for Finland’s GDP growth.

Entrepreneur’s note 1: The current tax relief for dividends of unlisted companies, still in force, has also been perceived as a political bone of contention throughout its existence and therefore temporary, which has encouraged the distribution of more dividends than necessary. Every euro of dividend distributed is taken away from the company’s future investments. The current model acts as an effective barrier to growth.

PROPOSAL:

Entrepreneur’s note 2: Lowering the corporate tax to 15% would enable larger investments. This could be compensated by a higher dividend tax so that the total tax rate of 30% is maintained.

The Finnish Shareholders’ Association’s proposal falls short. If growth is truly desired, investing in business activities must be made more attractive at all capital levels than investing in bank deposits or real estate. It is not enough for it to be attractive to small investors. It must also attract large investors. The same tax treatment for equity invested in a company unifies objectives. At the macro level, this unites the nation, and at the micro level, it facilitates corporate decision-making. Therefore, I propose that the taxation of bank deposits and rental income be tightened to 34% and that the 30,000 euro progressive scale for the total capital gains tax rate be abolished, meaning it would always be 30%.

A total tax rate of 30% would be quite competitive at the European level. Correspondingly,

Sweden 44%

Norway 44%

Denmark 46+%

Germany 48%

Estonia 20%

France 47.5%

The third proposal, the Wealth Accumulation Account (Vaurastumistili), on the other hand, does not seem to serve the national economy in any way. I do not oppose it, but I hope for justifications from a national economic perspective.

All proposals from the Finnish Shareholders’ Association:

- A basic deduction of 1,000 euros for capital gains taxation

- Owner’s capital tax to be uniform across all asset classes

- A new account type, Wealth Accumulation Account (Vaurastumistili), for long-term investing

- Development of the Share Savings Account (OST):

- Loss-making partial withdrawals deductible from other capital gains, without closing the account

- Withholding tax on foreign dividends not charged

- Deposit cap removed

- Allowing ownership of multiple Share Savings Accounts simultaneously

- Trading with subscription rights enabled

- Introduction of a deposit presumption

- Trade unions, employer associations, and political parties to be subject to the same capital gains taxation as private individuals. (foundations or ideological associations would remain outside capital gains taxation)

The proposals of the Finnish Shareholders’ Association are available here Suomen-Osakesaastajat-Veromanifesti-.pdf