In the absence of discussion, let’s continue with an informative approach. Stillfront published its Q3 results on Thursday, with revenue and adj. EBITDAC (Adj. EBITDA - capex) already known in advance. Thus, no major surprises were seen, but a few observations (positives / negatives):

\+ Both Europe and Asia / Middle East growing, negative growth purely driven by the United States (weak organic development + restructuring)

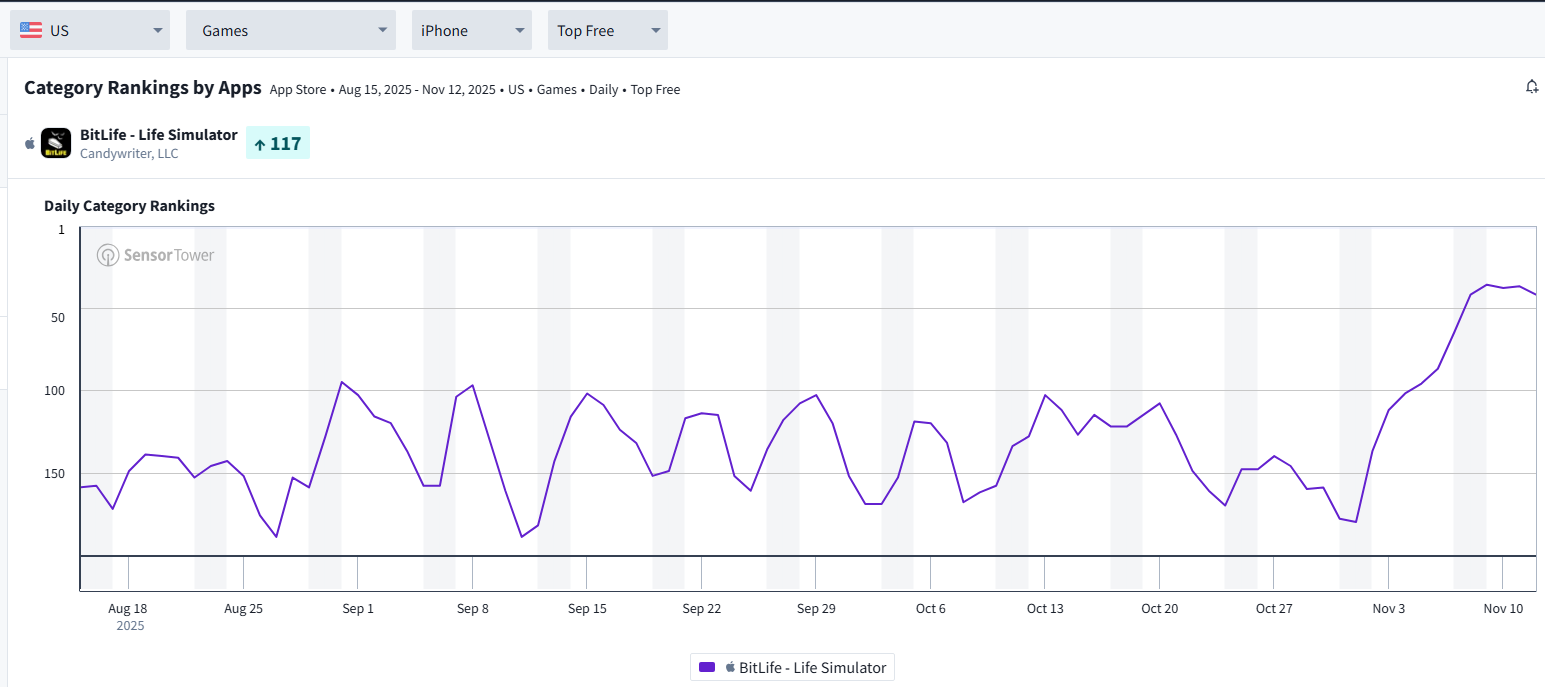

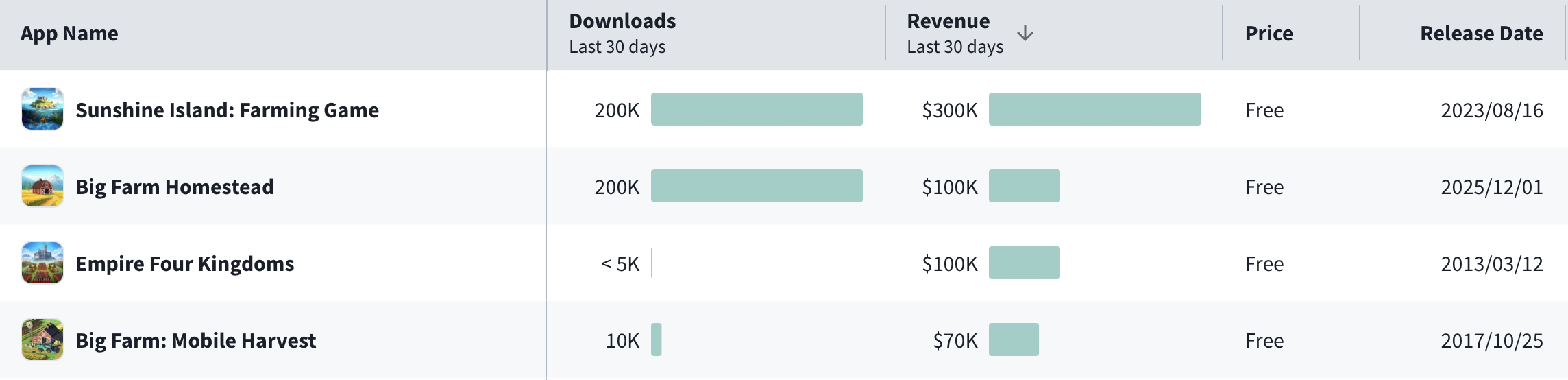

\+ Three new games are being released imminently (the previous one being Sunshine Island 2023), which finally creates belief in better organic revenue development in 2026 (though analysts remain cautious about 2026 growth). The impact on Q4 is moderate (excluding increased marketing costs) due to the late release timing.

\+ DTC channel revenue share grew 33% → 44% y/y, which is a high level compared to the industry. This had a +3ppt impact on gross margin (which, of course, scales significantly to the bottom line), even though players are attracted to DTC channels with significant discounts during the transformation phase.

\- Cash flow was disappointing, but mainly due to NWC fluctuations and abnormally high taxes (LTM cash flow still >900mSEK)

\- No divestment news, but regarding the strategic review, the continuous exploration of divestments was explicitly mentioned – on the other hand, winding down unproductive operations increases the significance of valuable assets, bringing out value without divestments

\- Q4 revenue growth will be closer to H1’s weak levels due to the partial shutdown in the United States and lower UAC usage at the end of Q3, with the focus being on Q4 new game releases –- however, the market seems to be gradually looking past this quarter.

In addition, the board initiated fairly large share buyback programs for earn-out payments (SEK 210m, or 6.4% of market value). On the other hand, this would imply that there is no acute insider project regarding divestments on the board’s table (if I understand insider trading legislation correctly). Before the results, Cantor, among others, surprisingly raised its target price from SEK 6 to SEK 14, and after the Q3 results, Pareto, which had been bearish recently, raised its target price from SEK 6 to SEK 9. The share price also rose +19% in a week, but the YTD graph looks more like Linnanmäki’s wooden roller coaster than a stock price – YTD still -24%.

Next in sight are the three game releases in November/December (the first significant one being Supremacy: Warhammer 40k) and the anticipation of potential divestment news. A new CFO starts at the beginning of the year (although I personally liked the interim CFO’s firm communication), and hopefully, a comprehensive CMD will be held after the strategic review concludes early next year.