Q4 is nearing its halfway point, and the most active period for mobile gaming has begun. Here are a few observations from recent weeks.

-

Own share repurchases: Between 24.10 and 11.11, Stillfront has repurchased 7,405,000 of its own shares (approximately 47mSEK / 210mSEK of the program). The entire program represents about 6% of the market capitalization. (Stockholm Repurchase of Own Shares | Nasdaq)

-

Insider purchases: Board member Markus Jacobs (a gaming industry veteran from EA and King, among others) bought 140,000 shares at the turn of the month for 891kSEK (approx. 82kEUR, a significant sum for a board position). His ownership is now 355k shares, with previous smaller purchases in August.

-

New game soft launches:

-

Big Farm Homestead has been available in limited release in the US Google Play Store since summer. The game aims to build on the successes familiar from Sunshine Island, and initial comments are cautiously positive despite limited content (poor reviews mainly due to restricted levels). According to the Q3 report, the game’s global launch is at the end of the quarter, so the biggest impact on figures will only be in 2026.

-

Supremacy: Warhammer 40k, for which Stillfront likely has the highest expectations, has gradually added countries to its Beta version. More content will be added before the actual release, and on Discord, for example, the game’s development team is in close discussion with dedicated players about bugs, game mechanics, etc. No actual data is available yet, but based on information received today (Discord), the global launch will happen “before the holidays,” contrary to the earlier 17.11 indication. This means development will continue slightly longer than expected due to player feedback, which has included positive comments in addition to development suggestions – negative for Q4 revenue, but in the long run, this is certainly preferable.

-

Nanobit’s new Unfolded: Webtoon Stories, which has also been pre-released in the US, among other places, appears to be a weak game at least at this stage, based on reviews. Of course, I personally haven’t set any expectations for this hypercasual narrative game, and Nanobit’s previous games are not very relevant to the group’s revenue generation (Nanobit’s entire 3-month revenue for three games is $300k on iOS vs. e.g., Jawaker $1m – which also has a larger D2C share – and Bitlife $600k).

-

-

Old games: Due to Stillfront’s “patchwork” nature, it is very difficult to estimate the growth of “Key franchise” games (many games, many countries, many platforms, D2C / 3rd party stores, etc.), but I have not noticed any significant weakening in any game when moving from Q3 to Q4 (note: I mainly follow Sensor Tower’s free data in relation to other games, and it only shows a small part of Stillfront’s earnings in terms of revenue, thus mainly indicating an increase/decrease in activity relative to the rest of the market. For Albion, Steam is also relevant, but most players play directly through Stillfront’s interface). However, a few clear positive observations can be found:

- Bitlife, whose development was somewhat subdued in Q3 due to, among other things, investment in D2C payment channels, has now shown very positive results due to Halloween updates (Vampire theme bit?

). The game has risen to among the top 40 most downloaded games on iOS in the US from around 100-150th place in a 3-month review.

). The game has risen to among the top 40 most downloaded games on iOS in the US from around 100-150th place in a 3-month review.

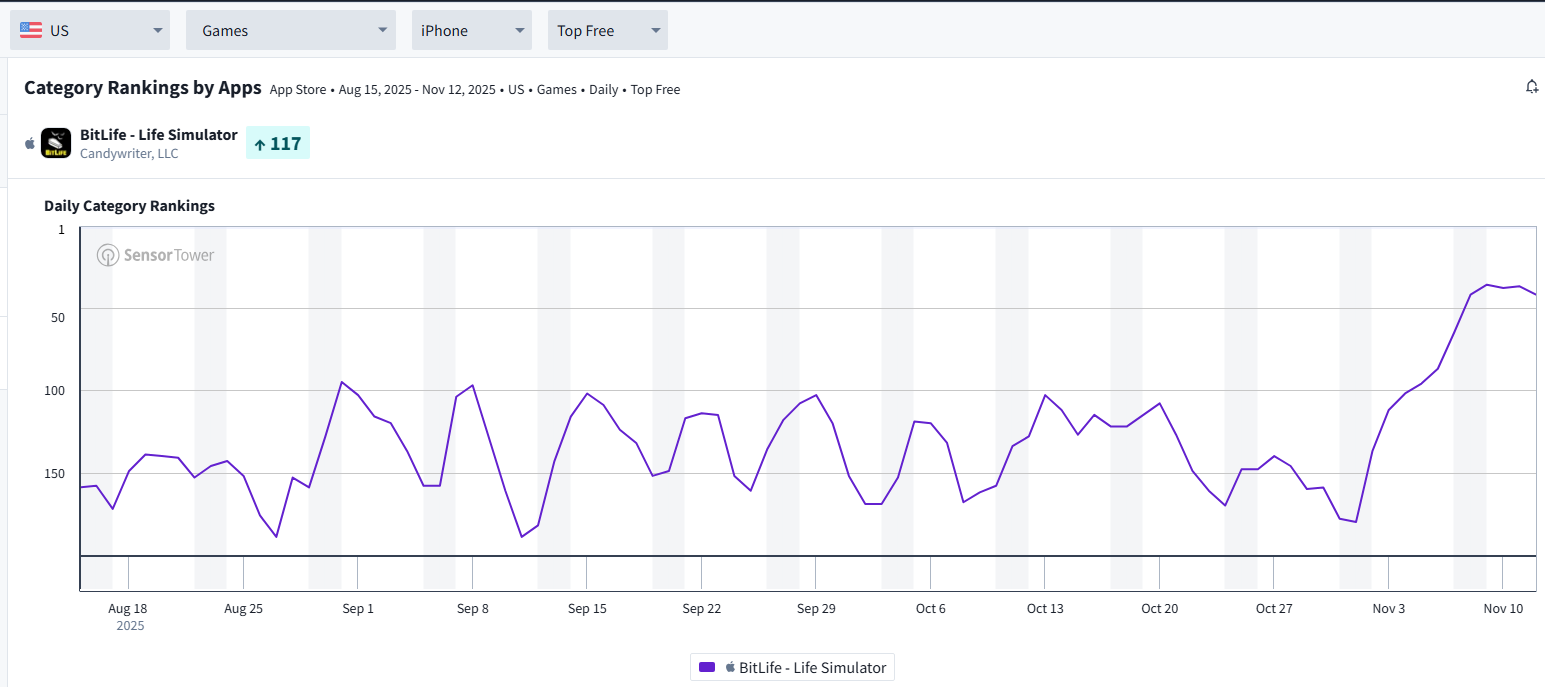

- Sunshine Island, released in 2023, which based on comments continued strong performance already in Q3/25, still seems to have accelerated activity for Q4 (below is a 3-month graph of game downloads on iOS in the US in the “Family” category). It is also noteworthy that the game is already among Stillfront’s top 3 highest-revenue-generating individual games, if only Sensor Tower’s Google Play / iOS are considered – the top 3 are Jawaker, Supremacy: ww3, and Sunshine Island.

- Bitlife, whose development was somewhat subdued in Q3 due to, among other things, investment in D2C payment channels, has now shown very positive results due to Halloween updates (Vampire theme bit?

-

Google Play fees: Not a Q4 matter yet, apparently (awaiting court approval), but on 4.11, an agreement between Epic and Google was announced, which attracted attention in the gaming industry. It concerned the long-running monopoly dispute over Google Play Store fees and openness. The parties agreed that Google would drop its own fee share from approximately 15/30% (under/over 1 million payments) to 9/20% (depending on the payment type) and open Google Play to third-party payment solutions (such as Stillfront’s D2C) without a separate fee. This will have a positive impact on game gross margins and thus on the profitability of mobile gaming companies with leverage over time. As one example of the challenges of the current setup, Sunshine Island has roughly the same number of downloads on iOS / Android, but Android has €700k in monthly revenue vs. €300k on iOS according to Sensor Tower (presumably a larger portion of iOS revenue goes through Stillfront’s own payment service with a higher gross margin).

Overall, it feels like the momentum in the portfolio is currently better than what could be seen at the time of the Q3 earnings release. On the other hand, Q4 revenue will not get much help from new releases, but I see 2/3 of the games as quite potential contributors to organic growth in 2026.

Edit. The situation in point 5 was not finalized, as a judge in the US did not approve the settlement, seeing elements that still restrict competition. No wonder, with Google and Epic as parties ![]()