And it’s quite difficult for an analyst to start pulling growth forecasts out of a hat when the company itself is silent. I took it for granted that clear numerical targets for the short and medium term would be presented at the CMD, but it turned out otherwise. It also makes me wonder why Inderes was chosen again; there are others like Danske, Evli, Carnegie, etc., who analyze many small Finnish companies. But this special situation was caused entirely by themselves.

On the other hand, I gladly welcome such an opportunity to acquire shares at a reasonable price. And besides, Inderes’ reports are extensive and thorough. I bet that this will follow the path paved by Bittium, meaning target prices and recommendations will lag for quite some time. It would be strange if insiders didn’t continue buying shares.

What’s the point of an analysis that just pumps up the stock price? Surely the price will rise based on actual performance and results. A few years ago, stories without proof were still enough (I’m now speaking generally about stocks).

It’s probably Henri’s/Accendo’s hope that SSH’s market value would rise above half a billion, and with that, the stock would also start appearing on big money scanners.

The Chairman of the Board, Österlund, gave an interview in KL regarding the recent initiation of monitoring and disagreements related to growth prospects.

From my perspective, the situation is interesting because the company did not provide concrete growth targets in terms of numbers. Regarding the outlook given at the CMD, my forecast is in line (growth accelerating from next year onwards). This was an interesting point: “In my opinion, it is also not critical whether growth is verified in Q1 next year or Q4 next year. I know that the market potential there is very large. It remains to be seen how quickly it will be reflected in our own figures.” and “Based on Österlund’s comments, precisely defining growth targets would still be a rather difficult task for the company.” I do not disagree that there is a lot of potential, and this potential is one major theme in the report. Our forecasts, through which valuation has also been examined, do indeed show strong growth: revenue in 2029 already nearly 40 MEUR. An investor must therefore take a rather strong stance that growth will accelerate significantly beyond our forecasts if they wish to achieve significant excess returns.

SSH Communications Security is lowering its revenue guidance due to decreased license sales during the fourth quarter and a weakened US dollar. The guidance for positive EBITDA and operational cash flow remains unchanged. Subscription sales are expected to have grown by approximately 10% during 2025.

”The strategic partnership and investment agreement with Leonardo S.p.A. announced on July 1, 2025, was successfully completed on October 21, 2025. Since the agreement came into effect, we have focused during the fourth quarter on aligning our goals with Leonardo and training their personnel, which has delayed the closing of new deals and revenue recognition. We expect the partnership to generate significant revenue growth in 2026,” says SSH CEO Rami Raulas.

New guidance for 2025:

Revenue will decrease slightly compared to 2024. EBITDA and operational cash flow will be positive.

According to the previous guidance issued on February 14, 2025, revenue was expected to grow, and EBITDA and operational cash flow were expected to be positive.

I mean, excuse me, but does this smell a bit like talk? That deals are left unsigned because there’s no time to close them when Leonardo’s people need to be trained?! I’m willing to believe that sales resources have been temporarily reduced, but certainly not that it would have any impact on revenue as early as Q4. After all, the sales cycle is hardly that fast.

And even if I were wrong about the sales cycle, in what company are deals supposedly left unclosed if they are already within reach? I don’t believe that happens at SSH either. To my eyes, it just looks like a poor excuse for why sales aren’t picking up.

Here is Luiro’s comment on SSH’s negative profit warning.

SSH Communications Security issued a profit warning on Friday, in which the company lowered its 2025 revenue guidance. According to the company, the profit warning was a result of weaker-than-expected license sales at the end of the year and exchange rate effects. Following the guidance downgrade, there is downward pressure on our estimates, which we will take into account at the latest in connection with our Q4 earnings preview. From the perspective of SSH’s value creation, we believe the focus should still be kept on the company’s growth outlook, on which the profit warning has a more limited impact.

Negative profit warnings come and go, and that’s nothing new. But what makes this warning feel more pathetic is that only a couple of months ago, the CEO was criticizing analysts for not giving the company the valuation it “deserves.”

A positive profit warning alongside that criticism would have lent more credibility to the CEO’s otherwise quite unbelievable remarks. Now, the CEO’s earlier criticism, at least in my mind, mostly “boosts” this warning to look even more foolish. Or perhaps it’s better put the other way around: the negative warning makes the CEO’s previous comments look even sillier.

Perhaps it has been agreed that target prices won’t be given in this case, as Inderes’s perspective is too short from the viewpoint of the Board Chairman’s wishes.

We have lowered our Q4 forecasts following SSH’s negative profit warning, but our forecasts for the coming years remain largely unchanged as the warning was due to a one-off license deal. The most interesting aspect of the 2025 financial statements is the growth outlook, especially regarding the Leonardo partnership. The growth potential brought by the partnership is significant, but so far there is no evidence of accelerating growth, and in our view, the risk-reward ratio of the stock, which prices in strong scalable growth for the coming years, is weak. We reiterate our target price of EUR 2.0 and our sell recommendation.

Tomorrow we’ll get to read SSH’s updates regarding the financial statements!

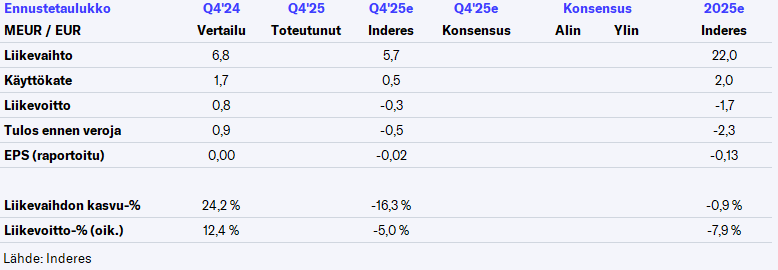

The January report linked by Alokas above served as a preview, but the forecast table was only in the report itself, so I’m posting the table here as a reminder

SSH Communications Security Oyj | Stock Exchange Release | Feb 17, 2026, at 09:00:00 EET

Full-year net sales decreased 2%, quarterly and full-year EBITDA and operating cash flow were positive

October–December 2025:

·Net sales were EUR 5.4 million (EUR 6.8 million)

·EBITDA was EUR 0.1 million (EUR 1.7 million)

·Operating profit (EBIT) was EUR -0.7 million (EUR 0.8 million)

·Profit for the period was EUR -0.2 million (EUR 0.5 million)

·Earnings per share were EUR -0.01 (EUR 0.011)

January–December 2025:

·Net sales were EUR 21.6 million (EUR 22.2 million)

·EBITDA was EUR 1.5 million (EUR 3.4 million)

·Operating profit (EBIT) was EUR -2.2 million (EUR -0.3 million)

·Profit for the period was EUR -2.3 million (EUR -0.8 million)

·Earnings per share were EUR -0.08 (EUR -0.06)

Operating cash flow was EUR 1.1 million (EUR 2.7 million). The company’s equity ratio was 78.7% (52.8%), and liquid assets, including short-term liquid investments, were EUR 21.0 million (EUR 2.9 million).