Kassu and Antti have given their comments on the company’s board deciding on yet another “profit distribution” for this year.

Springvest’s board has decided to distribute an additional dividend of 0.05 euros per share for the financial year 2025 and a capital repayment from the fund for invested unrestricted equity of 0.05 euros per share, totaling 0.10 euros per share.

Kasper and Antti have given their comments on Springvest’s new strategic cooperation. Springvest announced on Tuesday that it had signed a preliminary agreement for strategic cooperation with the service company HT Growth Partners Oy (HTGP). The goal of the cooperation is to create a service package aimed at growth companies, which supports companies not only in financing but also in operational growth. The arrangement also includes HTGP’s offer to purchase Springvest shares at a price higher than the current market price.

“As part of the overall arrangement, negotiations are also underway regarding a share arrangement consisting of a strategic share purchase and call options, in which HTGP has offered to buy Springvest shares from certain shareholders of the company at 8.464 euros per share.”

The transaction then materialized today:

Block trade at 2:22 PM. In the trade, 103,854 shares were sold for 8.464 euros each.

Donut Lab’s CEO also developed artificial superintelligence (=ASI. More advanced than AGI, which other AI companies haven’t achieved either) in the spring of 2025. Everyone can imagine how much this adds to the guy’s credibility:

You are certainly right about the delivery. Although he is a Doctor of Science in battery technology, his communication skills didn’t even earn him a seat on a remote rural municipal council.

The track record still seems quite flimsy. Fortunately, Springvest isn’t some unnamed Finnish “defense sector serial acquirer,” so the stock has a clear foundation.

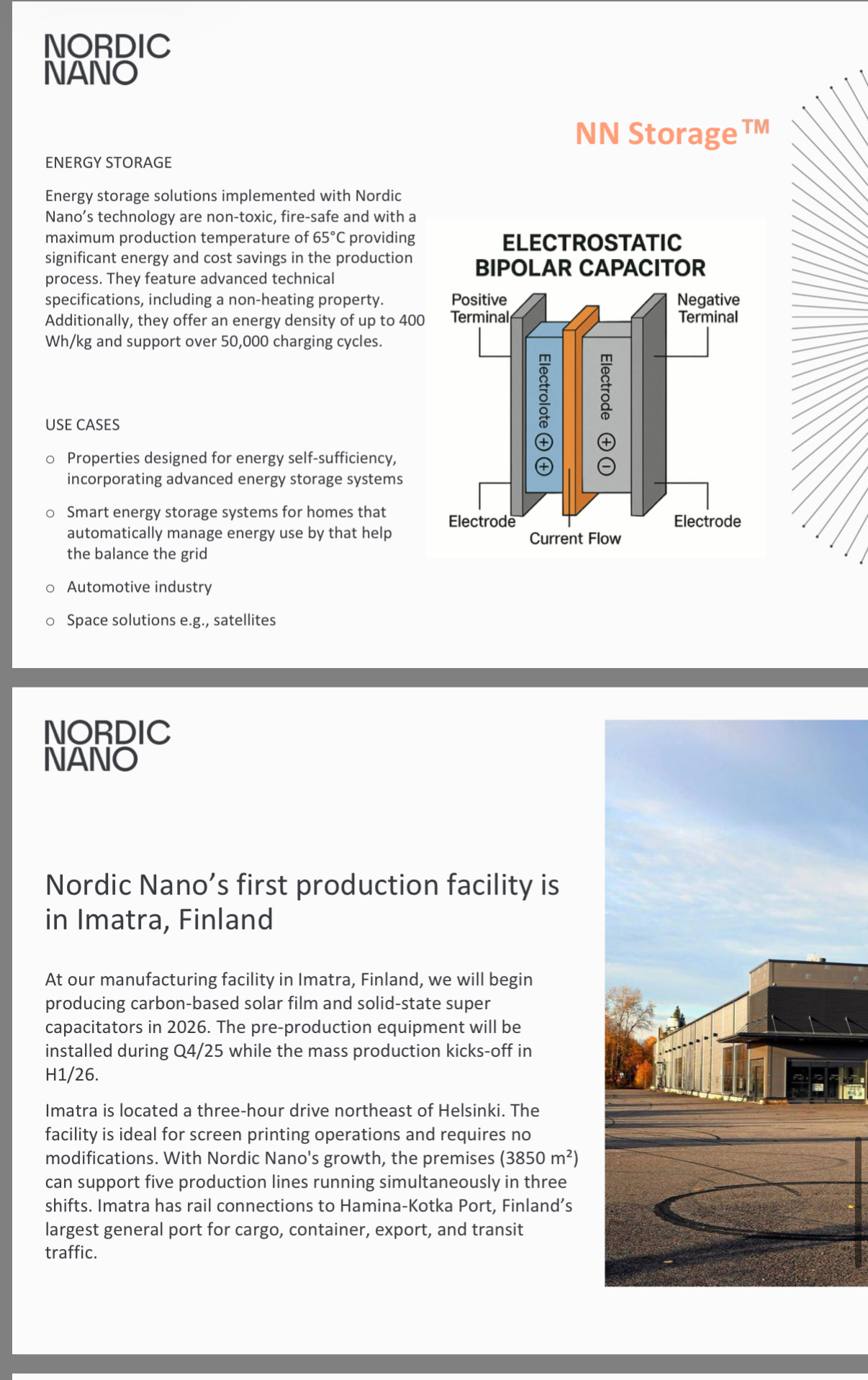

I’m not buying or selling. If things don’t pan out, it will drop back down in the short term. If the battery, against all odds, works as advertised, it’s a whole different ball game. The stock will hit ten either way, but the timeframe varies.

In my opinion, the most important slide in the video is this:

So these guys can achieve in two years what Tesla, CATL, BYD, or Panasonic couldn’t. All it took was a handful of ex-Nokians, sales professionals, an investor, and a PhD who defended their dissertation on solar cell technology last summer.

Springvest doesn’t appear to be among the largest owners (Verge Motorcycles); the sixth-largest owner has 0.6% of the shares. That list should have been longer, so there would have been clarity on the size of the holding:

Due to the complex ownership structure and the mystery surrounding IP ownership, I personally wouldn’t invest in Springvest for Donut exposure, even if I considered the invention a sure thing. In a positive scenario, everyone in this setup (Verge, Donut labs, Nordic Nano, etc.) will need additional funding, and it won’t be forthcoming from Springvest. Therefore, ownership will certainly be diluted, especially in the parts of the corporate group where the most value resides.

It’s quite crazy that Springvest’s market value has risen by over 70% since the beginning of the year solely due to a very small ownership stake in Verge, the exact amount of which we don’t even know. Now we at least have the information that the ownership stake is less than the 0.6% mentioned in the 2025 H1 report.

I wonder how many of those who bought Springvest shares based on this Verge/Donut Lab connection have actually purchased Verge’s latest financial statements from the PRH (Finnish Patent and Registration Office) for the price of just over four euros? Or read anything about the company’s past and current structure?

Springvest’s stock has risen by approximately 73.5% since January 5th. The rise is practically based only on this hype surrounding Donut Lab, even though some on Shareville are already justifying the stock as cheap even without Donut Lab. If Springvest owned even that 0.6% of Verge according to the latest interim report, the market is pricing it at approximately4 billion. This is an incomprehensible valuation, considering the company’s previous sales, losses, and, in my opinion, other likely indications that the SSB IP most likely belongs to someone other than Donut Lab, provided the product is real. That battery technology would be the most revolutionary thing here, and perhaps next would be those electric motors integrated into the wheels, but the latter innovation is unlikely to be that valuable since there is no market for it yet like there is for batteries.

It would seem that the market is wrong. Some people might be in for a rude awakening.

I’m inevitably forced to think about trimming my position. I’ve personally viewed Springvest as a case that yields, well, next to nothing during bad times, but during upturns, it can provide exposure to small startups that I wouldn’t otherwise have access to with my limited capital or expertise. In any case, it’s a high-risk and high-volatility investment.

In my opinion, the current valuation isn’t supported by the company’s overall portfolio. I definitely wouldn’t buy more right now. With the return percentage on my own position already over 100%, the sell button is on my mind morning and night.