All the world’s music online is at the same time both a beautiful dream and a huge nuisance:

Almost a hundred thousand new songs appear on streaming services daily.

“About half of the tracks were listened to less than ten times a year, and about a quarter 10-100 times a year. In total, there were about 140 million such tracks. Conversely, only 500,000 different tracks were listened to over a million times a year.”

“Luminate did not report this time how many tracks were not listened to even once last year. According to estimates based on previous figures, this ‘dead weight’ would constitute up to 25% of all tracks.”

Here are Christoffer Jennel’s pre-comments as Spotify releases its results on Tuesday, Feb 4.

EDIT: Changed Finnish comment to English.

Spotify will release its Q4 results on Tuesday, February 4, before the market opens. We expect the report to focus particularly on gross margin, MAU/subscriber growth, monetization, and Q1’25 guidance. Following the stock’s strong performance after the Q3 report, we believe there is little room for disappointment in the report. Furthermore, Netflix’s strong Q4 subscriber growth has likely raised expectations for a similar Spotify result in the MAU/subscriber metric. However, we are not making changes to our MAU/subscriber addition forecasts before the report.

Ja tässä olisi vielä kunnolliset kommentit Q4:sta Inderesin tapaan, eli tässä ois analyytikko Christoffer Jennel:in ajatuksia Q4:sta.

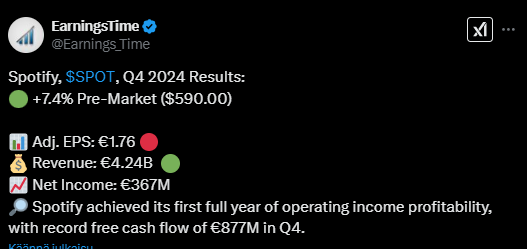

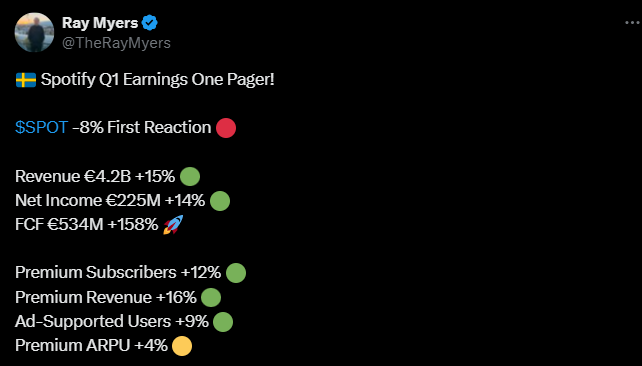

Spotify reported an overall very strong, better-than-expected Q4 print. The report had many bright spots, most notably an impressive MAU and subscriber beat. In addition, the profitability exceeded our and Street’s estimates by a wide margin, showcasing strong operational efficiency. The guidance for Q1’25 topped consensus and our estimate, especially on operating income. However, despite robust user growth in Q4, the guidance suggests a modest sequential increase of +3m MAUs and +2m subscribers. Nonetheless, Wall Street appears focused on the strong Q4 results, with shares up 8% in pre-market trading. Following the better-than-expected report, we see some upward pressure on our estimates, primarily on margins and FCFF.

EDIT:

Finnish text replaced with the English version, the company report itself “remained in English”.

Spotify’s Q4 report was very strong overall and better than expected. The report had many positive aspects, such as a significant beat on MAU and subscriber numbers. Considering this, the Q1’25 MAU/subscriber guidance was cautious and indicated moderate growth of +3m MAU and +2m subscribers. However, management remains confident that user growth will be in line with the last 4–5 years in 2025. Furthermore, the Q1’25 EBIT guidance was clearly above our and the consensus forecast, indicating strong operational performance. Thanks to the better-than-expected Q4 report, we have raised our forecasts, especially regarding profitability. Despite these adjustments, the stock’s continuous price increase keeps the valuation tight. Therefore, we still see the risk/reward ratio as insufficient and reiterate our reduce recommendation while raising our target price to $535 (previously $470).

Below is a video where Jesper and Christoffer chat in Swedish about Spotify’s Q4.

If you know even a little Swedish, it’s worth watching and listening. However, you can also get automatically generated subtitles (in any language), which are… tolerable.

Spotify released its Q4 report on February 4, and we summarize it together with analyst Christoffer Jennel. What does Christoffer consider to be the most important insights from the report? What did CEO Daniel Ek actually say during Spotify’s earnings call? And how should Spotify use its strong net cash position?

On the Inderes Nordic channel, there are also videos in English!

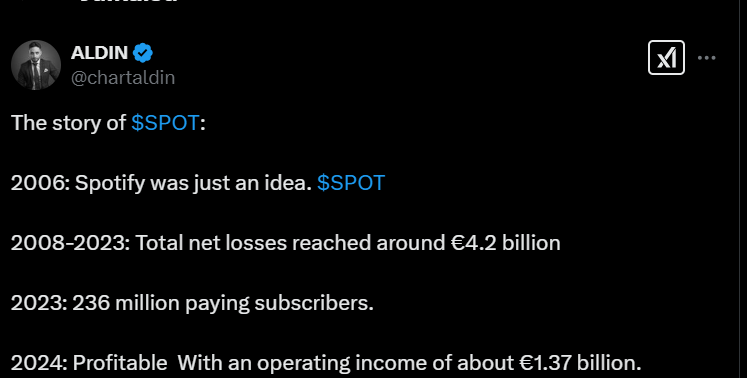

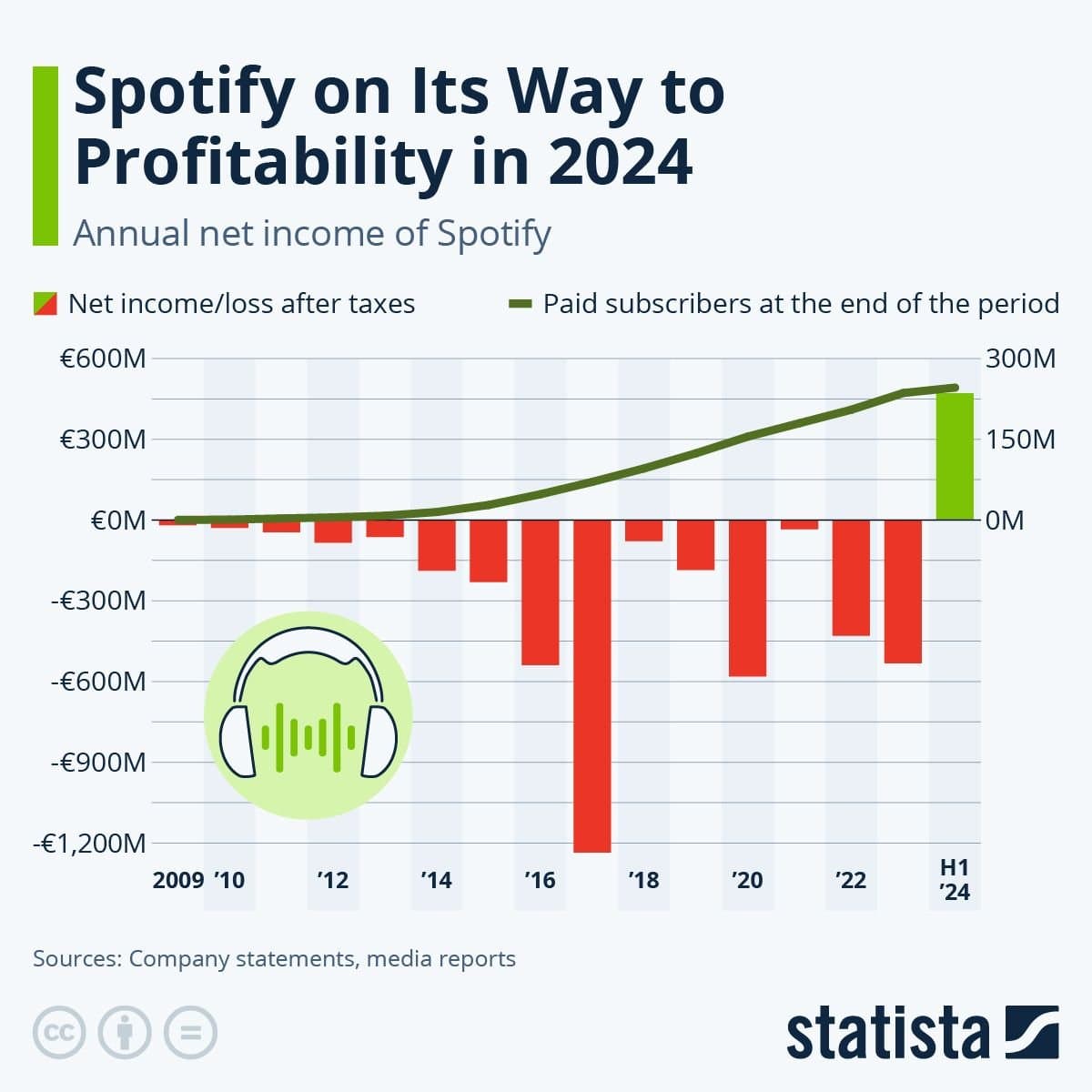

Perhaps one of the most incredible stories is that this has become a profitable product. Spotify is also almost synonymous with music, just as YouTube is with videos.

The biggest fear is probably that the music industry wants its share of these profits and will pressure Spotify. I don’t know if anyone can say what the streaming services’ agreements with music rights holders are like?

I would say that the threat is precisely the opposite. And mainly from the perspective of how much content, for example, is becoming the services’ own production, how, for example, AI-generated content will take over the field in Spotify’s guided consumption behavior, etc.

On the record industry side, we have four major players: the three major record companies and Merlin, representing the indies. Spotify pays royalties based on consumption, a certain percentage of its revenue. And in addition to the record companies, the parties to the agreement are, of course, separately the owners of performing rights (composer/lyricist/publisher).

@Tomi_Valkeajarvi is this podcast based on Inderes’ own material, or what is its added value compared to generating a similar podcast yourself using available public material?

Of course, this saves time if you collect and upload the material, and generate and publish the podcast.

Yes, I agree that the data collection (where sources might be chosen more wisely than, for example, by me), uploading them, and publishing them in a shareable format for everyone brings good added value.

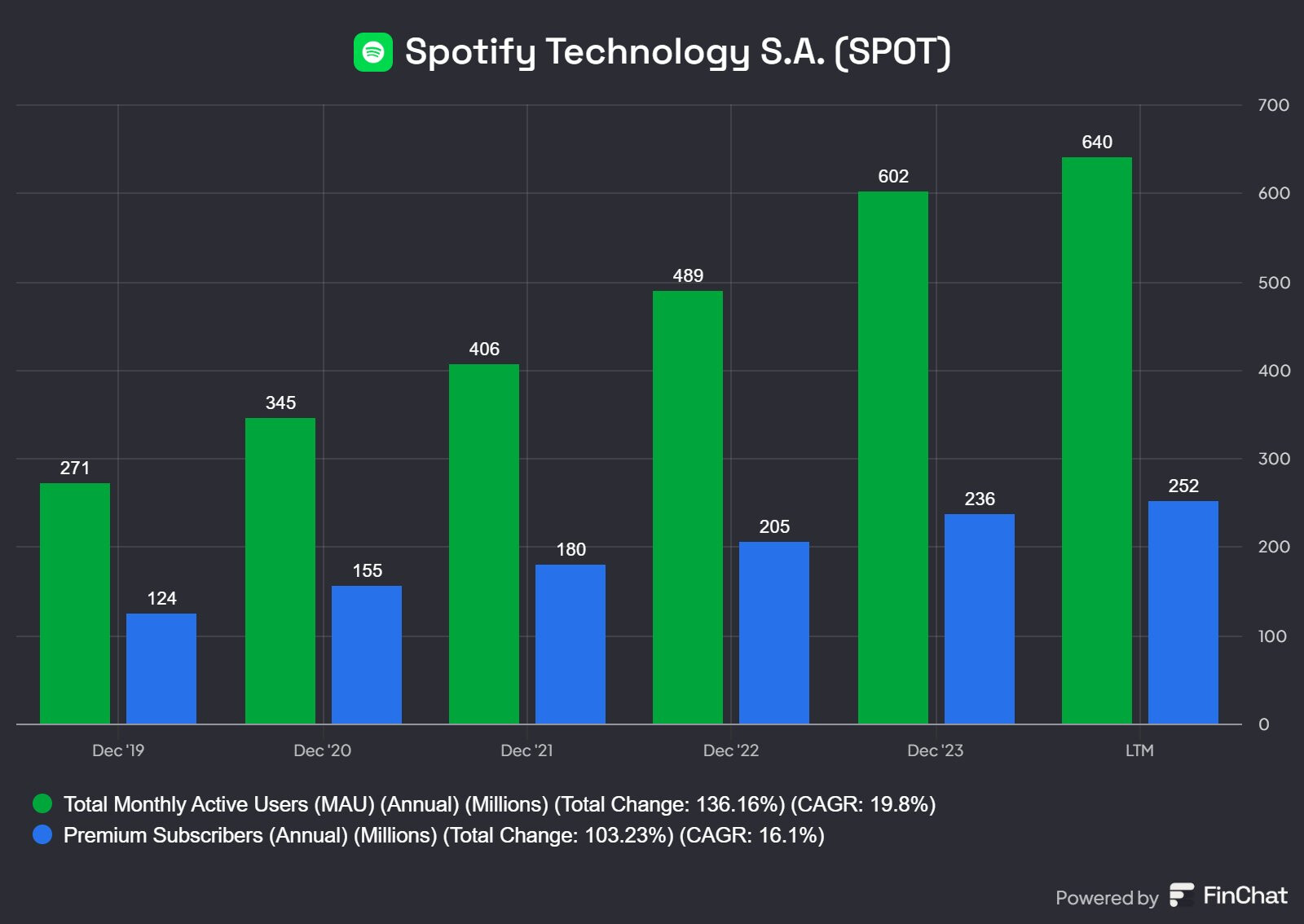

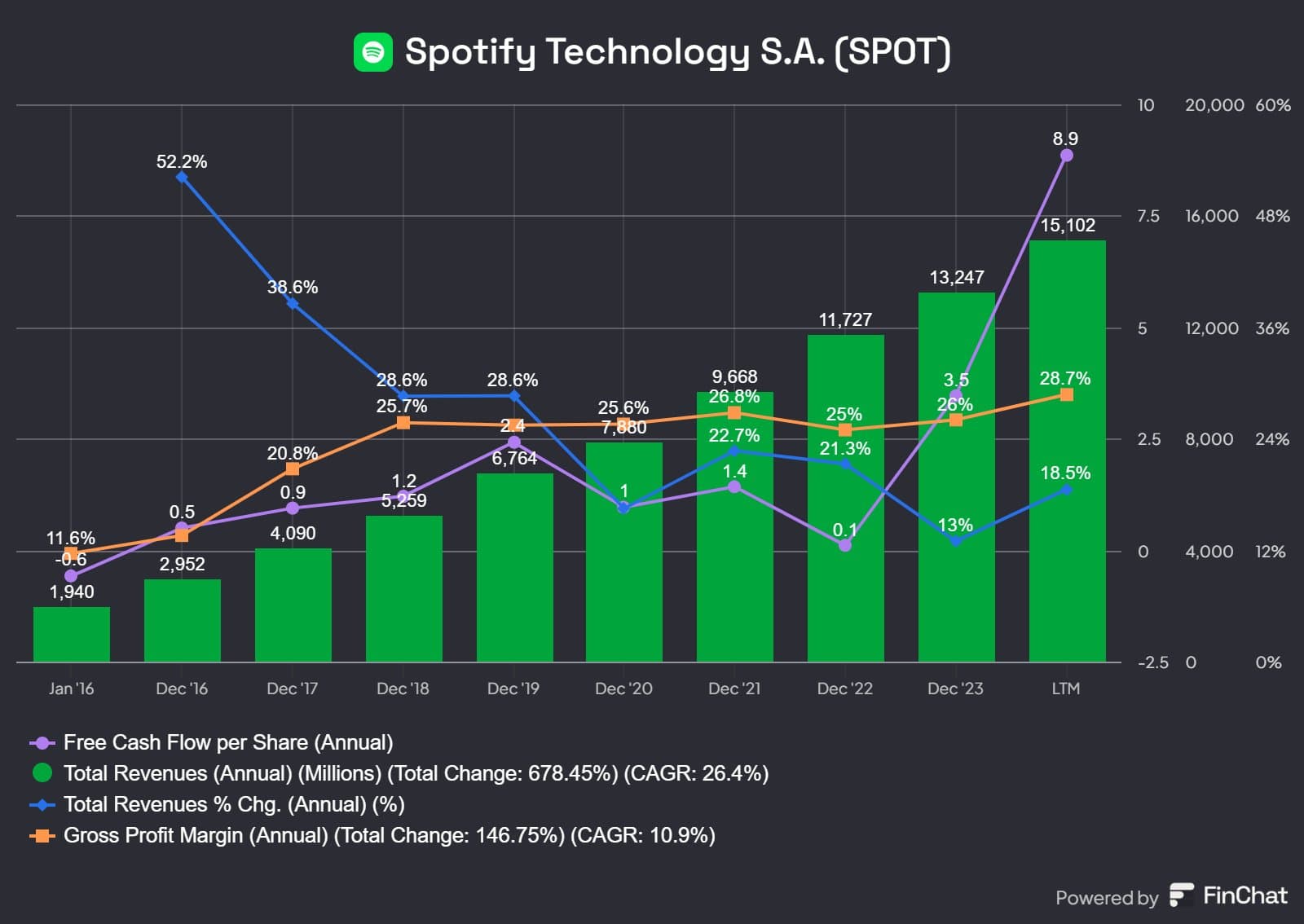

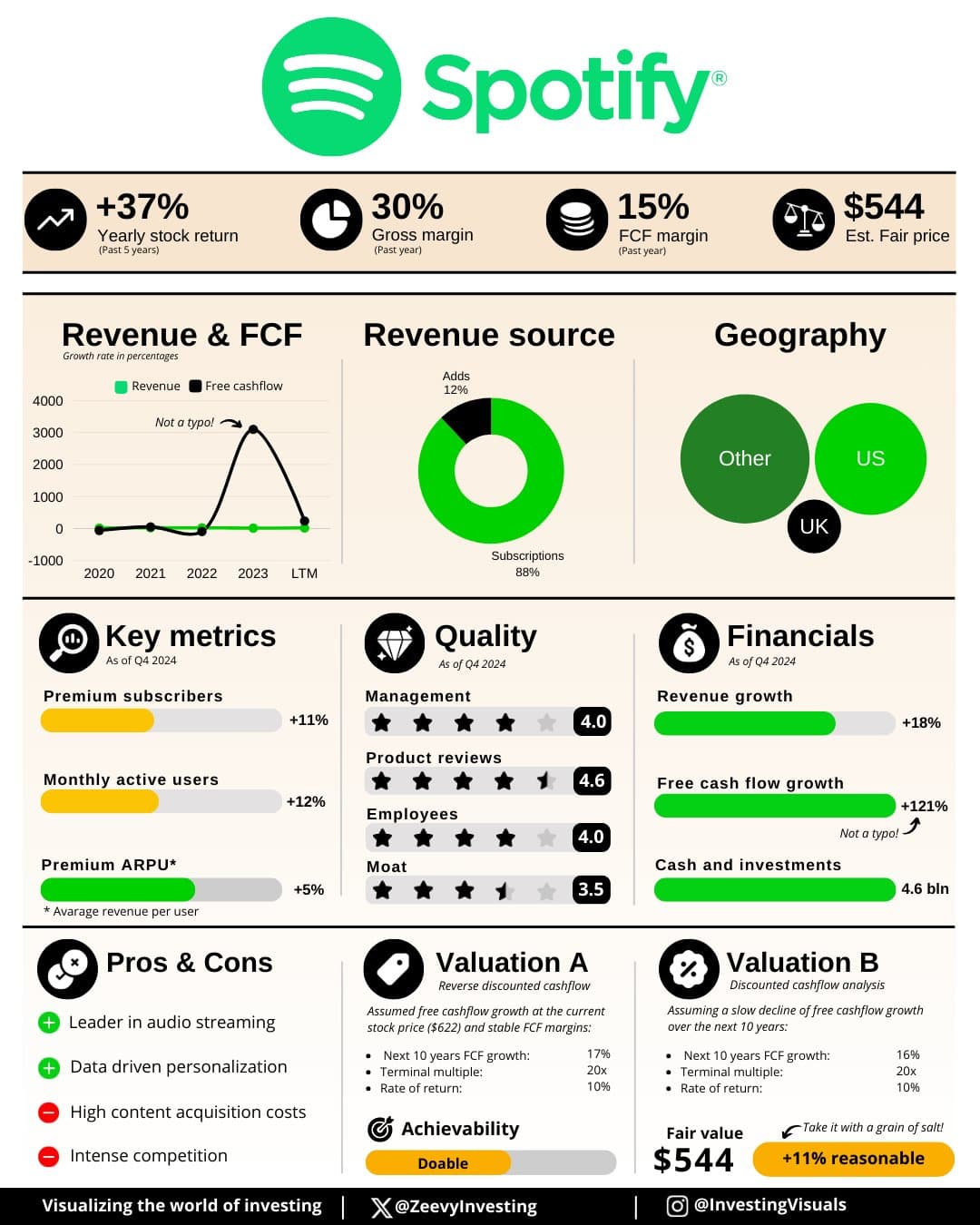

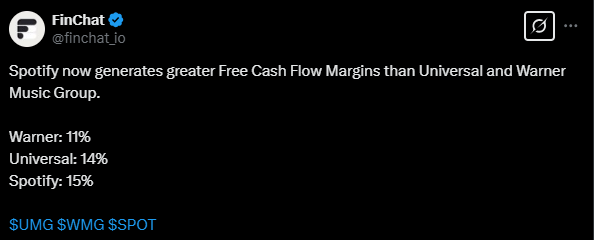

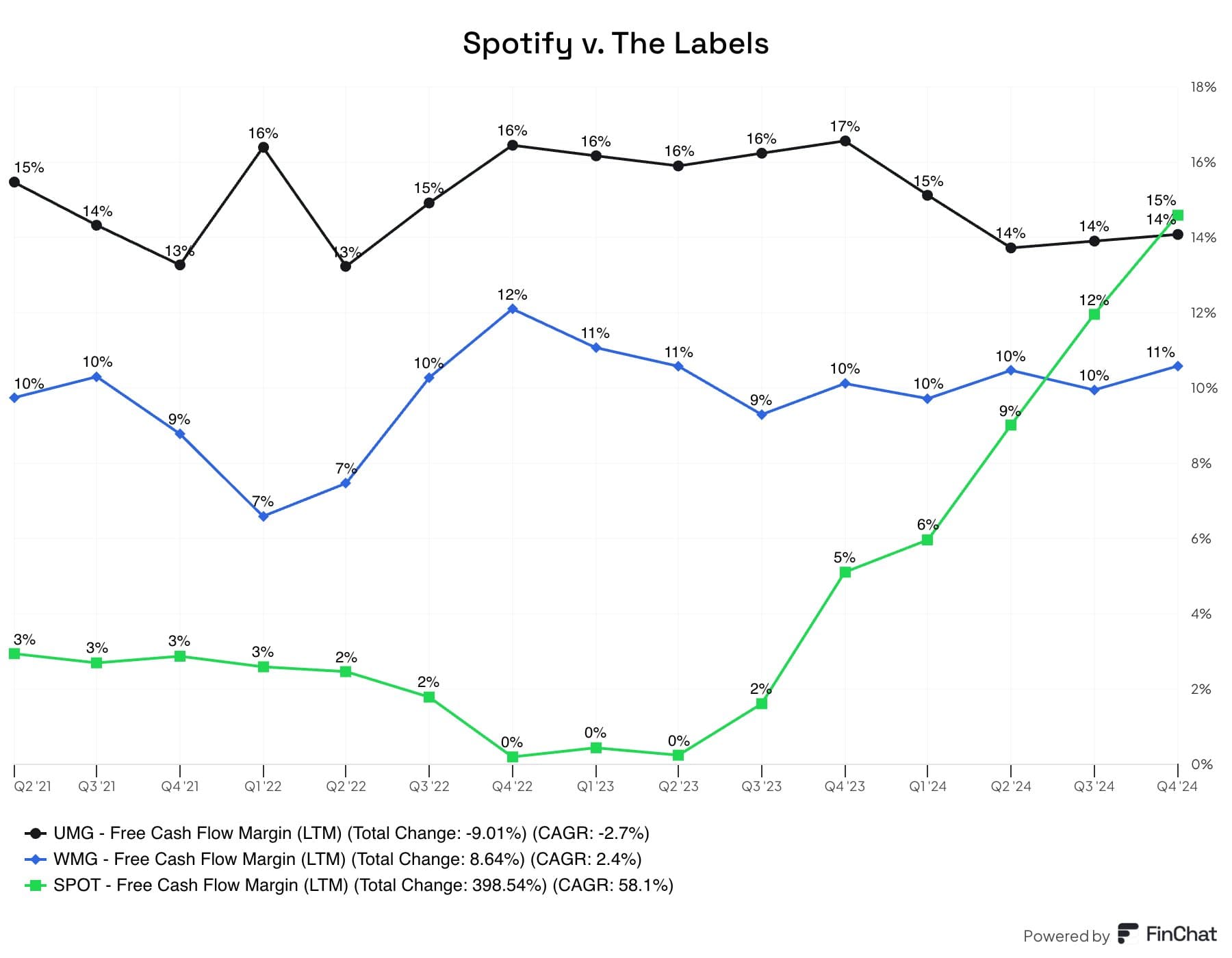

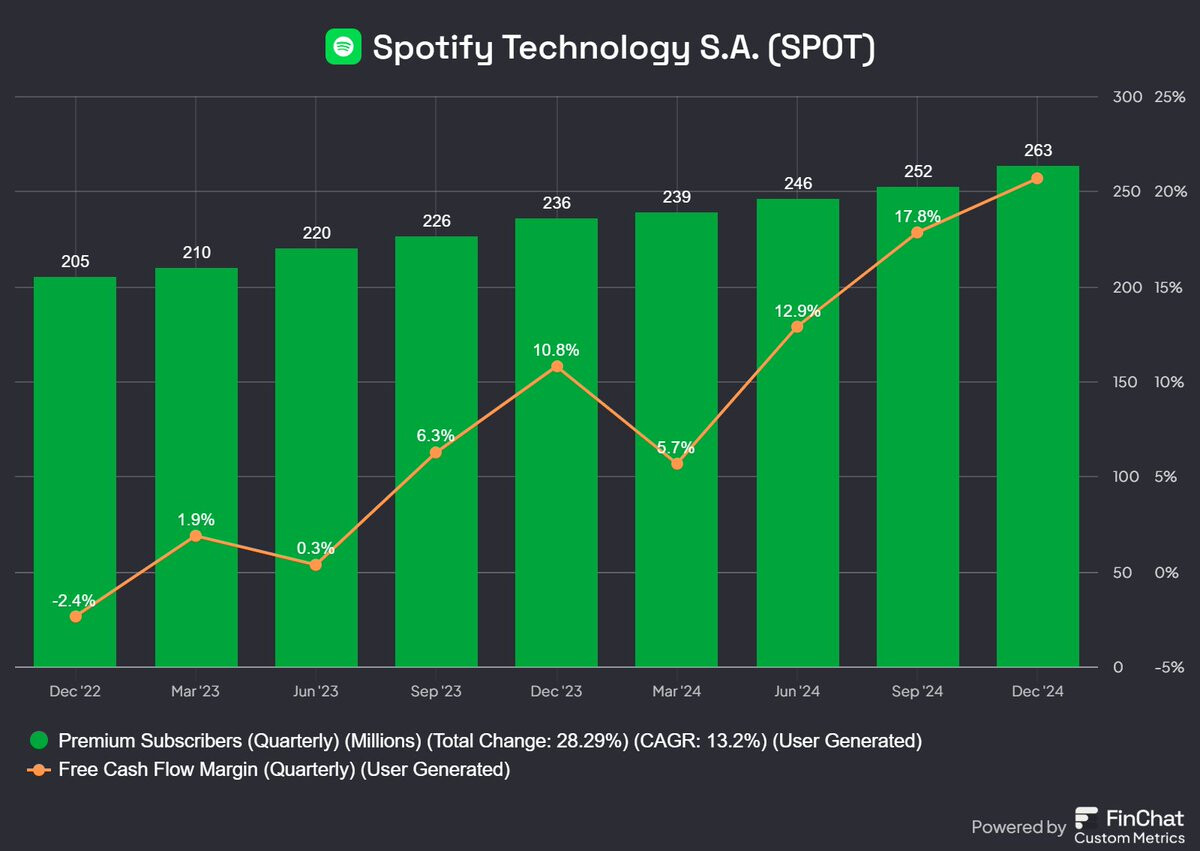

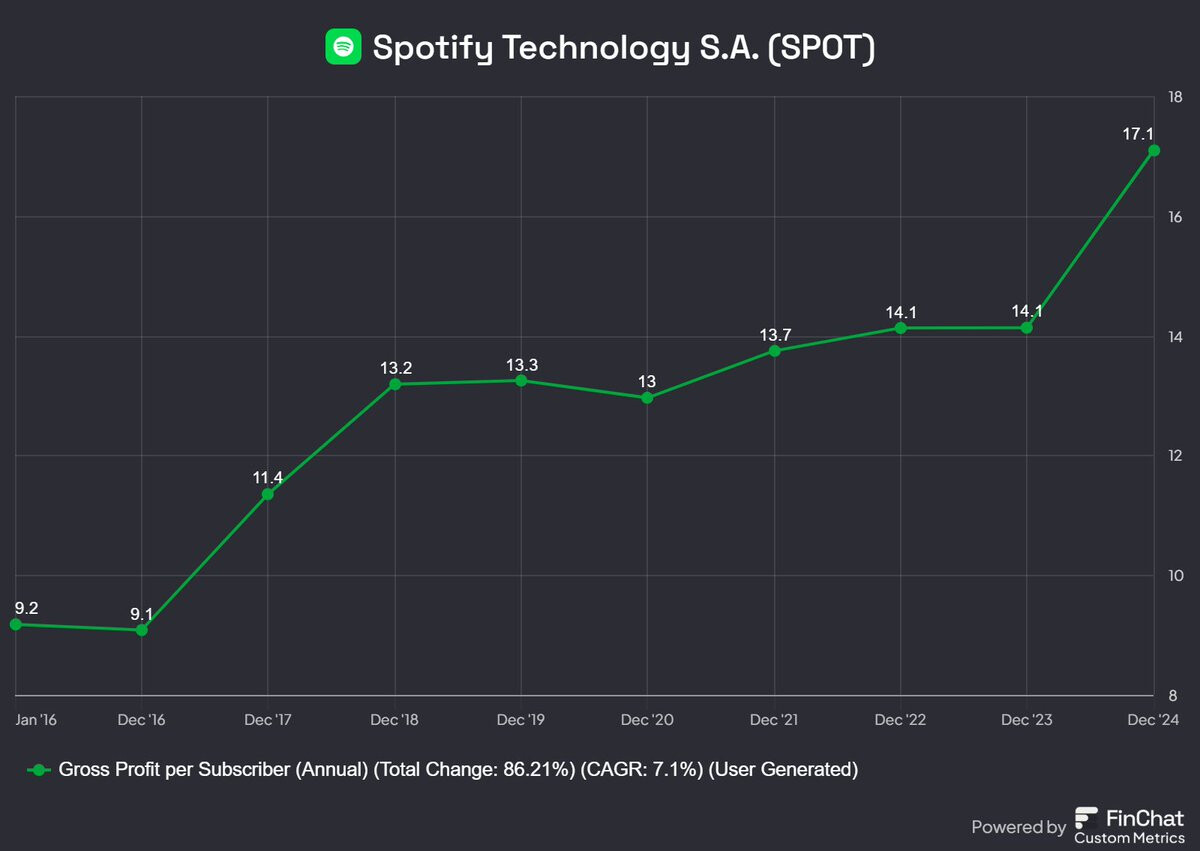

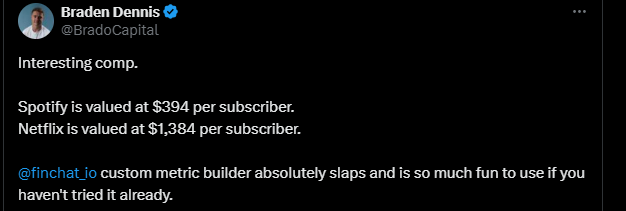

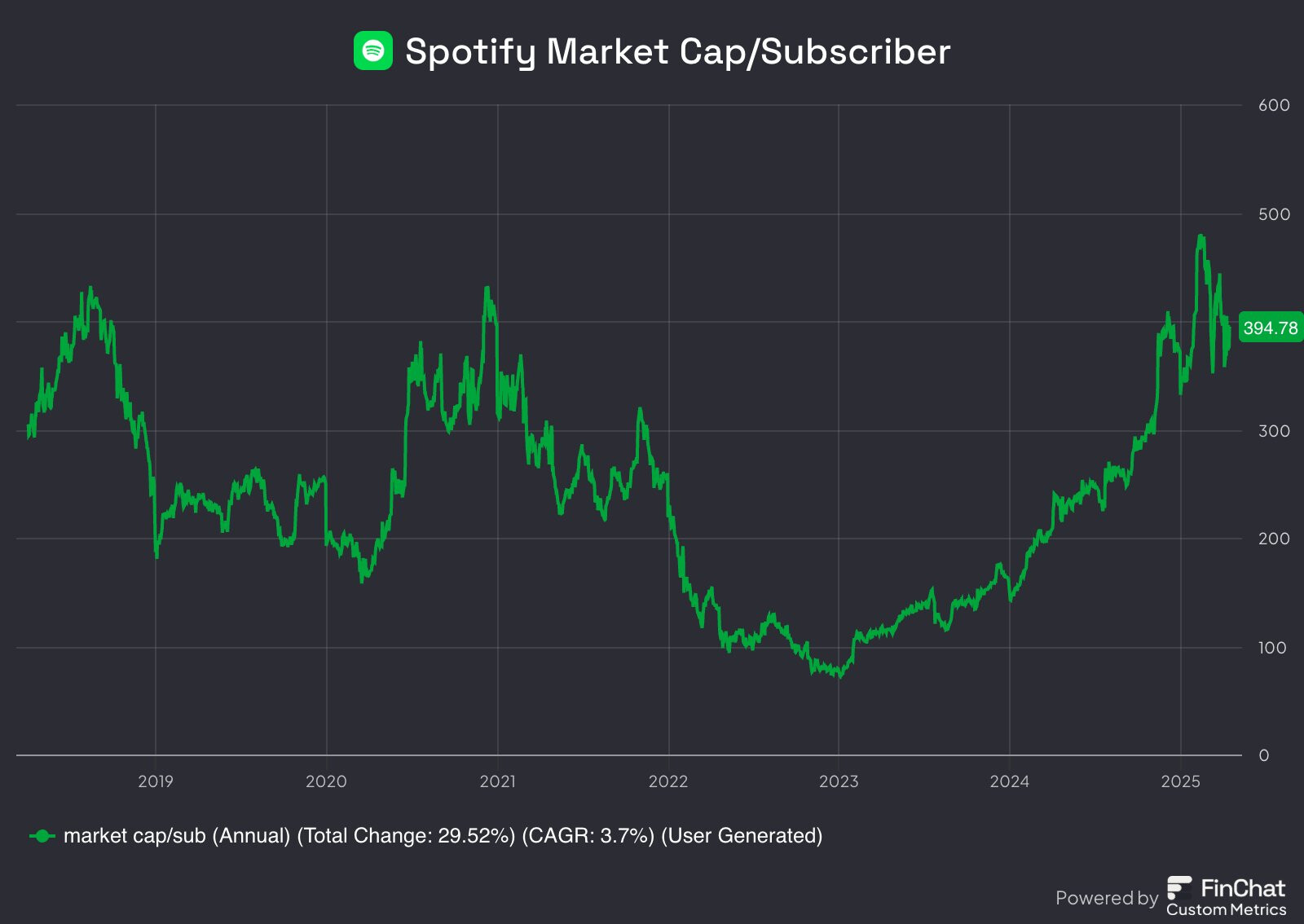

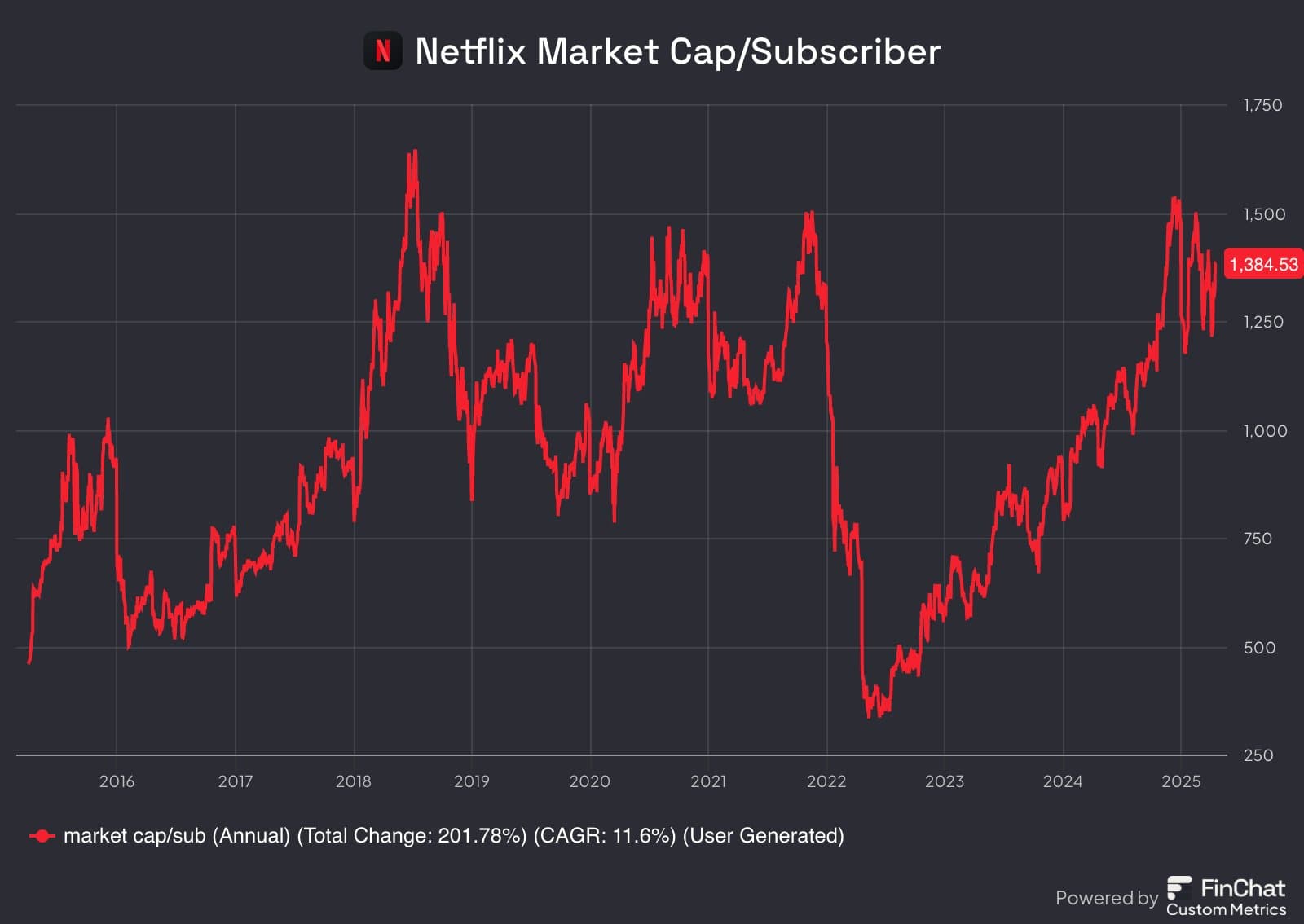

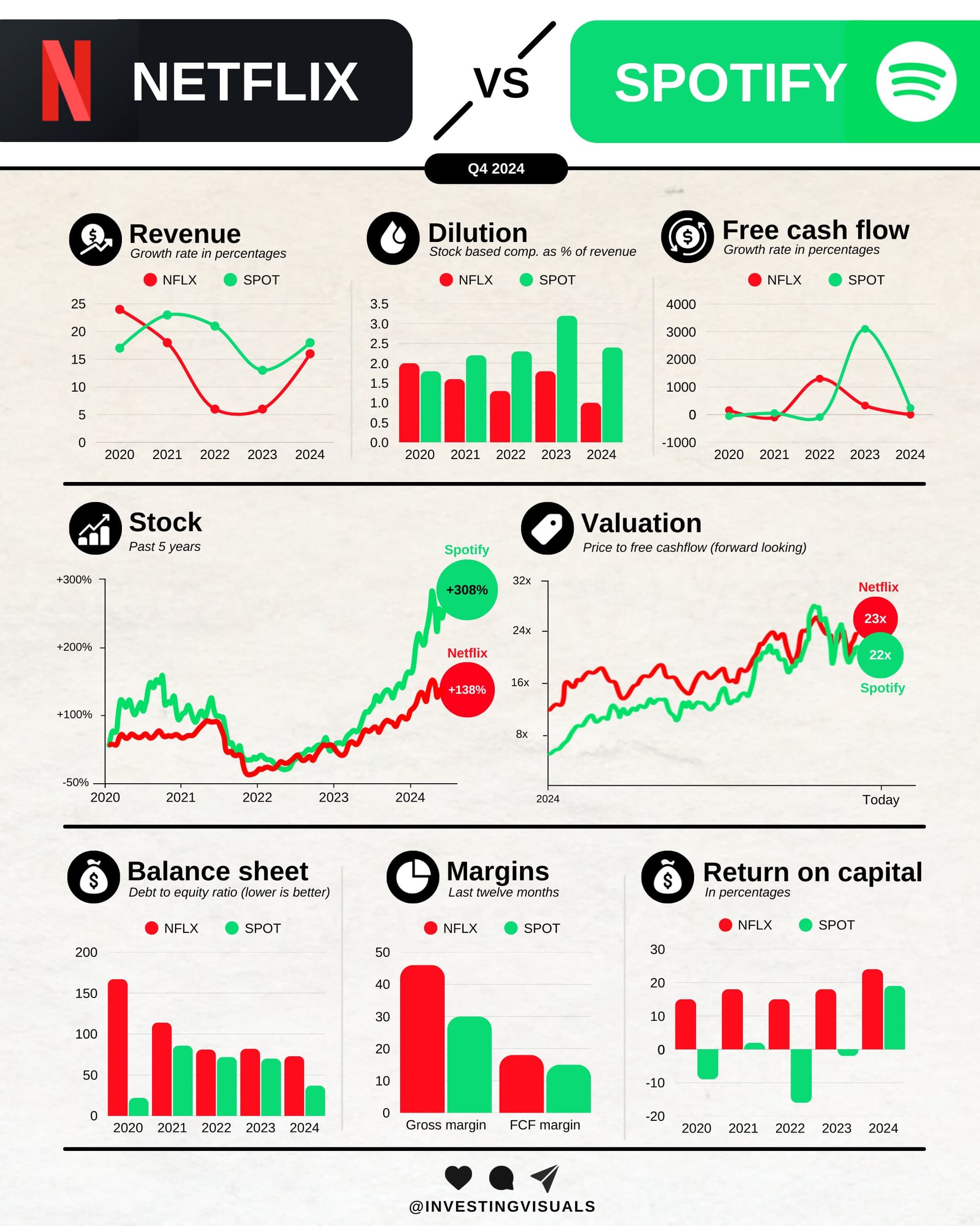

According to the tweeter, Spotify’s competitive advantage is clearly visible in the fact that as paying subscribers grow, cash flow and margin per subscriber have also increased.

Since 2016, the margin per subscriber has grown by 86 percent, and the company generates over 20 percent free cash flow.

Tässä on Jennelin ennakkokommentit Spotifyn Q1:sta ajatellen

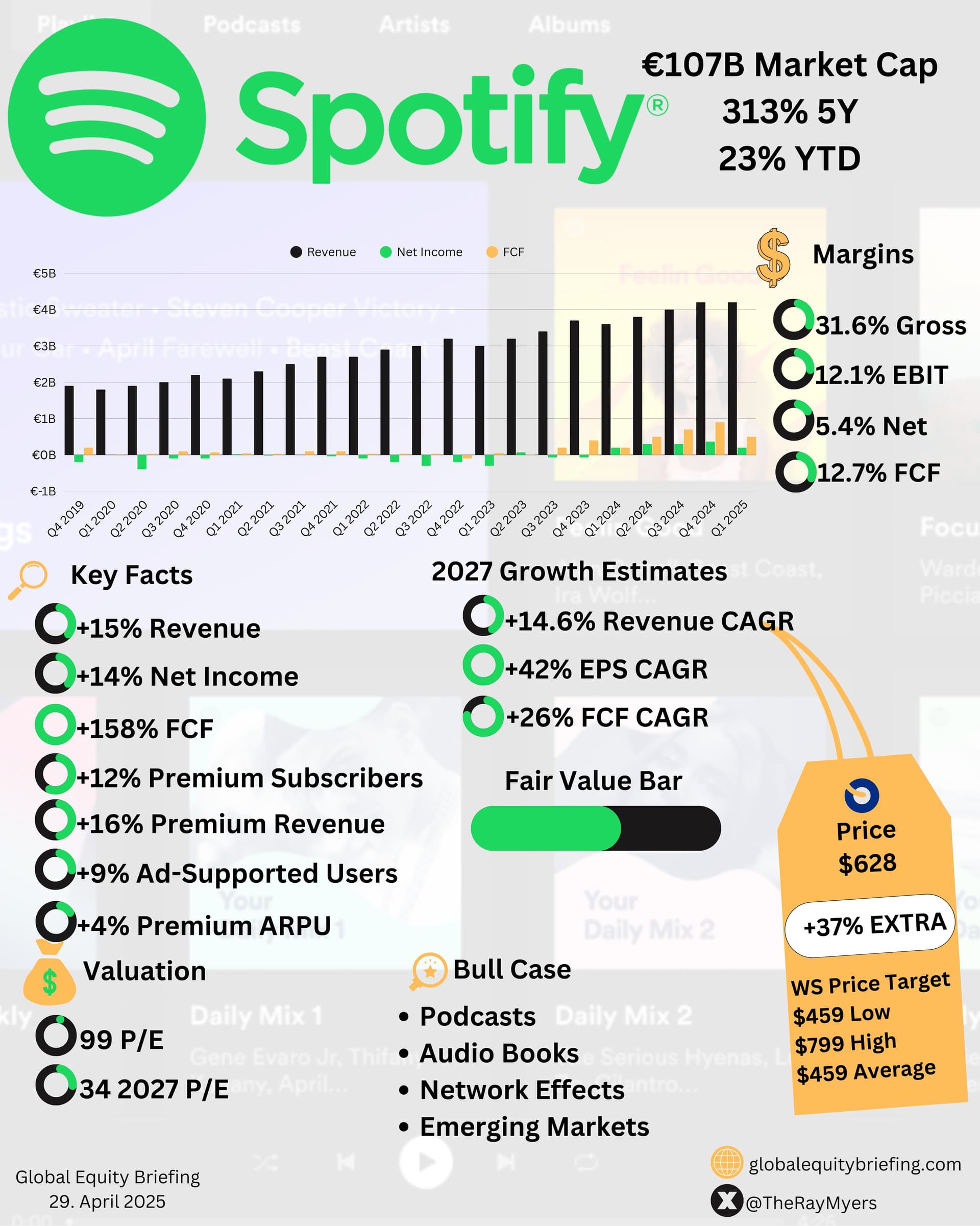

Spotify will report Q1 earnings on Tuesday, April 29, before the market opens. The company enters earnings season with strong momentum and a macro environment that, while uncertain, likely has minimal impact on its core business. With subscription revenue dominant and user engagement rising, fundamentals remain solid despite a weaker ad market and ongoing geopolitical risks, which we believe are behind the stock’s relative resilience compared to the broader market. We’ve kept MAU/subscriber forecasts steady ahead of the Q1 print but made minor adjustments to ad revenue and near-term EBIT estimates, reflecting more conservative projections for advertising revenue and incremental social charges. Subscriber growth, product expansion, gross margin, and pricing strategy remain key pillars of the investment case heading into the Q1 report.

Spotify is reportedly raising its subscription prices this summer in several countries in Europe and Latin America, but the United States will be exempt from the price increases.

Prices are expected to rise by about one euro per monthly subscription.

I’m not sure if the article below will be accessible to everyone, but the main message is in my summary.

Spotify grew strongly in the first quarter of the year. Revenue increased significantly in all regions, and profitability improved. Gross margin and operating income rose to record levels, as did free cash flow.

The number of monthly users grew across the board, especially in Latin America and other developing countries. The number of paying subscribers also clearly increased this year.

Spotify’s Q1 print was broadly in line with our expectations, though net subscriber additions surprised positively. However, guidance for Q2’25 came in somewhat below both our and Street’s estimates, particularly on MAUs, revenue, and operating income. That said, the guided +5m premium subscriber additions (q/q) stood out as a clear positive, beating our expectations. We think this underscores the strength of Spotify’s value proposition even amid macroeconomic headwinds and soft consumer sentiment. However, following the Q1 report, we have slightly lowered our estimates, primarily due to FX-effects, with currency-neutral estimates remaining largely intact. The share price has been resilient despite a broader market downturn and continues to trade at rich levels. As such, we continue to view the risk/reward as insufficient and reiterate our Reduce recommendation and, when adjusting for the effects of a weaker USD to EUR, we increase our target price to USD 570 (was USD 535).