Silver price is currently -33%, interesting to see how Sotkamo’s share price reacts on Monday. The price gains from the start of the year have been wiped out.

4 Likes

Hi,

It’s nice that during this busy start to the year, there is at least some commentary regarding the company. Right at the start, I want to express my thanks to the company’s analyst for the careful and thorough reports, which help in understanding this company amidst share price fluctuations and silver price volatility. Some say they have sold and some say they have bought. A certain Canadian investor has been quietly loading up on the company in several batches, and it seems their name can be found quite high on the list. I would like to ask those of you following the company how you determine the company’s mineral and ore reserves while the price of silver lives a life of its own, and does extending the mine’s lifespan have significance regarding your investment decisions? It would be nice to hear different perspectives. At least a ten-year extension for Finland’s only silver mine: more to be mined has been found in Sotkamo | National | Yle

3 Likes

I’m asking as I don’t know the company in much detail: what kind of commercial agreements does Sotkamo Silver have? Does the product being sold have some form of price hedging, or have any delivery agreements been made?

This has a significant impact on when the rise in silver prices starts to show in the company’s earnings and revenue.

2 Likes

They have price hedging; if I recall correctly, the lag is around 2 months, so Q4 prices won’t be fully reflected in Q4.

Here are Aapeli’s preview comments, as Sotkamo releases its Q4 results on Friday ![]()

We expect the company’s production volumes to have remained at a weak level in the final quarter, reflecting the guidance downgrade in November. However, we expect the company’s revenue and earnings to have been supported by the sharp rise in silver prices, although the full impact of this will only be reflected in the figures for the early part of the year. The main point of interest in the report is the production guidance for the current year, which we expect to indicate clear growth compared to last year.

2 Likes

If it’s not clear from tomorrow’s earnings report, Aapeli, could you dig out the current silver price hedging from Jalasto? It seems to be a mystery to everyone. This, however, significantly impacts the result.

1 Like

The answer was that last year the hedging horizon was 2 months, and about 1 month so far this year. Longer-term hedging has likely become more expensive.

2 Likes

As an addition to @JL12’s message, they promised in the Q&A to explain this in the form of a separate slide in the next webcast. And admittedly, these hedges are still a bit unclear to me as well, which is partly because the hedges are applied to a “portion” of production that hasn’t been detailed more specifically than this. Additionally, in Q4, the hedges were not in use the whole time for reasons related to covenants. Well, I suppose we’ll be wiser regarding this after the next webcast.

5 Likes

Here is a company report from Aapeli regarding Sotkamo Silver’s Q4 results. ![]()

Sotkamo Silver’s Q4 production fell clearly short of our expectations, but the operating figures were in line with our forecasts, supported by a strengthened metal market. For the current year, the company expects its production to grow, but the range is still wide. Based on the provided guidance and comments regarding the beginning of the year, we lowered our production forecasts for the current year, but we kept market parameters and forecasts for the coming years largely unchanged. With a strengthened financial position and a favorable market situation, we lowered our required rate of return, but changes in our sum-of-the-parts remained moderate. Reflecting this, we revise our target price to SEK 3.1 (prev. SEK 3.0). In our view, the current share price is largely dependent on the favorable price development of silver before there are concrete signs of a sustainable increase in production levels. Against this backdrop, we see the stock’s risk-adjusted expected return as very weak and lower our recommendation to Sell (prev. Reduce).

11 Likes

Adding a recent interview with the CFO related to the topic. Interview with Sotkamo Silver’s CFO Tommi Talasterä - Analyst Group

4 Likes

Can anyone comment on the new board members proposed at the general meeting? Do they bring expertise to the work or more board professionals draining the gravy train?

The Nomination Committee proposes the re-election of board members Eeva-Liisa Virkkunen, Kimmo Luukkonen, Jukka Jokela, and Joni Lukkaroinen. In addition, the Nomination Committee proposes Mikko Keränen, Miika Heiskanen, and Vesa Heikkilä as new members of the Board.

New Board Candidates

Mikko Keränen: Brings exceptionally strong operational mining expertise. He has served, among other roles, as the director of Agnico Eagle’s Kittilä gold mine (Europe’s largest) and as the Research and Innovation Director at Kajaani University of Applied Sciences (KAMK). Keränen has a deep understanding of the daily operations of a mine, environmental matters, and the local operating environment in Kainuu. He is a full-fledged mining professional.

Vesa Heikkilä: Represents the company’s long-standing tradition and owner stewardship. Heikkilä has served for years on Sotkamo Silver’s nomination committee (also as its chairman), nominated by, among others, the companies of the company’s founder, Timo Lindborg. His role on the board is likely to ensure the realization of major shareholders’ views and to maintain the company’s internal historical knowledge.

Miika Heiskänen: For Heiskänen, direct, public references to heavy mining industry or large holdings are more limited. Typically, these “less known” additions, however, bring specific expertise to the board that is needed in addition to operational mining directors – for example, in law, finance, or information systems.

That’s a quick AI overview.

1 Like

Hello,

Here’s another video published by Jussi Halme this morning concerning mining companies. GOLD $4500, SILVER $75 – What’s Happening to Mining Stocks? (BULL SCENARIO). It also discusses the situation of Sotkamo Silver from different angles. Additionally, it’s worth checking out Kauppalehti’s article about CEO Mikko Jalasto and his current thoughts on Sotkamo Silver. It’s behind a paywall. Stock soared, 16,000 new owners in an instant – Mikko Jalasto leads Sotkamo Silver, for which a sudden price rally opened up a completely new game | Kauppalehti

1 Like

A video about Sotkamo Silver was described: ![]()

4 Likes

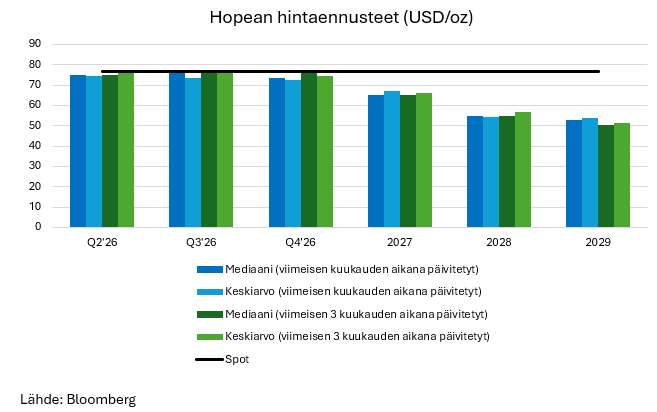

Could you dig up a chart for the forum on the consensus forecast for silver prices for the coming years?

3 Likes

Here’s a very quickly put together graph regarding consensus estimates. The table includes current median and average estimates for Q2-Q4’26, as well as for the years 2027-2029. I included in the graph both estimates updated within the last month and those updated within the last three months, which are currently largely in line with each other. For this year, consensus expectations are for development at approximately the current spot price level, while a declining trend is expected for the coming years. The consensus estimates are also somewhat in line with our latest estimates. However, it is worth noting that estimates can change rapidly.

7 Likes

“In practice, 10% changes in our silver price assumptions throughout the forecast period would raise/lower the sum-of-the-parts value by just under SEK 0.7/share at current high prices.”

Has the model calculated that the price of silver will remain at $50 “forever”? So, if the forecast is changed so that $60 is the new price for the longer future, the target price in the model would increase by approximately SEK 1.4/share?

2 Likes

Thanks for the great question. Currently, the life cycle of the Silver Mine in our model extends to 2035 based on the company’s latest exploration results. Extending the life cycle beyond this is certainly possible through new exploration programs in the longer term, but we have not yet included these in the production forecasts. Thus, for SoS, the forecasts do not have the same perpetual assumption due to the limited life cycle of the mine as for “normal” companies. In practice, that 50 USD/oz applies in the years 2029–2035. On the other hand, the sensitivity refers to the entire forecast period (2026–2035), so in that sense, such a large change would not directly result from that long-term change (note also the high discount rates and their impact in the long term), but it would still be significant. I also emphasize that this sensitivity is based on the euro-denominated prices of silver, with everything else remaining constant. Thus, it should only be regarded as indicative, as a change in only one parameter would not be very likely (e.g., the historically clearly negative correlation between the price of silver and the EUR/USD exchange rate) or their linear change. At the same time, it is also good to remember that forecasts and, through this, sensitivity analysis assume production to stabilize at over 1.3 million ounces per year in the longer term.

5 Likes

Thanks for the comprehensive answer! I’d still like to ask if the value in the calculation would be affected if, for example, the uncharted western part of the mine yielded an additional 5 years of life?

1 Like

Our production forecasts do not yet include this western potential. Thus, extending the mine’s life to the west, downwards, or both would have a positive impact on forecasts and the sum of the parts, all other factors remaining equal. The potential commissioning of the western side could also have a production-increasing or at least stabilizing effect, even if the mine life does not immediately lengthen (mine life extension is often a gradual process). As such, there should also be exploration potential in the Silver Mine area for future life extensions. This naturally requires sufficient funding and that production volumes can be sustainably increased, and the risks of chronic production problems do not materialize, so that mining is economically viable even in potentially weaker metal market conditions.

7 Likes