A search for the word SoFi seems to yield exactly one result on the forum. That hit was from some SPAC thread almost a year ago. This disruptive and relatively small growth company is one of the largest positions in my portfolio. I find the company interesting, so let’s try to bring it to the attention of others with its own thread and a comprehensive introduction. Here you go.

Background

SoFi Technologies is an American financial technology company. The company went public in 2021 through a SPAC listing. SoFi, also known as Social Finance, was founded in 2011 at Stanford University. Its purpose was to provide more affordable financing for students’ studies, for which it received two million dollars in funding from alumni. The company quickly raised more funding, and its operations expanded rapidly, though the first few years revolved around student financing. In 2014, mortgages were introduced, and a year later, personal loans. In the same year, SoFi was the first American fintech company to raise a billion dollars in funding at once, which came from Softbank. Since then, SoFi has also launched accounts, cards, investments, and, of course, cryptocurrencies in line with modern trends, offering consumers a nearly full portfolio of banking products.

The ‘Technologies’ in the name primarily refers to the Galileo platform, which SoFi acquired in 2020 for 1.2 billion dollars. Galileo is a core banking platform used by, among others, Robinhood, Wise, and Chime. SoFi Bank, on the other hand, is emerging as the company merges with a small Californian bank it acquired. This arrangement will grant SoFi an official banking license, which reduces SoFi’s dependence on other banks and provides the opportunity to operate like a real bank. Which it would then be. So far, only preliminary approval has been received, but final approval was already expected by the end of last year. There has been a news blackout for a while, but perhaps we will be wiser after the Q4 earnings release.

SoFi has an NFL stadium bearing its name in Los Angeles, where the LA Rams and LA Chargers play. In less than a month, this year’s Super Bowl is scheduled to be held there, so visibility is guaranteed. SoFi customers are offered benefits at SoFi Stadium. The opening ceremonies of the 2028 Olympics will be held at the stadium, but as I understand it, sponsored stadium names are not used in the Olympics.

How is the company doing?

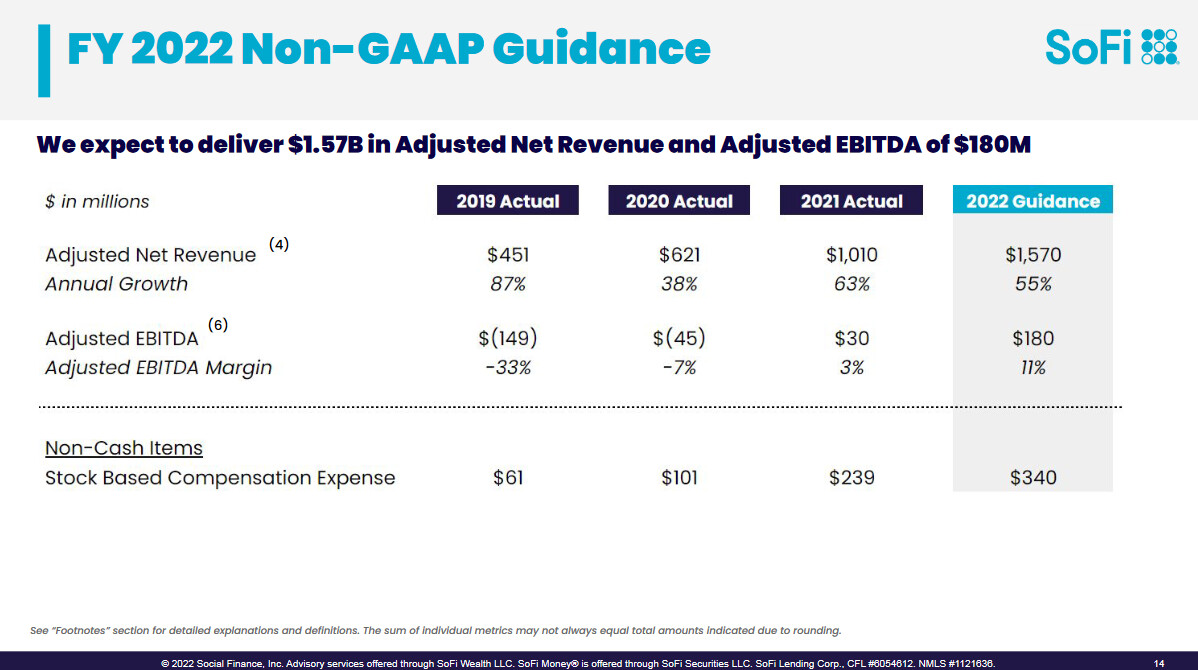

The latest available figures are from Q3. I’ll link them here for everyone to examine in more detail. In short, growth is strong by many metrics. YoY customer count grew by almost 100%. Losses are being made, but growth is prioritized, and achieving a profitable result is not far off.

Management

I’ll link SoFi’s leadership pages for more detailed research. A few words, however. CEO Anthony Noto has a banking background from Goldman Sachs, and he has also been Twitter’s COO and the NFL’s CFO. The rest of the management team has a diverse background from the banking sector, but also from outside it. At face value, they don’t tell me anything, and I haven’t researched their backgrounds and merits in any great detail, but a quick look suggests that they have managed to recruit professionals with diverse backgrounds from various fields into leadership, and the company is no longer run by four students. So, we’ve come a long way from the founding stages.

Differences from competitors

Fintech companies have sprung up like mushrooms after rain, and frankly, I haven’t had the energy to examine all of them too closely. Based on what I’ve read and watched in videos, it seems that SoFi is one of the few, if not the only one, that offers consumers virtually all banking services from a single “window”. Among those operating in Europe, I myself have used Revolut and a couple of others. They work quite well, but their service offerings are very limited. An account, a card, some limited investment activities. That’s it. A similar situation seems to exist across the Atlantic. There are many specialized in one thing or excellent in one service, but a comprehensive digital bank like SoFi has not come across in my research. I believe I would have encountered them if they existed, but I’ll allow for error.

Why I invested?

Banks, and especially banks in the United States, need a good shake-up when it comes to technology. If change doesn’t come from within the industry, it must come from a new and small player. I don’t claim to fully understand the US banking sector from the perspective of an ordinary consumer, but from what I’ve gathered, they are certainly no more advanced there than here in Finland, where the situation is quite OK. A fully digital SoFi could succeed in capturing a good share of the market if growth continues in the same way and there are no major bumps along the road.

SoFi wants to be a digital one-stop bank for consumers. Based on everything, it seems I would be their customer if I lived in the United States. In my opinion, SoFi is well-positioned in the digitalizing banking world. I believe in the company and will keep the shares in my long-term portfolio.