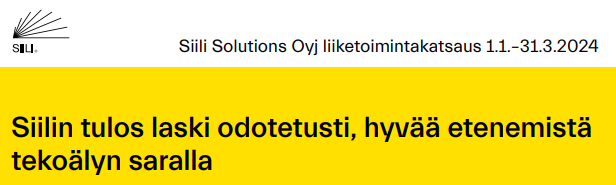

The thread has gone quiet following the share price drop, so here are some AI-related thoughts from Siili’s perspective.

Siili regularly promotes its AI expertise on LinkedIn, which suggests a strong focus on it.

Siili seems to be primarily focusing on AI-assisted software development and its related processes. They recently hired someone who seems very competent as a Principal Consultant for that area.

However, the competition there is tough, as all IT service companies are aiming for the same thing.

In my opinion, the pace of development in the AI space has accelerated, even though NVIDIA generally seems to dominate the news. NVIDIA’s success is mainly a result of the development of actual AI models, and utilizing AI models will boost economic efficiency.

Therefore, I think investing in AI is sensible if done correctly.

In my view, development is rapid in the following areas:

- Development of large models, which requires a lot of data.

- Training models without labels, unsupervised learning and self-supervised learning.

- Use of the Transformer architecture.

Siili has mostly published very general AI articles that don’t really showcase the depth of AI expertise they might have.

I agree with Silo.ai’s blog post stating that an AI team requires at least one person with a very deep technical understanding of AI, plus someone capable of brainstorming AI use cases from a business perspective.

That person with deep AI and trend knowledge could train Siili’s staff, which might be more effective than off-the-shelf AI certificates.

I have practical experience in the effectiveness of sharing this kind of expertise within an IT company.

In my opinion, it is crucial to understand how different AI models process data internally, what their probability calculations are based on, and what kind of corporate data they can be applied to.

The use of the Transformer is growing, and its core concept is performing probability calculations on data relationships in a multidimensional space.

If you only have a minute to learn the principle of the Transformer, watch this:

That video explains the relationships of words in a multidimensional space. Words can be replaced by any data. Words or other data are converted into tokens, represented by vectors, before processing.

This is why the Transformer enables the processing of different types of data (multimodal). This is what GPT-4o’s features (image, speech, text) are based on.

In enterprise architecture, multimodality could, for example, enable the prediction of customer behavior through relationships between very different types of data. The same applies to improving business efficiency based on various data sources.

Collecting data solely for the needs of a single AI application is not sensible; data architecture must be considered from the perspective of the entire company’s business.

Therefore, Siili should, when necessary, also offer consulting for enterprise-level architecture and especially data architecture. Large companies, of course, already have their own enterprise architects, but an AI perspective from Siili’s side could be a competitive advantage.

Personally, I am not convinced when AI companies nowadays appoint a “former Agile coach” to lead the AI department. As a result, the discussion mostly revolves around how ChatGPT could be used to streamline company processes.