I’ve slightly fallen behind on following SDS since selling my position.

Q1 is out, steady plodding. Investment in the future, challenges in profitability.

At least a couple of orders were pushed from Q1 onwards.

https://investor.seamless.se/nyheter/interim-report-for-the-period-january-1-march-31-2022-95110

Interim report for the period January 1 - March 31, 2022

January - March

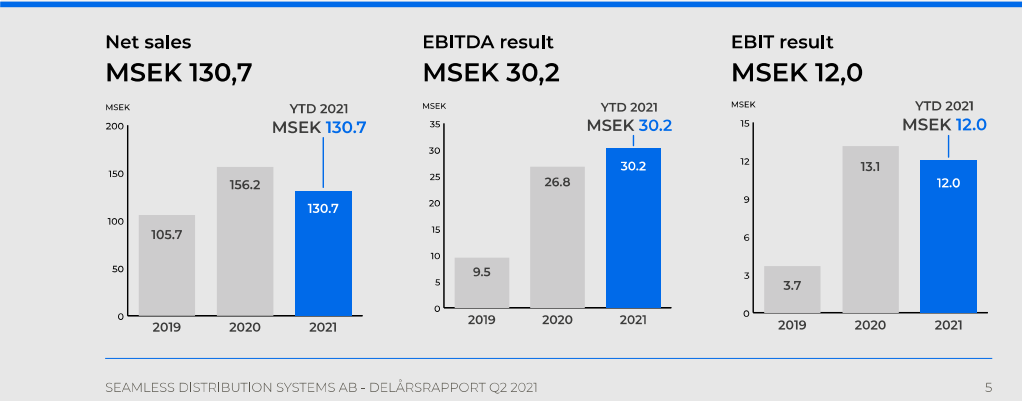

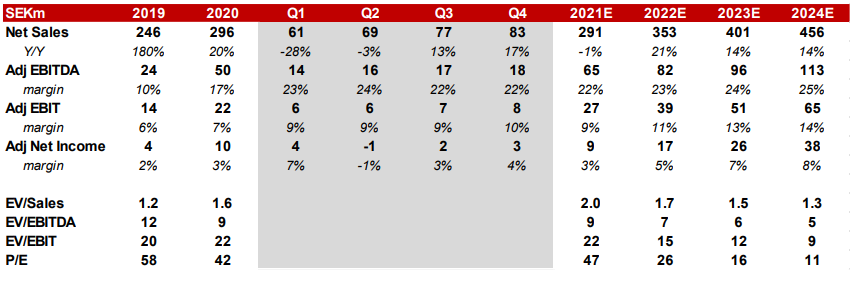

- Net sales amounted to SEK 63.1 (61.5) million, an increase of 2.6% compared to the same period last year.

- EBITDA earnings amounted to SEK 9.3 (13.9) million.

- EBITDA margin amounted to 14.8% (22.6%).

- Profit after tax amounted to SEK -7.9 (3.6) million.

- Earnings per share amounted to SEK -0.8 (0.4).

- Total cash flow amounted to SEK 4.4 (0.9) million.

CEO’s comments

"Intensive start to 2022

Net sales in level with the previous year

Net sales in the first quarter landed at SEK 63 million. This is an increase of almost 3% compared to the corresponding quarter last year, but lower than we had hoped for. The main reason is two large orders, which for reasons beyond the company’s control did not arrive as expected during the quarter. Profitability was thus weighed down by the increased personnel costs with the acquisition of Riaktr and EBITDA was just over 9 million, a decrease of 33% compared to the corresponding quarter in 2021. This again shows that the company’s development cannot be seen on a quarterly basis but requires a longer perspective.

A quarter with investments for the future

A very important activity for the company’s development was the participation in the Mobile World Congress, MWC, in Barcelona in the shift February-March. The company’s management conducted more than 20 high-quality customer meetings with high-level management teams at both new and prospective customers. The newly defined and expanded product portfolio attracted great interest and led to several new business discussions.

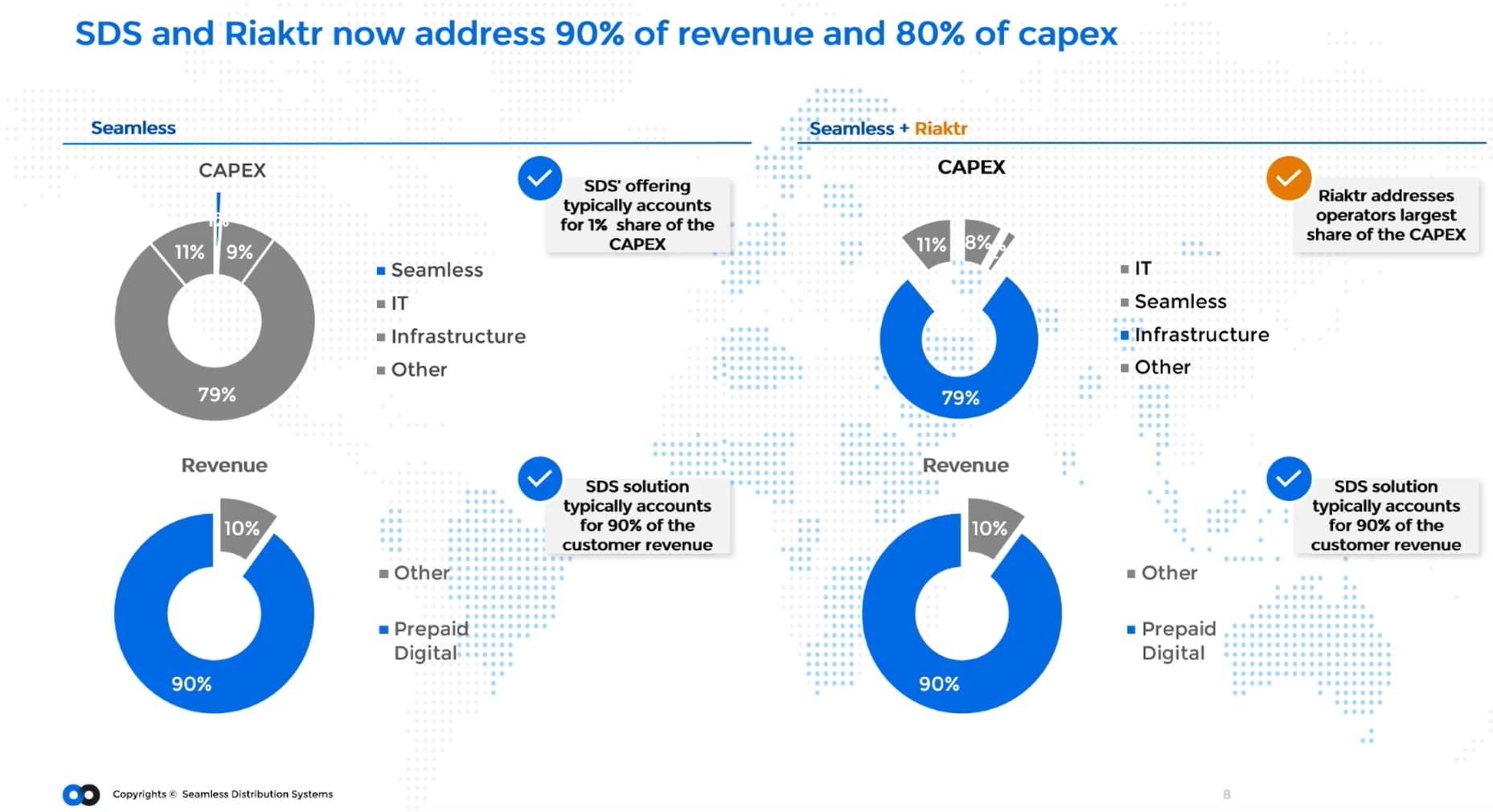

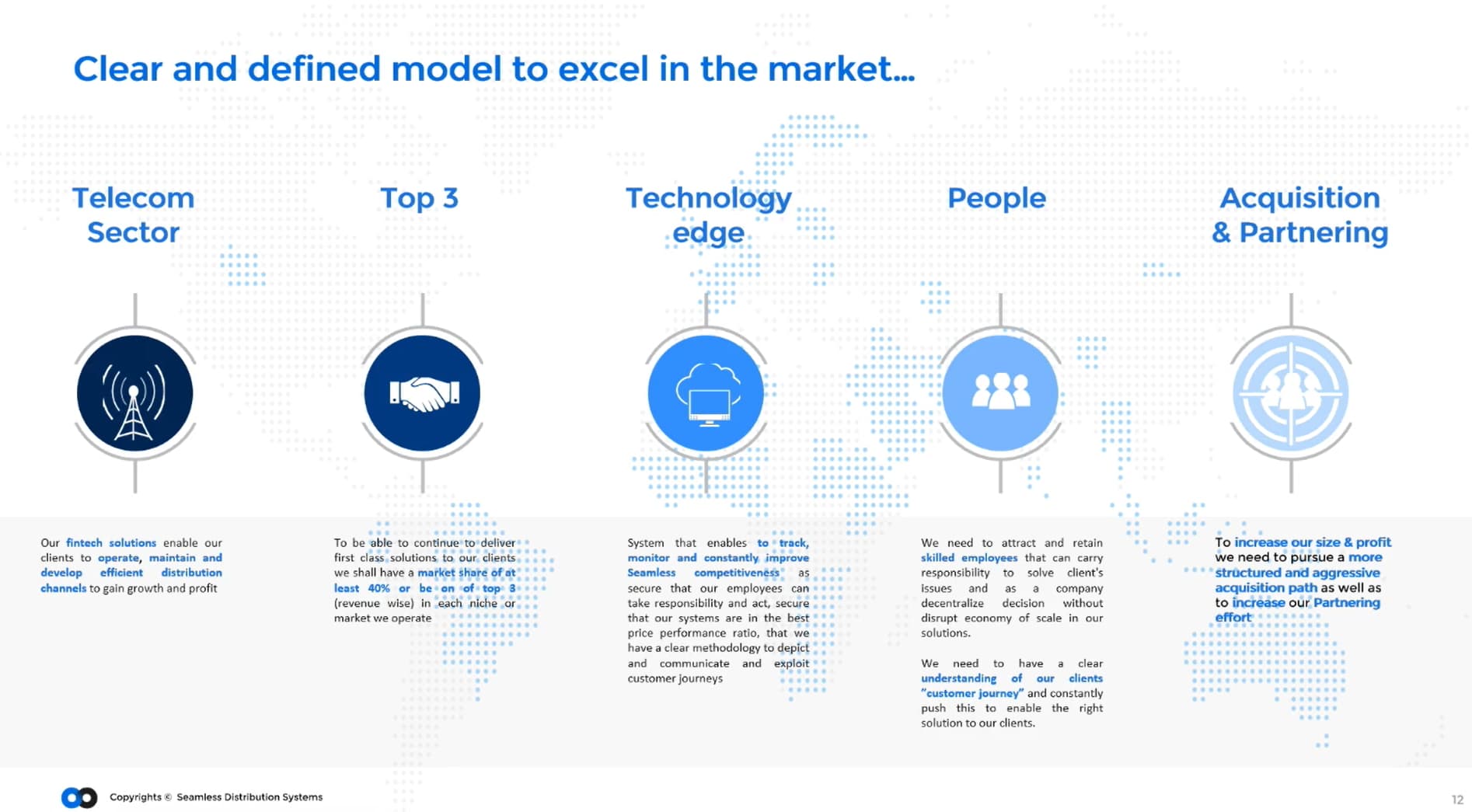

During the quarter, work was completed on the definition of our new product portfolio for the value chain we call Retail Value Management, RVM. Our mobile operator customers depend on the value chain being managed efficiently as a very large part of their revenue takes place through their dealer network. With our expanded and redefined product portfolio, we have clear solutions for all the steps, challenges and growth opportunities that the operator faces in RVM. We currently see no other supplier with such a clear and broad portfolio adapted for RVM - something that was also noticed by the operators we met at MWC.

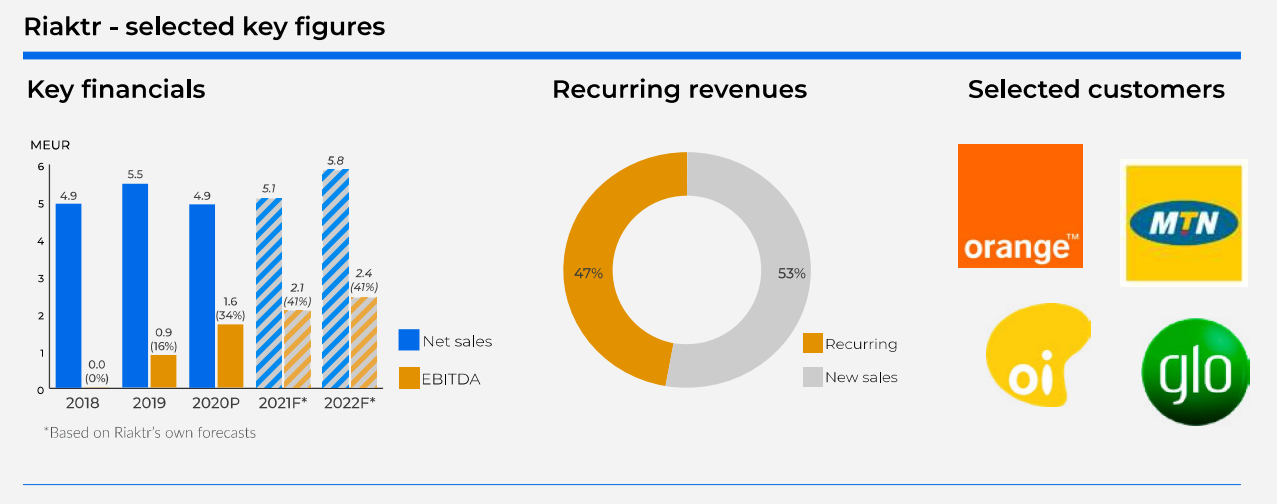

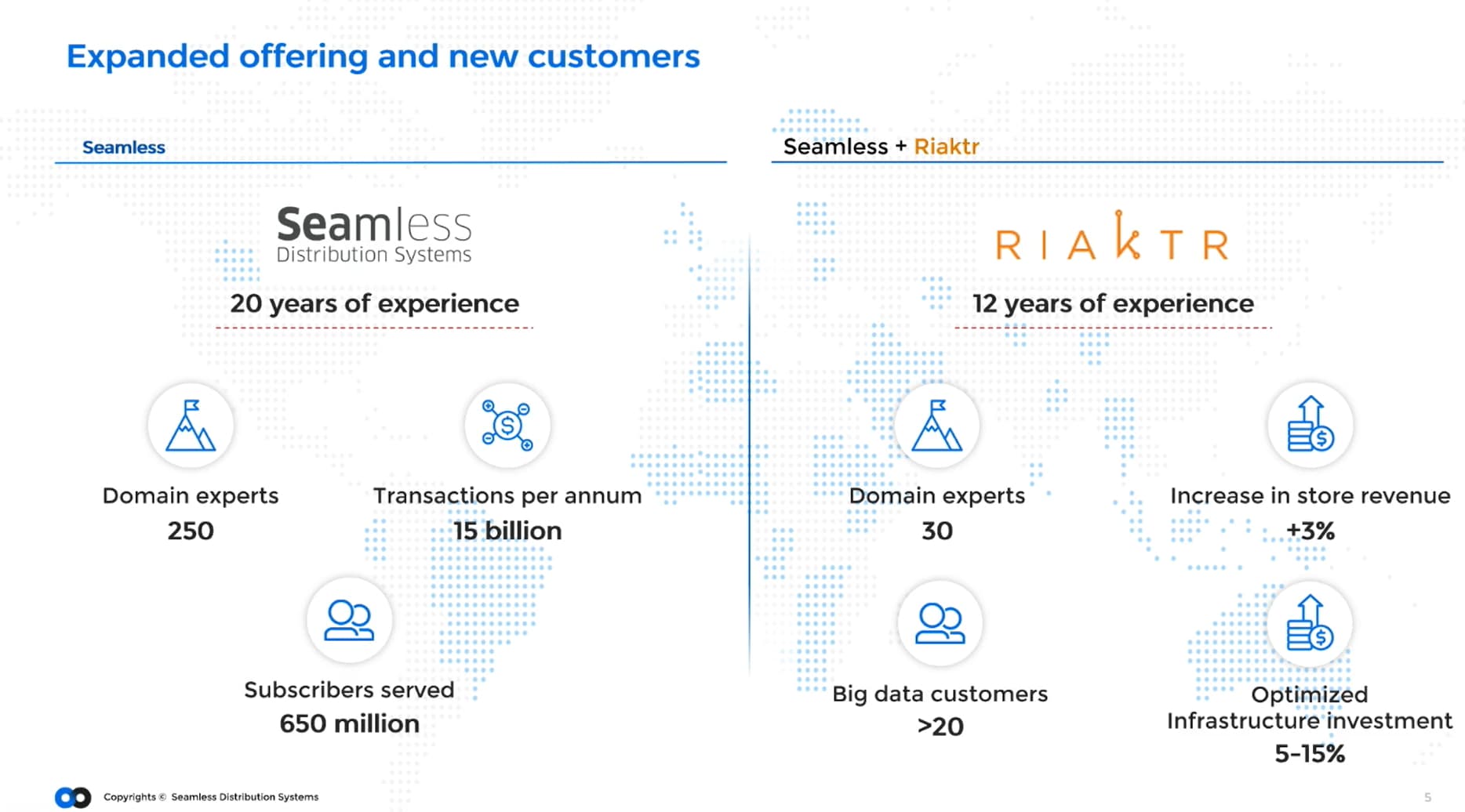

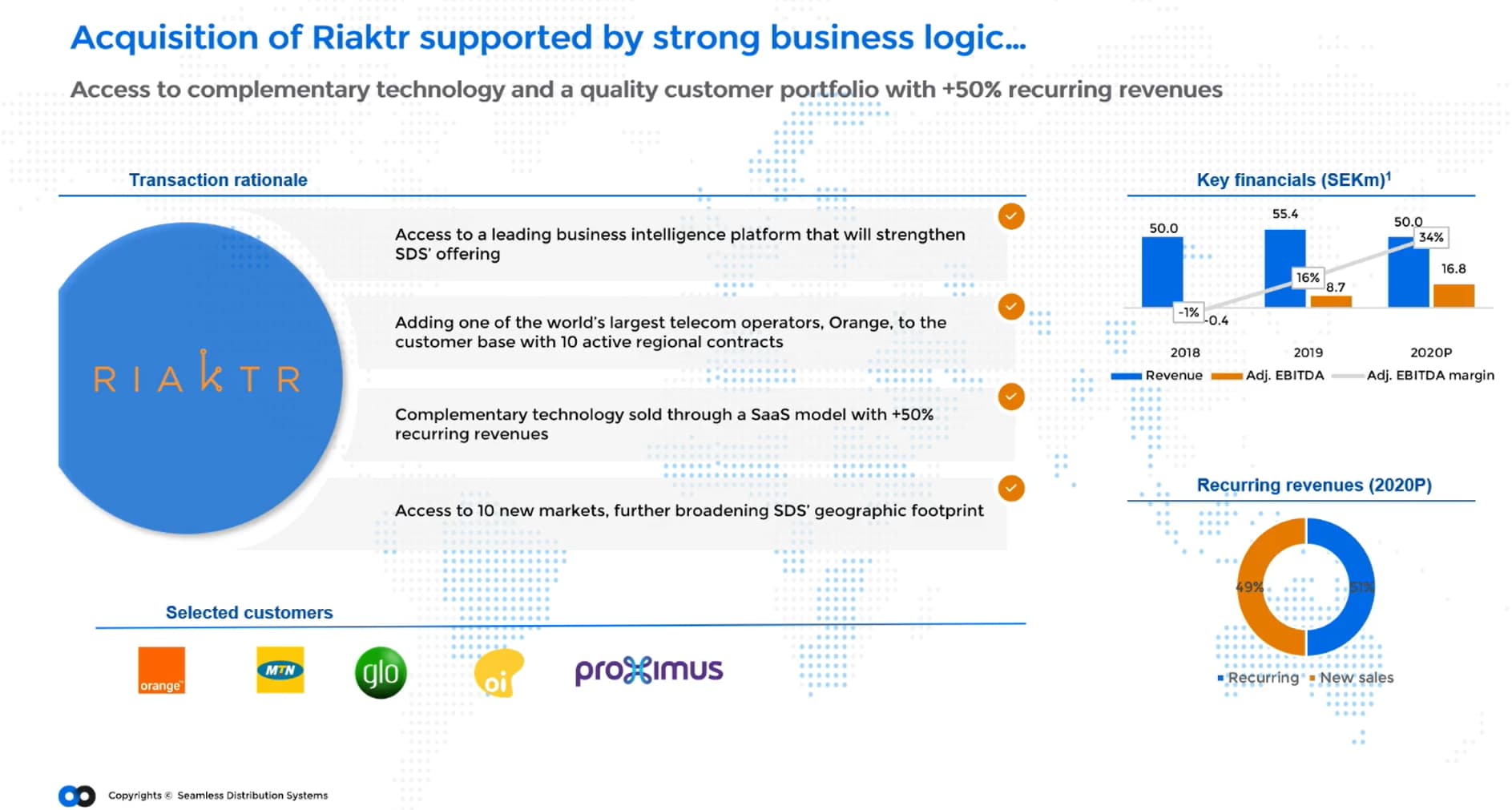

The acquisition of the analysis company Riaktr in the spring of 2021 has immediately proved successful, with a positive contribution to the result in 2021. In 2022, we will take further steps in the integration of the company into SDS. The product portfolio from Riaktr is now a natural and strategically important part of RVM, in addition to its ability to continue to address its own business opportunities. During the quarter, we intensified the work with cross-selling on the expanded customer base that came with the acquisition, and we are already starting to see results from this in new business discussions.

The company carried out a directed issue of SEK 20 million during the quarter to the major owners. It feels good that all the owners surveyed participated and show continued confidence in the company and the organic growth investments the issue aims to enable.

Sales development during the quarter

An important deal during the quarter was the additional order of SEK 2.7 million that the company received in Pakistan with one of the largest international operators in the region. This is an operator group that was added as a customer to SDS in 2021 and which with the order already shows us a strategically important continued confidence. The order concerned our component Smart Campaigns & Commissions, SCC, and the customer is thus expanding its installation in Pakistan with another component from our RVM portfolio. As the operator group has several local operators in the region - two of which have been SDS customers since 2021 - we see further opportunities for a successful implementation.

In March, the formal and locally acclaimed agreement was signed with Vodafon Oman on site in Muscat. Vodafon Oman is making a major investment with its establishment in Oman and places great faith in SDS 'entire RVM portfolio. SDS has a volume-based business model with Vodafon Oman and the result during the quarter exceeded our forecast. Two major and important orders that were expected to arrive during the quarter were delayed due to customer-internal processes.

Clear course

The market for our services remains stable and our price remains stable. With the issue supplement, we can implement the nearby growth initiatives we have identified for our organic growth. Strengthened by what we saw at MWC, we continue to see interesting opportunities for SDS in an expected market consolidation among suppliers. We consider ourselves well positioned to take a leading role in this consolidation as we have already made the necessary technology investments in Microservices, expanded and sharpened the product portfolio and demonstrated the ability for longterm profitability growth and to successfully integrate acquired companies.