I thought I’d open a thread for a true value company on the Helsinki Stock Exchange, Saga Furs, which didn’t have a thread or any discussion yet. After years of languishing, Saga Furs might have an opportunity for significant profit growth following the closure of its largest competitor. Saga Furs issued a positive profit warning today. Saga Furs Oyj: Positive profit warning, inside information: Saga Furs Group’s result for the ended financial year clearly better than the previous year | Kauppalehti

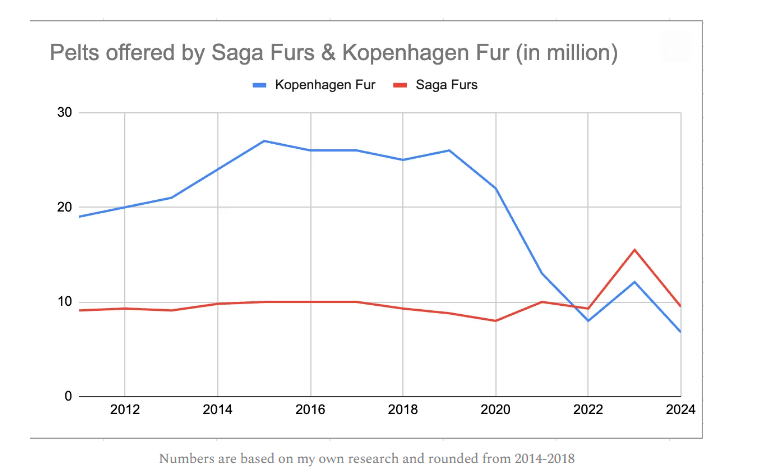

Saga Furs doesn’t necessarily operate in a glamorous industry, as the company organizes fur auctions. However, the company is in an interesting situation because the market leader in fur auctions, Kopenhagen Furs, is shutting down its business entirely, likely during this year, 2024. A few years ago, Kopenhagen Furs’ market share was around 60%. This could potentially provide Saga Furs with a significant amount of market share. The cost structure of auctions is quite fixed, and profitability could be pushed higher through additional sales (cf. 2021 revenue of €51M and EBIT of €11M). According to the just-issued positive profit warning, revenue in 2023 was €46M. Saga Furs has the opportunity to organically achieve a near-monopoly market position, as competitors have ceased operations and the industry isn’t the most attractive, so there will likely be very little new competition ![]()

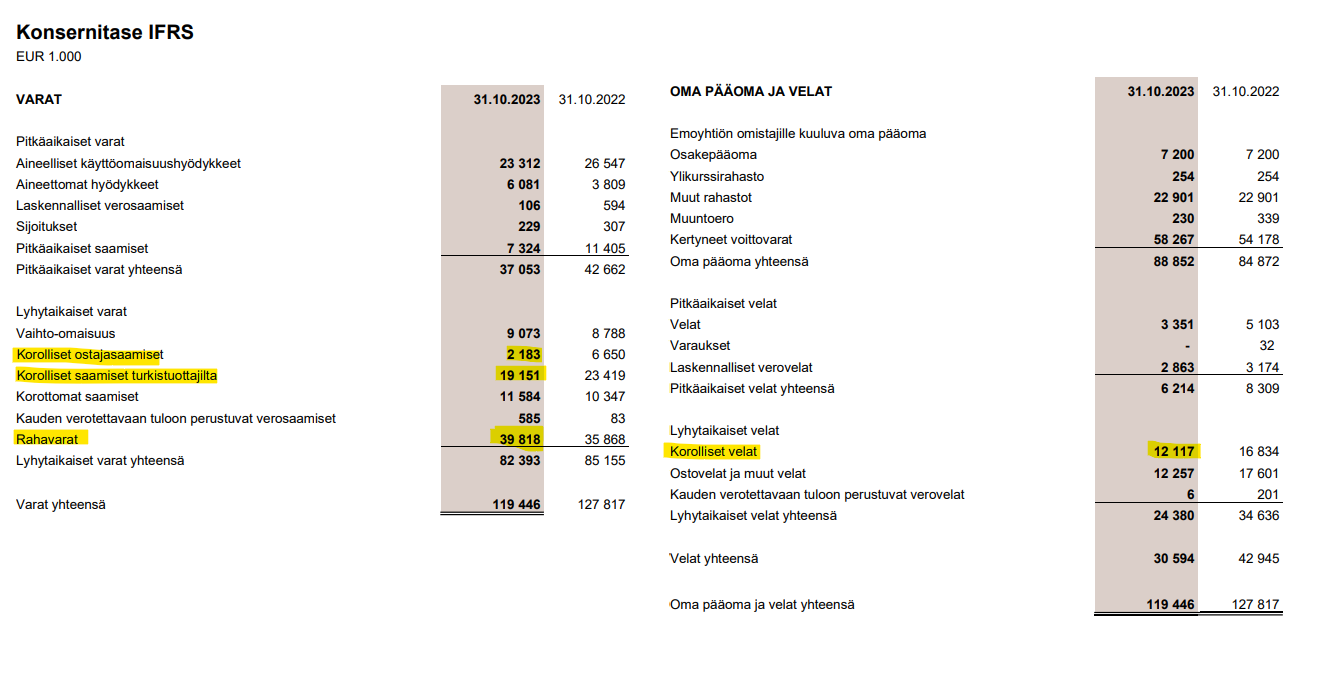

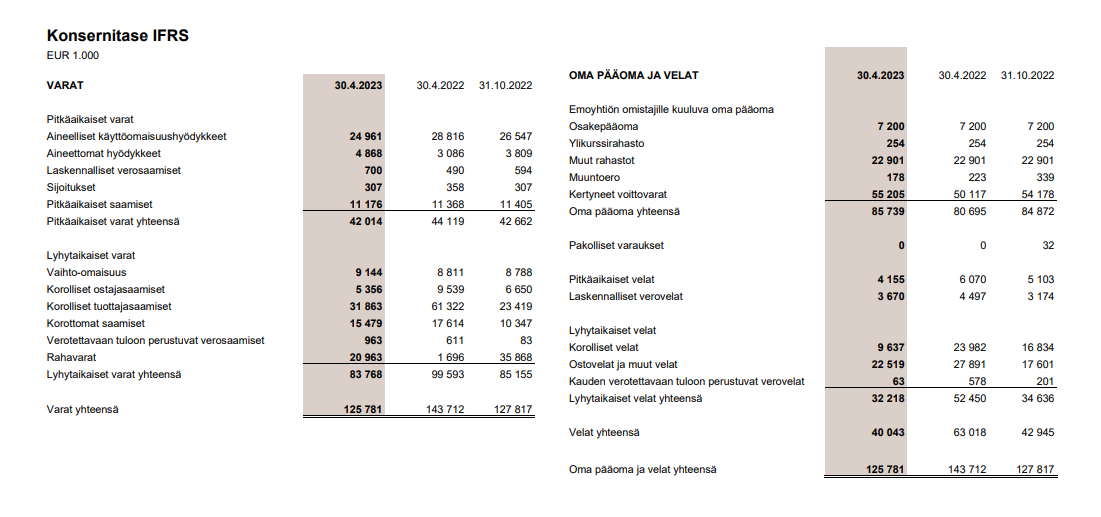

The company generates its income from auction commissions and by providing financing to buyers and sellers. In H1, the company had €37M in interest-bearing receivables from auctions. Cash stood at €21M and interest-bearing debt at €9.6M. In addition to gaining a significant potential market share, the company is very solvent, there is hidden value in the balance sheet, and the stock is priced at approximately P/B 0.4. If a larger amount of cash flow was released from interest-bearing receivables in H2 compared to last year, the company’s enterprise value (EV) could turn NEGATIVE. It sounds like a Chinese scam or a value investor’s dream stock.

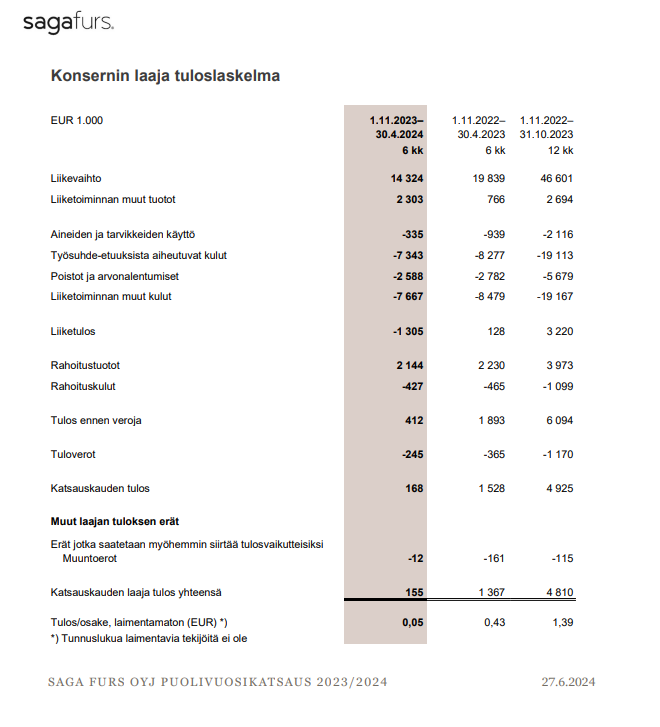

The company’s cash flow fluctuates significantly due to the interest-bearing receivables it offers to auction buyers, from which it earns substantial financial income annually. This has kept the company’s results for financial years profitable, even when the operating result has been negative. The company’s market cap is €38M at a share price of €10.5. If the company were to make an operating profit of €2.6M in 2023 and financial income of €2.5M, the result for the period after taxes would be €4.1M, meaning the P/E ratio would be 9.2x. There is potential for significant profit growth in the coming years when Kopenhagen Furs’ final auctions conclude.

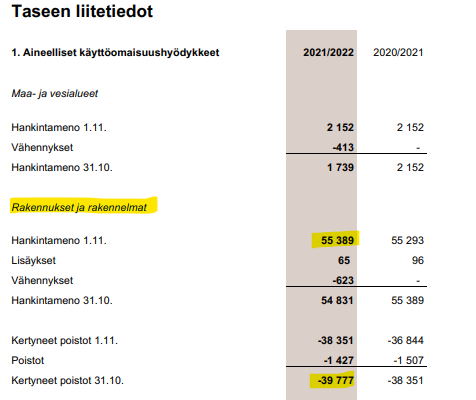

Speaking of hidden value, the company appears to have real estate on the balance sheet worth about €55M. I don’t know what these properties are or where they are located, but after annual depreciation, a significant amount of potential hidden value has been created on the balance sheet when proportioned to the company’s market cap (€38M).

I am no expert in fur farming, but as I understand it, even if fur farming were banned in Finland, it might not necessarily have a major impact on Saga Furs’ business, since according to the March 2023 auction, at least 18% of the pelts acquired were sourced from the Nordics. There are political risks in the industry, but I see Saga Furs as a low-risk investment due to its significant assets. If the real estate is liquid, the company’s liquidation value could be 3x the current share price.

Here is a story from October 2023 regarding Kopenhagen Furs:

The Changing Fur Auction Landscape (truthaboutfur.com)

Are there any experts on this subject on the forum?