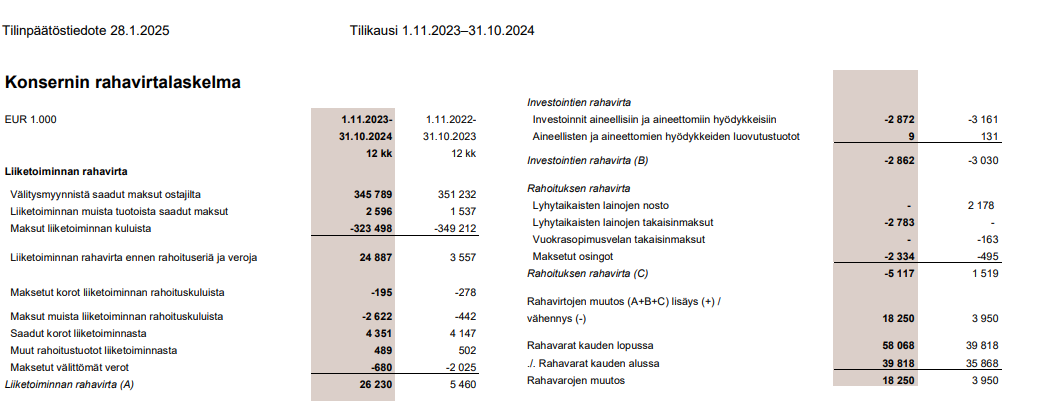

Free cash flow for the past period 23.37m€. ![]()

4 Likes

Isn’t it a bit less, though? Or am I looking at it the wrong way again?

Change in cash flows + dividend ~ 20.5M (?)

Free cash flow is, as I understand it, business cash flow minus investments. So 26.23M€ - 2.862M€ = 23.368M€.

I myself don’t usually take into account disposal gains from investments.

3 Likes

Ahh, that’s right, debt payment shouldn’t be reduced after all, I thought it was rent.. ![]()

1 Like

A very interesting company. What do those who know the industry better think about the future? We all know that the industry’s appeal, from breeders to end customers, is at least challenging at the moment. Is any change towards a more positive attitude towards fur farming expected anywhere in the world that could increase volume levels? As I understand it, the only area where furs are viewed in a relatively neutral light is in the Asian luxury markets, but how much can we expect that market to develop and grow in the coming years?

I was quite alarmed by those comments about declining volumes, even though the situation should be the opposite due to Denmark, meaning goods should be selling better than in recent years and profitability levels should rise quite high. What are the thoughts of those who know the industry more deeply, how much hope is there for a turnaround?

3 Likes

I was digging through Hesulin’s trash can, and one paper that came under closer scrutiny was this Saga Furs. I once, a long, long time ago, got burned by this (and lost euros) when an inexperienced investor fell into the traditional value trap. Now, however, the numbers are interesting enough that it deserves a bit more digging. As has been commendably mentioned in this thread as well, there would be substance for an investment case based on the numbers. Unfortunately, the initial enthusiasm quickly died when I glanced at the company’s ownership and board. Most probably already know, but on the board, everyone except one person is a fur farmer, and the ownership list is dominated by industry organizations. A strong déjà vu to listed food companies – are we serving the producers’ interests or the shareholders’ interests?

The whole case also strongly reminds me of another similarly valued case from Helsinki: Ilkka. The assets clearly exceed the market value, but the governance structure is exceptionally convoluted, and power is concentrated in parties whose primary agenda is not maximizing shareholder value. The old core business is also slowly fading (fur auctions vs. regional media), and there is no clear outlook for the future.

Does anyone on the forum have a view on what could unlock value in Saga’s case? Of course, you get about 7% from the dividend, which isn’t bad if it stays at the current level or grows, but I wouldn’t base an investment decision on that.

In the long run, it doesn’t really warm you up that you know you bought two euros for one euro, if the two euros are in a wallet behind glass, and you can either wait for the glass to break someday or immediately sell the two euros for that same one euro.

It would be interesting to get more information about those properties.

12 Likes

Quite a good analogy. I own both Ilkka and HKScan, and both indeed carry a significant owner risk. I’ve been following Saga Furs but haven’t taken a position, as the outlook on the currency of the company’s balance sheet value and the realization of its value is quite thin. However, Ilkka’s balance sheet includes Alma Media shares as a revenue-generating asset (which, unfortunately, are much fewer now since 60% of them were sold) and HKScan produces essential food in all situations, so there is demand for its products. Saga Furs constantly faces a big question mark regarding the long-term continuation of its operations.

In my opinion, comments from those ‘fox girls’ (animal rights activists) and demands for a prohibition law do not belong in this thread. Go to the politics thread if you absolutely must whine and declare your own pure orthodoxy on the Inderes forum.

5 Likes

In the March auction, prices still seem to be on the rise. I haven’t bothered to calculate for every category, but roughly between 5-15%.

The company’s news also includes verbal descriptions of price levels per category:

7 Likes

Mink farming is ending in Sweden.

7 Likes

Based on the first good hour of the June auction, mink prices are falling compared to March and are roughly at the same level as last year’s June auction.

| Color | Size | June 2025 | Difference 12mo | March 2025 | June 2024 |

|---|---|---|---|---|---|

| Brown | M50 | 43 | −2,3% | 49 | 44 |

| Brown | M40 | 39 | 0,0% | 43 | 39 |

| Brown | M30 | 37 | 5,7% | 38 | 35 |

| Brown | M20 | 31 | 6,9% | 32 | 29 |

| Brown | M0 | 25 | 13,6% | 28 | 22 |

5 Likes

Here is SalkunRakentaja’s article about Saga Furs, which has remained a very unfamiliar company to me for several reasons.

Saga Furs is the only Western intermediary for responsibly produced furs, and the company has successfully collected a good number of pelts from producers. Despite this, decreased production volumes have reduced supply. Compared to the situation two years ago, approximately 40 percent fewer pelts were brokered in the first half of the current fiscal year.

3 Likes

A couple of days ago, I wrote an English article/pitch about Saga Furs on Substack. If you’re interested in reading it, you can find it via this link: Saga Furs - messy deep value Finnish stock trading 0.33 P/TBV and net cash position twice the mcap.

If anyone here happens to read the article, feedback is always welcome, whether it concerns readability, incorrect facts, or assumptions.

17 Likes

Excellent summary of Saga Furs as an investment case. I have exactly the same thoughts. Perhaps the most interesting thing for an investor is the liquidation value of that Fur Center, which is indeed quite a big question mark. However, there is so much net cash that one doesn’t need to know the value of the buildings to invest in this with a net-net strategy. Understanding a more precise value might, however, provide grounds for increasing the position in the portfolio.

3 Likes

Poland bans fur farming. Transition period 8 years.

12 Likes

The results are out and they are looking really good. Saga Furs actually is a growth company ![]()

Financial year 1 Oct 2024 - 31 Oct 2025

-

A decrease in the volume of pelts brokered reduced the value of Saga Furs’ brokerage sales to EUR 324 million (financial year 2023/2024: EUR 343 million).

-

Group revenue increased by 3 percent and was EUR 42 million (EUR 41 million).

-

Operating expenses were at the level of the comparison period at EUR 43 million (EUR 43 million).

-

Operating profit weakened to EUR 1.4 million (EUR 1.7 million).

-

Net financial income increased to EUR 3.1 million (EUR 1.7 million).

-

Profit before taxes improved to EUR 4.5 million (EUR 3.5 million).

-

Earnings per share was EUR 1.00 (0.73).

The cherry on top is a massive €0.72 dividend coming up.

10 Likes

The first thing that caught my eye was this:

I stopped reading right there then.. ![]()

While waiting for a correction, at least the headline of the release has the correct dates.

5 Likes

Here is a piece by Jorma Erkkilä about Saga Furs.

Subheadings:

- Revenue and earnings turned profitable

- Share price more than doubled in six months

- The June auction will determine the way forward

3 Likes