The insiders will start buying with their own money once the valuation reaches the right level or is undervalued ![]()

3 Likes

The Danish foundation model generates value primarily through long-term stability, strategic consistency, and stakeholder focus, whereas direct share ownership emphasizes financial return, active owner guidance, and market-driven value creation. The foundation model minimizes short-term pressure but can be less dynamic than market-based ownership.

It guides the company through the foundation’s purpose (mission), rather than the owners’ return targets.

So, perhaps the goal of Revenio’s major owner is not the growth of the share value at all, but the mission to improve the treatment of eye diseases.

Jouni’s excuse about investing through a personnel fund for tax reasons is pure damage control. Funding bonuses through a personnel fund is an economic no-brainer, of course, but the fund’s board decides on the investments, and they are usually well-diversified. There is no requirement for the fund to hold the company’s own shares at all. It’s surprising there’s even that much in there ![]()

How is that relevant to anything?

@Tmpr2000 You don’t seem to be familiar with personnel funds. I had Gemini explain what kind of structure (himmeli) we are talking about.

Summary

Here is a ready-made, concise, and clear information package to be copied to the discussion forum. The text is based directly on Finnish tax legislation (Income Tax Act, Section 65) and illustrates the benefit with rock-solid math for high-income brackets.

Financial Benefits of a Personnel Fund – Should You Take a Bonus in Cash or into the Fund?

In many companies, employees can choose whether to receive performance bonuses and incentives as cash with their salary or direct them into the company’s personnel fund. The financial difference between these two choices is surprisingly large in favor of the fund.

The benefit of a personnel fund is based on three advantages baked into the law:

- No employee side costs: No employee pension or unemployment insurance contributions (totaling approx. 8.6%) are withheld from the amount transferred to the fund.

- Employer’s additional bonus: Since the employer saves their own side costs by transferring money to the fund instead of paying salary, many companies pay this saving to the employee as an additional bonus (in this example +20%).

- Withdrawal tax relief: When money is withdrawn from the fund, 20% of the withdrawal is completely tax-free and only 80% is taxed as earned income.

Calculation: Immediate Benefit (Gross Bonus €1,000)

The calculation below compares a situation where a €1,000 gross bonus is either taken as cash or directed to a fund and withdrawn immediately as soon as the fund’s rules allow.

The calculation uses a high 50% marginal tax rate (a common situation for middle and high-income specialists and managers) and a 20% employer additional bonus.

| Item | Bonus as Cash | Bonus via Fund |

|---|---|---|

| Gross Substance | €1,000.00 | €1,200.00 (incl. 20% additional bonus) |

| Employee side costs (8.6%) | - €86.00 | €0.00 (not applicable to fund transfers) |

| Tax-free portion (20%) | €0.00 | €240.00 |

| Taxable earned income (80%) | €914.00 | €960.00 |

| Income tax (50% marginal tax) | - €457.00 | - €480.00 |

| Net take-home | €457.00 | €720.00 |

Summary and Conclusion

- As cash with salary: Out of a thousand-euro bonus, you are left with €457.00.

- Recycled through the fund: Out of the same thousand-euro bonus, even if withdrawn immediately, you are left with €720.00.

The financial benefit to the employee is +€263.00, meaning you get approximately 57.5% more net cash in hand.

The higher your marginal tax rate, the more you benefit from the fund’s 20% tax-free portion. If you leave the assets in the fund to grow for years, the benefit multiplies thanks to the tax-free compound interest effect within the fund. Even in the short term, taking cash is purely leaving money on the table.

6 Likes

I highly doubt that is the case. If it were, the company’s management would be acting in violation of the Limited Liability Companies Act.

According to the Limited Liability Companies Act (OYL 1:5 §), the primary purpose of a company is to generate profit for its shareholders, unless otherwise stipulated in the articles of association.

3 Likes

True, that is what the law says. I am thinking about the foundation ownership model. In the same way, Stockmann’s main owners were Swedish-speaking foundations. In other words, ownership essentially vanished because it wasn’t clear who exactly was in charge and had the will—well, the foundation decides, but who specifically? Is there a similar pattern here with Revenio? A “will-less foundation” that just “blesses” the actions of the company management, whether those are just management’s obsessions or “grand” expansions involving expensive acquisitions. I truly hope that in the Danish foundation, there is a person who actually scrutinizes and decides what is sensible for Revenio to do. Additionally, since the problem is that the foundation is supposed to manage several companies… I wonder how significant steering Revenio actually is for them?

1 Like

There is clearly an effort for closer monitoring and influence from Demant’s side. Nicklas Hansen, Demant’s Investment Director, was recently elected to Revenio’s Board of Directors. The same guy is also apparently on the boards of other companies owned by Demant.

Ownership steering is rare and by no means involves interfering in daily management. Owners essentially make only one crucial decision - electing the Board of Directors. The Board’s most important task is the selection of the CEO.

Revenio is building the foundation for future growth. Demant is a stable owner that knows the industry. At the same time, however, it reduces the probability of someone else buying the entire company. Overall, the situation currently looks more positive than worrying.

8 Likes

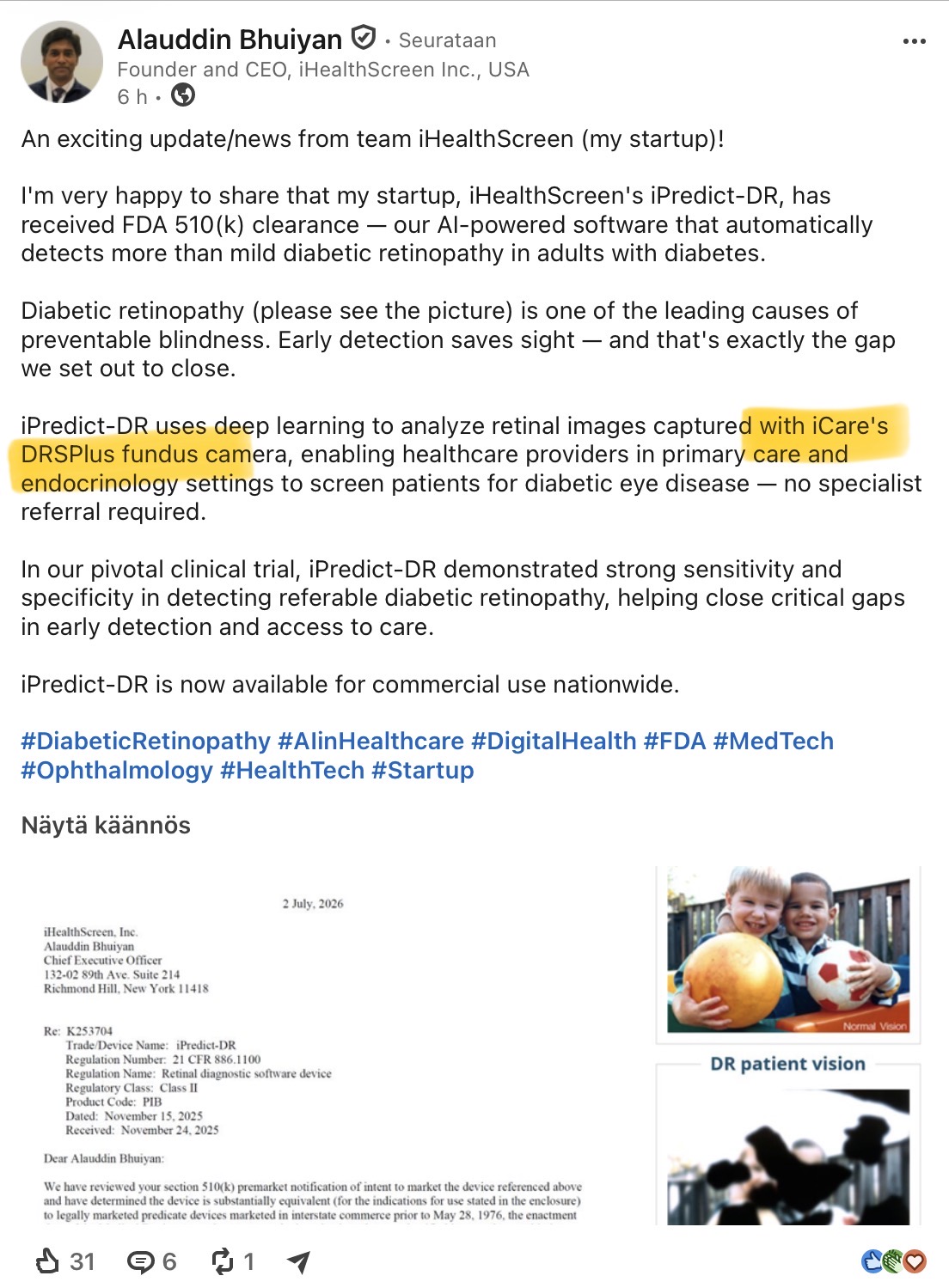

iHealthscreen has been granted FDA clearance for its class PIB for autonomous diagnosis of diabetic retinopathy. Judging by the trials, the clearance has been granted for the combination of iHealthscreen’s algorithm + DRSPlus. → edit: Confirmation on LinkedIn

The results of this trial were likely used for the application:

A newer trial is apparently still ongoing:

18 Likes