This background and the CEO explain to some extent the low purchase price and why Visionix has been willing to merge with Revenio in a way that the old company “ceases to exist.” It is difficult for me to believe that Revenio’s management didn’t know the whole story beforehand. Red flag.

2 Likes

Well, first there was concern about buying a French company. Now people are outraged when the acquisition target turns out to be of Israeli origin.

It is good to realize that a vast number of high-tech firms have originated in Israel. In fact, Israel is likely the world leader in this field when adjusted for population.

I have no problem with the company to be acquired having operations in Israel. Quite the contrary, given that their innovativeness is a statistically proven fact.

31 Likes

I agree with you, there is a lot of great expertise to be found “there.” As I wrote above, the article rather reinforced my thought to stay on board and see if this turns out well.

7 Likes

Maybe some subscriber could summarize what it is that Europeans are failing to grasp.

Certainly, a pro tip for the CEO:

Since you know this to be the case, and this is a quote, how about trying once more to help with that perception?

After all, quite a few of the owners and potential investors are European, and judging by the share price performance, there hasn’t exactly been a rush to the buy side.

Well, I know it’s just Alma’s subpar headline writing, of course… But still, it would be good for the company to shed some light on the matter.

Revenio made a giant deal, share price collapsed – CEO: ”Europeans do not grasp the big picture” Revenio teki jättikaupan, osake romahti – Toimitusjohtaja: ”Eurooppalaiset eivät hahmota kokonaisuutta” | Kauppalehti

3 Likes

The CEO’s view is likely based on this: According to the CEO, American investors have remained significantly more confident than Europeans.

“If we consider our shareholder base, the Americans have remained very confident.”

According to Toijala, this is also evident in investor meetings and interest toward the company.

“If you look at meeting requests, investors in the United States—including new ones—have been very active.”

In Europe, however, the mood is more cautious. According to Toijala, the market lacks a certain general positive momentum.

“Perhaps one would hope for more of that kind of positivity and courage in these European markets.”

And then a summarizing comment from Toijala: “In principle, we didn’t just buy a company now, but long-term strategic growth.”

I don’t dare to quote any more.

15 Likes

I promised to write a bit about yesterday’s meeting with Revenio’s CEO Jouni Toijala, so here are some of my scattered thoughts. We had about 2.5 hours and there were around 40 fellow investors, so questions ranged from the new acquisition and distribution network to specific questions about the devices.

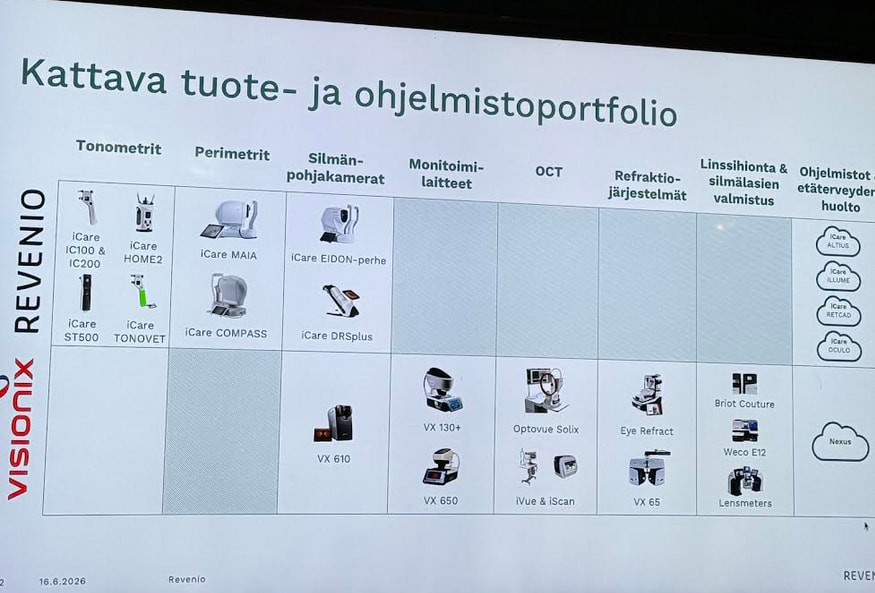

The evening followed a similar pattern to the Annual General Meeting 1.5 months ago, and the slides were largely the same; I didn’t really expect anything new to emerge in this timeframe. Perhaps it became clearer to me now regarding Visionix’s OCT Optovue Solix that the device is very competitive (in Jouni’s opinion) compared to other devices of the same level on the market. Optovue Solix definitely does not compete with high-end devices sold to universities or research institutes, but is more middle-range. The OCT R&D center is located in the US, and manufacturing—if my notes are to be trusted—takes place in China. Revenio expects organic growth from Visionix’s strong devices such as the Optovue Solix (OCT) and the multi-diagnostic devices VX 130+ and VX 650. Jouni noted that it would be amazing if they could one day combine true confocal + OCT into the same package; in his opinion, that would be a superior combination. We’ll wait and see if product development moves in this direction. One last point on the OCT: Revenio would have had the opportunity to develop its own device, but they saw that the surest way to enter the market was through acquisition.

There was again discussion about Visionix’s profitability, but I didn’t quite grasp what the actual steps are for the 20 million EBITDA improvement by 2029. Apparently, there is a meeting today, Wednesday, to discuss sales synergies and set clear goals for the future. If I understood correctly, that 20 million EBITDA improvement does not include potential production efficiencies, which would come on top of that 20 million. @Sergio, who was present, can correct me if I misunderstood. Jouni noted that when Centervue was acquired, its profitability wasn’t quite at Icare’s level, but Centervue’s profitability has been improved over the years, though not quite to Icare’s level.

I thought there was a good question from the audience regarding which products will drive Revenio’s growth in the future, but the answer was quite political. Jouni went through all possible products and their market shares; I would have preferred some more concreteness here, but unfortunately, it wasn’t provided. At least it was news to me that Revenio’s microperimeter Maia has a 70% market share and the price of a single device can rise to 50,000 euros depending on which software licenses are included.

He was also asked what was learned from the Centervue acquisition and what was done differently now with Visionix. Jouni replied that at the time of the Centervue acquisition, Centervue’s R&D department was kept separate for a long time, but now with the Visionix deal, the product development units will be integrated into one quickly.

There was also talk about the Revenio brand, and it became clear quite quickly that Revenio as a brand is not well known, especially to Americans, but is rather known as Icare. Apparently, the Visionix brand is very well known globally, and they are now considering which angle to take in the future. It sounded a bit like a name change might be coming and brands would be clarified, which doesn’t sound like a bad idea to me in principle.

I can’t manage to write everything here during my workday as there really were a lot of questions. Finally, regarding the article where Visionix founder Marc Abitbol was interviewed: Jouni hadn’t read the interview and looked very surprised when I told him about the content of the article. Jouni stated that he had certainly not had a conversation with Marc where it was mentioned that Visionix should be referred to as an Israeli company. Jouni asked to read the article, and I emailed it to him yesterday evening. Jouni noted that Marc is very patriotic and proud of his Israeli background, and they have had good trips together in Jerusalem.

83 Likes

I didn’t quite understand how the EBITDA improvement will be achieved either.

In addition, some information regarding the share issues: the directed share issue has already been carried out at a high subscription price. The public offering is expected around the beginning of October. It remains to be seen what the subscription price will be.

11 Likes

Thank you @Pandakarhu for the comprehensive answer and for sharing the information ![]()

Apologies for my skepticism and for harping on these points, but we are dealing with major issues regarding the Revenio investment case.

I have nothing against inorganic expansion. Visionix’s offering crosses nicely with Revenio’s, and on paper, the merger looks quite logical.

One of the positive aspects of the acquisition is that Revenio gets cheap debt, and shares are issued to Visionix at a “high” price relative to the current exchange rate. As they say, you don’t get quality for cheap. Expanding into the OCT market organically would have been a long and uncertain process; purchasing Visionix and paying some level of premium is quite justified.

However, when moving from consultants’ Excel synergies to the real world and previous experiences with M&A, the situation doesn’t look particularly rosy.

Mergers and acquisitions have been studied with varying results, but for example, Harvard Business School and Fortune refer to data suggesting that over 70% of acquisitions fail!

The management team has no “skin in the game” at all!

For example, the CEO has worked at the company for years and drawn a high salary. Yet, he owns shares worth less than a month’s pay?!

From the Kauppalehti article, the CEO states: “the critical question is not financing or valuation, but what the deal changes.”

It is somewhat cringeworthy to shout that valuation doesn’t matter when you don’t have your own money at stake. And then it’s said that investors just don’t understand.

I agree to some extent that the stock market is sensitive to uncertainty, share issues, etc., and the stock might even be beaten down too much.

Revenio’s total addressable market is growing, yes. By buying Visionix, they expanded the offering into faster-growing areas, yes. Visionix’s and Revenio’s portfolios overlap beautifully, yes. The companies surely have some cost synergies, yes. The companies surely have some cross-selling potential, yes.

But I, for one, am not convinced that things will go like they do in the movies.

- As mentioned in Pandakarhu’s message, the product portfolio brands are all over the place, and apparently even the company insiders don’t know what will be done with them.

- Revenio hasn’t really had its own production, while Visionix has it in Israel and China? It’s quite difficult to start streamlining and extracting synergies from that.

- Cross-selling and a “one-stop shop” sound beautiful on paper, but time will tell if Revenio’s sales + Visionix’s sales are much more than the sum of their parts.

- Revenio paints a picture of growing three times faster than the market. In segments where they are strong, the market share is already high. In segments where they are not strong (e.g., Visionix’s OCT with 5% of the market?), will competitors just watch from the sidelines as Revenio conquers the market with high margins?

30 Likes

The brands are indeed all over the place, but on a positive note, there is very little overlap in the products; now they just really need to figure out how to brand this entity.

In my opinion, however, the acquisition is quite fresh and it’s quite normal that management is currently searching for a direction on how to steer this “ocean liner” forward. I spoke with many people from Revenio at the Annual General Meeting, and it emerged that Revenio hasn’t received data directly from Visionix; instead, they always had to go through Due Diligence (DD) because Visionix and Revenio had a non-compete agreement before the deal closed. I’m no professional, but I’d wager that when DD is in the middle, communication is certainly not the smoothest or fastest. Now that the deal is officially wrapped up, the wheels will likely turn a bit faster.

I do agree with you about the cross-selling; it can be made to look very good on paper, but how will this be efficiently integrated globally? Jouni said that in the US, for example, Visionix and Revenio have a very similar sales model, meaning there is both direct sales and distributors. Direct sales is presumably Visionix’s strength, and now Revenio gets access to it as well; the question now is how effectively this can be integrated.

I’m not trying to defend this acquisition—I’m a bit skeptical myself. I’ve mainly asked management the same questions you are raising here and I’m pasting answers from my own notes ![]()

29 Likes

I’m looking at this as a very long-term Revenio investor, and I’m honestly anxious to see how they pull this package together. Just one observation regarding how Toijala commented on the different product families: it gives the impression that they don’t know what they are doing with each one. It’s important to remember that Toijala cannot make comments in casual investor communications that might affect the motivation of certain key players. Plans are surely already in place and will be communicated internally first to avoid rocking the boat.

2 Likes

To me, it is crystal clear what the profitability improvement calculations are based on.

Whether it will be easy and whether it will materialize to the extent planned is a different matter.

In a nutshell: phase out in-house sales staff as much as possible and provide distributors with broader product portfolios, giving Revenio more leverage in margin negotiations, the ability to select the best distributors, etc.

Additionally, there are, of course, other potential overlaps in IT, etc., but those are self-evident.

I don’t recall how much this has been discussed in the thread, but I personally assume the focus will shift more toward the distributor channel rather than direct sales. Naturally, there will be a hybrid model overall. For example, in the US, both likely have their own direct sales, which is where the “easiest” synergy potential probably lies.

I must specifically mention the “One-stop-shop” concept, which is emphasized in several of the company’s communications. As a layman, it is impossible to assess its significance, but let’s hope and trust that the company is correct regarding its weight. In practice, this will be measured by how well distributors are able to sell a wide range of different (new) products and how customer buying behavior functions.

9 Likes

In summary: get rid of in-house sales teams as much as possible and give distributors broader product portfolios, giving Revenio more leverage in margin discussions, allowing them to select the best distributors, etc.

I personally see it exactly the opposite way. That is, Visionix’s—now their own—salespeople will start selling Revenio products, and the margin previously taken by distributors will remain in-house. This will happen in the 6 countries where Visionix has its own sales operations. Additionally, there is of course the integration of organization, procurement, and processes shown in the slides, and later the creation of a common sales platform, etc. This means an entire eyewear/optician/doctor’s station can be equipped with Revenio products. Within a year, we should see if the benefits are gaining momentum; the longer term is then a separate matter.

4 Likes