It certainly seems like an acquisition option is playing a role in the background, which explains that specific wording.

In my eyes, Revenio is actually looking like quite an interesting company for the first time in a long while.

It certainly seems like an acquisition option is playing a role in the background, which explains that specific wording.

In my eyes, Revenio is actually looking like quite an interesting company for the first time in a long while.

Demant, BlackRock and the other big boys in the top 20 have, on the contrary, increased their holdings. Those who have lost faith are retail investors outside the top 100.

Revenio’s Q4 results were weighed down by currency headwinds, delayed price increases in the US due to customs, and one-off costs. However, cash flow from operations was historically strong thanks to efficient working capital management. Revenio CEO Jouni Toijala comments on the company’s performance in an interview with analyst Juha Kinnunen.

It’s very clear that an acquisition is coming, looking at Jouni’s answers to the questions ![]()

-That was a good interview, thanks to Juha![]() it became quite clear there that the product portfolio should be expanded on the device side. Targets have, of course, been scouted for a long time already, as long as the valuation is right. -One wouldn’t necessarily need to travel very far to go shopping. After all, Optomed is available right here, with a camera that already has FDA clearance

it became quite clear there that the product portfolio should be expanded on the device side. Targets have, of course, been scouted for a long time already, as long as the valuation is right. -One wouldn’t necessarily need to travel very far to go shopping. After all, Optomed is available right here, with a camera that already has FDA clearance![]()

I’m really excited to see what kind of acquisition is coming. It would be good if the same salespeople could have a larger portfolio to sell. Also, I think they have a good track record with integrations. But the current business is definitely very difficult.

Thanks for the great interview. It’s been stated directly before that inorganic growth is being actively pursued. But now, the wording of the dividend proposal was such that an acquisition is likely all but signed.

The AGM is held on April 16th, and if the acquisition is finalized before then, the board can decide to skip the dividend distribution.

In the Q&A section of the webcast, when Jouni was asked about acquisitions, he said that valuations have started to reach reasonable levels. He also mentioned that Robin has been working hard on these over the past quarters/years. Could it also be that Robin got an acquisition over the finish line and now is a good time to change companies?

And at Optomed’s current share price, the price wouldn’t be dizzying either…

I watched the interview and it seemed quite reasonable otherwise, despite the external factors. Is some kind of acquisition likely this year? But I didn’t grasp why the price increases in the US didn’t coincide with the tariffs. Was the old price locked into a signed contract or something?

I don’t share the same view of the interim report as the market reaction. If I didn’t already own enough, I would have bought more today after such a beating.

BUY and a couple of euros off the target price. Valuation has been pushed down so much that Juha considers it an overreaction. I have a strong hunch that the model portfolio will add to its position in a couple of days, unless the price runs away before that.

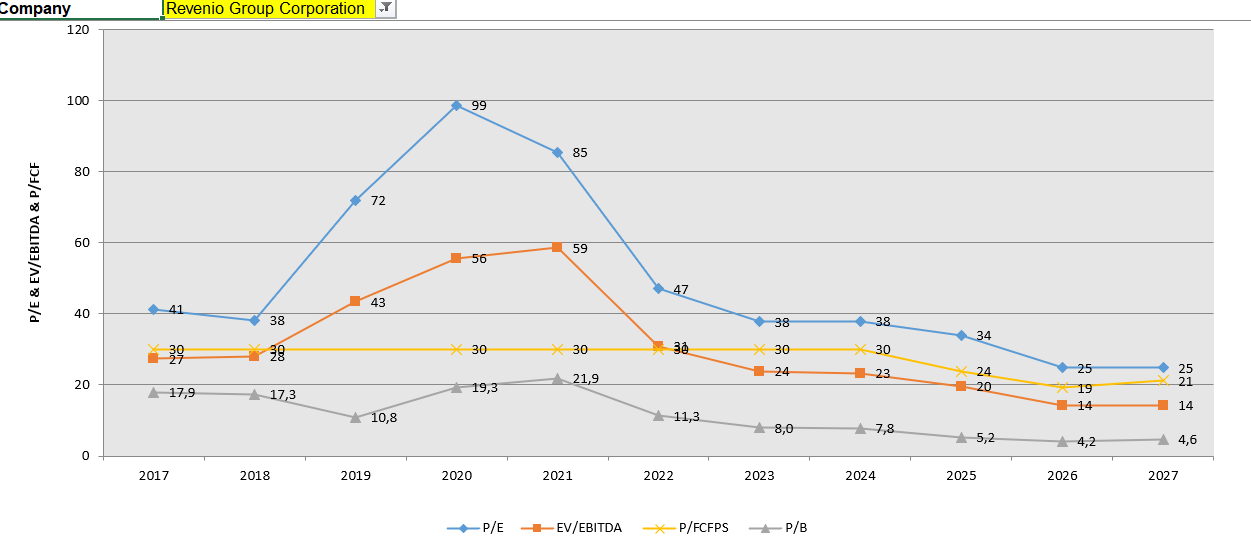

We reiterate our Buy recommendation for Revenio and adjust our target price to EUR 24.0 (prev. EUR 26.0). The Q4 result was a clear disappointment, especially regarding profitability, and we estimate that cost pressures will continue in 2026 as FDA trials accelerate. However, the guidance for 2026 supported our growth expectations, and despite the uncertainty, we consider the company’s outlook to be strong. The stock’s valuation is still at the bottom levels of the iCare era, and we see a potential acquisition bringing additional interest to the share.

The valuation has hardly changed, as the decline in the share price and forecasts practically cancelled each other out. Revenio’s EV/EBIT is only 15x based on this year’s forecast, whereas during the iCare era, the corresponding multiple has mainly fluctuated between 20–30x. Although the company’s earnings growth has slowed down and there is more uncertainty than usual in the market, we believe this is a clear overreaction. Even though the Q4 result was a clear disappointment, market-related uncertainty decreased significantly thanks to strong Q4 sales and guidance. Consequently, we consider it even more unlikely that Revenio would suffer significantly from the market situation in the same way as Zeiss. We see no material changes in the long-term drivers and consider Revenio’s position in the industry to be very good, which is why we view the current uncertainty as a buying opportunity. Acquisitions always involve significant risks, but we also view the strengthening of this option as a positive for Revenio.

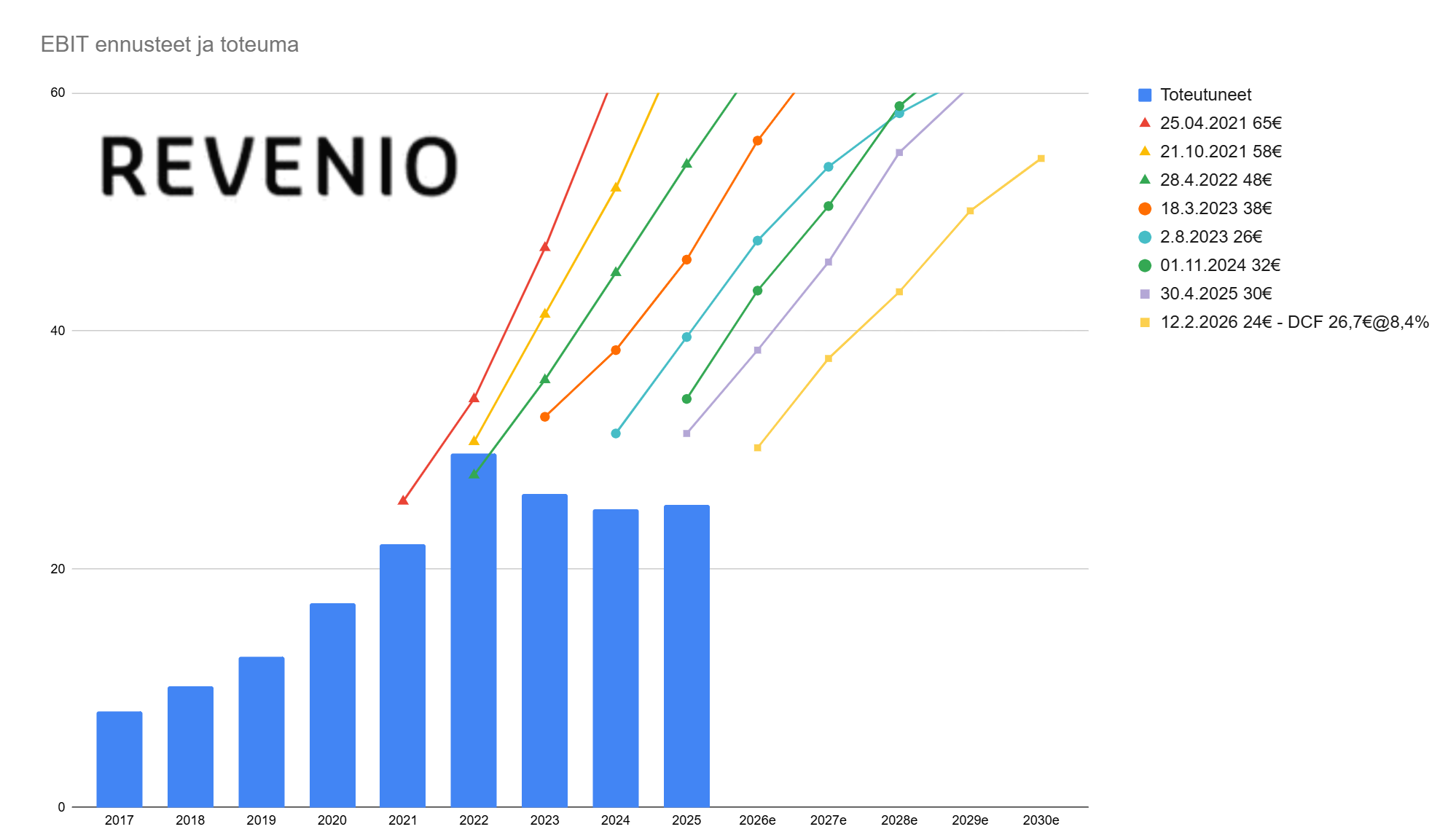

Earnings double in 4 years ![]()

Continuing with conservative forecasts. Explosive earnings growth is coming in the next few years.

Why have you chosen that specific analysis from April 25, 2021, as the starting point for your review? After all, Inderes has been covering Revenio for ages, and the forecasts have hit the mark quite well. I took a spot-check look at Mikael’s report from February 16, 2018, for example; in it, the EBIT trajectory is quite solid even up to this day ![]()

Is that the problem you see in the chart? ![]()

You can look at the matter in so many ways. Even the fact that Mikael made good forecasts in 2017 is true. I just don’t bother to write it in every post.

I didn’t say there was a problem, I was mainly wondering why the forecast history doesn’t go further back, since those forecasts are available; it would give a fairer picture of Inderes’ long-term forecast accuracy. Otherwise, it creates a recency bias ![]()

Mikael stopped making Revenio forecasts in 2021. I don’t believe that forecasts made by Mikael more than five years ago help with future forecasts. And yes, there is other informational value in that image besides whether those forecasts hit the mark. It is clear that they didn’t.

In my opinion, Revenio offers the best buying opportunity since spring 2019, when the CenterVue acquisition was made. The valuation has been pushed down, but at the same time, the market position and relative performance vs. competitors are first-class. I believe Revenio is executing its strategy very purposefully, supported by a committed and long-term principal owner. The acquisition card (even in the very short term) makes owning it interesting at this point, if/when the product portfolio and consequently the target market can be expanded. And surely the company has products/services in development in its own pipeline that we aren’t even aware of yet. Now you get growing quality at a reasonable price, and you can no longer claim that “Revenio is always expensive.”

So, is your point with that image a) forecasting is difficult, especially predicting the future, or b) do you think the current analyst is performing so poorly that the analyst should be replaced?

If it’s a), I strongly agree with that; especially in recent years (3-5y), forecasting economic development has been devilishly difficult.

Everyone can interpret those images however they like. In my opinion, one can draw very clear conclusions about future forecasts from them, but I’m not claiming that anyone needs to reach the same conclusions, even though I think it’s sensible to utilize that information.

The company’s valuation is lower than ever, at least. The cash position is strong and cash flow for the full year is good. Q4 was admittedly quite poor. Hopefully, these are temporary problems.