Pitchi #5: Alzchem

Alzchem - health benefits from creatine and the disruption of the world order

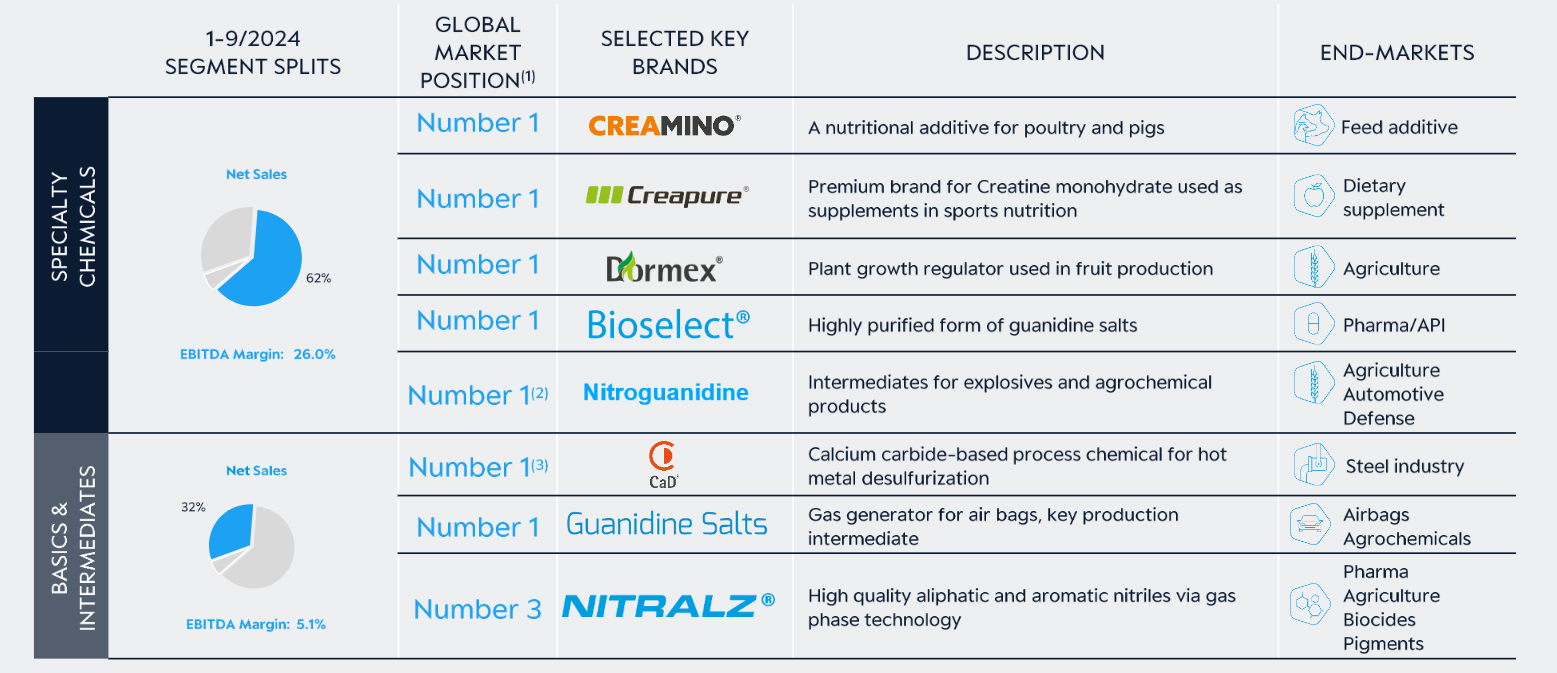

Alzchem is a German chemical industry company whose business is divided into three segments: Basics, Others, and Specialty Chemicals. The Specialty Chemicals segment manufactures various compounds used in many different industrial sectors - from consumer products to the defense sector. These two are the theme of this pitch. In short - Alzchem is one of the few cases where one can still get in cheaply on Europe’s rearmament of the defense sector and benefit from the increasing use of creatine.

Company History

For years, Alzchem invested in the specialty chemicals segment, and the market gave no value to this, even though the segment grew steadily year after year. However, as the German chemical industry took a hit due to rising energy prices, Alzchem was able to raise prices in the specialty segment without volumes suffering, and the market began to understand the value of the company’s business. The price increase that occurred in 22/23 appears to be sustainable, as prices have remained stable during -24, but volumes have grown.

A significant reason for this has likely been the structure of the creatine market. Various studies suggest the market size is around a billion - however, it is more difficult to discern whether this refers to the supplement products themselves or the compound itself. Nevertheless, some clarity can be gained by listening to management’s comments from the Q3 call.

Analyst:

“Could you share numbers regarding Creamino (creatine for production animals)?”

CEO:

“We don’t want to give too much information because we only have one competitor, a German one, and the next one is a Chinese company.”

So, the market appears to have a few Western companies and an undefined number of Chinese companies. This suggests an oligopoly. Market stability benefits everyone. However, recent events may have positive effects on Alzchem’s market share.

With most creatine coming from China, this also has a very interesting consequence. The price of Chinese creatine is now more expensive for the US due to Chinese import tariffs, and this may have a positive impact on Alzchem.

Defense Theme

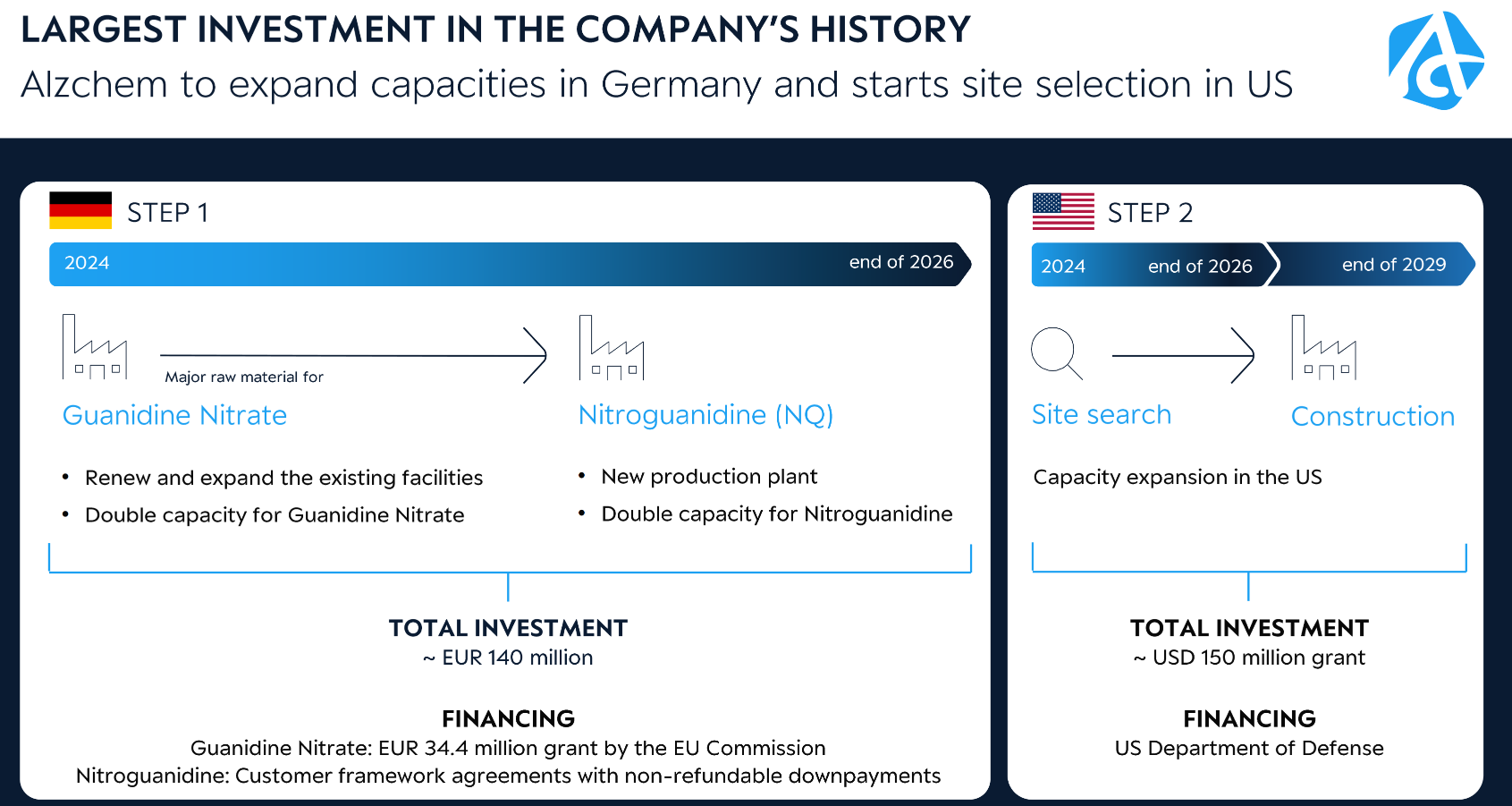

Alzchem is the only manufacturer of Nitroguanidine in the West, meeting the needs of the EU and US armies. Nitroguanidine is primarily used as a propellant in large-caliber artillery.

Over the past couple of years, Western countries have realized that they do not have enough ammunition stockpiles. The growing need for nitroguanidine is a direct consequence of this. As a result, both the EU and the US government are paying Alzchem to increase its nitroguanidine production capacity. How often do your customers pay you for your growth?

These are two truly large investments. Approximately 140 million for Europe and another similar amount for the United States. The European facility will be inaugurated for production in the autumn of -26, while the schedule for the US facility is still more uncertain. Likely by the end of the decade.

Catalyst

The reason why investing in Alzchem right now is interesting is that it has become clear over the past week that the Trump administration cannot be relied upon for European defense. This leads to a mandatory increase in defense spending, and as a result, the uncertainty about the utilization rate of the Nitroguanidine plant decreases.

Valuation

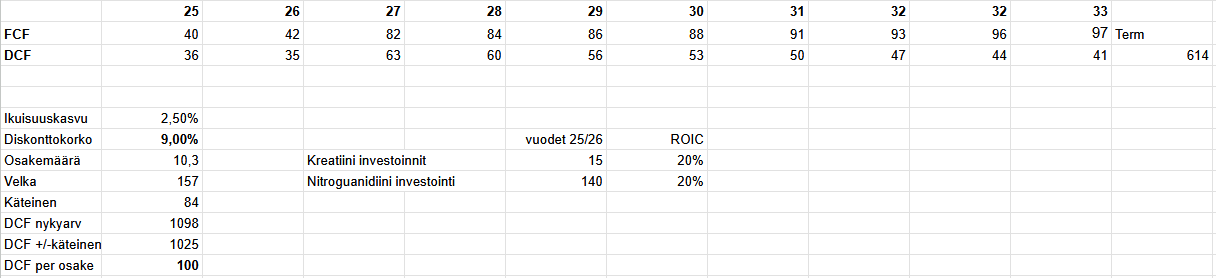

Therefore, in the cash flow statement, I assume that Alzchem will invest a communicated total of 15 million in new creatine capacity and the aforementioned 150 million in guanidine over the next two years. I assume that the investments will yield a 20% ROIC, and the non-guanidine business will grow by 4% until the terminal period.

As a result, with a discount rate suitable for a small company at 9%, I get a current share value of 100 €, which suggests an upside of approximately 50%. It is noteworthy in this valuation that I do not assign value to the US guanidine plant or potential M&A activities that management has started discussing.

From a valuation perspective, a -26 P/FCF of 16 is elevated for a small company, but a -27 P/FCF of 8 is attractive for a company operating in an oligopolistic market (creatine) and having a natural monopoly in another (nitroguanidine).