Thank you for your words. Personally, I am very confident that next year all this work from over the years will be rewarded. Contracts and deals are almost always under NDA and are disclosed at some point, either when royalties start flowing or when the RTLS business begins to scale. My main excitement/suspense is mostly about when this will happen and on what scale.

But if one has the patience to wade through these news/links of mine, I think you can fairly well estimate when the roadmaps have come into effect. If you research these things, you’ll know that from the moment decisions are made, it takes several years before products are ready and scalable in production.

And as for Revenio, I personally see potential here for something much greater than Revenio

More case studies. Getting that ADAS radar/IP into a Tier 1/OEM would certainly be a great boost for sales. The final breakthrough is starting to look close

Let’s also highlight the potential of the IoT market. It is going to be massive..

Here are Olli’s pre-match thoughts as Panostaja reports its Q1 results on Thursday.

In the report, our attention is particularly focused on the progress of CoreHW’s product business commercialization, as Japanese customers should have made decisions regarding potential pilot expansions by this point in the spring. Overall, we expect the company’s actual figures to be close to the comparison period, though our forecasting has been slightly complicated by the lack of comparison figures since the company changed its fiscal year timing. The Q1’26 report being published now covers the January–March period, whereas Q1’25 corresponded to the November–January period.

I believe we are now very close to closing deals with these pilot customers. I think there has been a wait for Bluetooth 6.2 “mandatory” status/testing availability and the release of Bluetooth 6.3.

Customers won’t buy until the BQB tests are passed; CoreHW already has Telec-certified products in Japan.

A customer justifies choosing CoreHW: “It meets both the Japanese radio requirements and the latest Bluetooth standard.”

TCRL makes Channel Sounding qualification mandatory if the feature is used.

A pretty good quick comment from Robo, matching what I managed to glance at myself! Forecasting was indeed a bit tricky since the comparison period figures weren’t available in advance! Robokommentti Panostajan Q1-tuloksesta - Inderes

If you have any good questions in mind for the Panostaja CEO interview, feel free to share them.

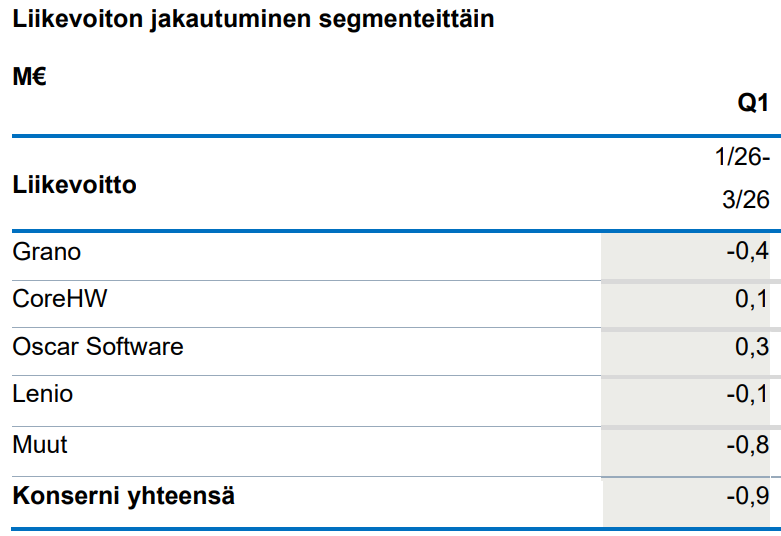

Why does such a small listed company have such high corporate expenses (-0.8 MEUR in Q1)? How is this justified, and what success has this brought to the shareholders?

I believe everyone wants to know about the situation with CoreHW. You would think that with €0.6m in group expenses, we would get a slightly more extensive report.

I recall that Gugguu’s minority stake was valued at approximately 1.5 million euros on Panostaja’s balance sheet. Has the risk of a write-down increased (cf. Hygga’s case)? Revenue continued to decline, and the loss relative to revenue increased further.

Have Panostaja’s growth targets for Lenio been adjusted (vs. autumn 2025), given that according to Q1, demand for Lenio remains weak and growth has not progressed according to plan?

This equation simply doesn’t work when the Tampere headquarters burns more than the portfolio companies manage to generate in operating profit for the group:

Another appalling result yet again, and nothing better is expected in the short term as the report describes the outlook for all investment targets as merely “satisfactory.” We have been waiting for CoreHW’s breakthrough for the last 5 years, and at this rate, we’ll probably be waiting for the next 5 years. The solution is similar to Optomed’s, but the promised final breakthrough has not materialized.

As for the management, the recent years have been a continuous cash burn. The most profitable parts of Grano (Sokopro, Diesel, etc.) have been carved out and sold off, leaving behind a constantly shrinking and unprofitable printing business.

This is certainly strange from a shareholder’s perspective. Profitable parts of Grano are being carved out and sold to the operational team at a bargain price. Meanwhile, after five years of waiting, they acquire a startup for a few million in an extremely competitive market.

I believe the first three factors justify and even exceed the current share price. Does headquarters have faith in Panostaja’s own valuation? What should the level be?

I reasoned the decrease in Grano’s net debt in the report as follows: “Grano’s net debt unexpectedly decreased by EUR 2 million from the end of the year despite the loss-making result. No clear reason for this was provided in the review, but we estimate it was driven by changes in IFRS 16 liabilities as office space was reduced to correspond with the decreased headcount.”

In Oscar, on the other hand, net debt rose by approximately EUR 1.5 million; this was due to dividend payments to Panostaja and a new lease agreement, which increased the IFRS 16 debt.

Regarding CoreHW, it could be a matter of the timing of customer pilot payments.

Gugguu has been optimized to the limit, and now its expensive children’s clothing is being produced in countries like China. So much for being “domestically made.”

Gugguu’s downward spiral doesn’t really seem to be improving. I wonder if this will be Panostajan’s next final write-off case this year: 1 MEUR in share capital and a 0.5 MEUR loan granted.

Olli has provided his comments on the merger of Lenio and Infomaatti

Panostaja announced on Tuesday that its portfolio company Lenio is merging with Infomaatti, which focuses on field work reporting. In our view, the arrangement is strategically very logical, as it effectively doubles the scale of the small Lenio and expands the software offering in the competitive mobile work market. Panostaja is investing EUR 2.0 million in the arrangement, which is approximately half of the parent company’s current net cash. In light of Infomaatti’s growth and profitability, the purchase price seems reasonable to us. In the context of Panostaja’s overall sum-of-the-parts, the transaction is small and does not affect our view of the company. We will update our Lenio forecasts in connection with the next update.