Olli has made a new company report on Panostaja in honor of Independence Day.

We reiterate Panostaja’s target price of 0.46 euros, but lower our recommendation to ‘add’ (previously ‘buy’) as the share price has already recovered slightly from its lows. In our opinion, the stock is still undervalued, but Panostaja will still require time.

Quoted from the report:

Overall, we consider Panostaja’s valuation level to be very low, but the unwinding of the undervaluation requires a return to a positive earnings trend and growth, especially from smaller value creators (CoreHW and Oscar). Grano, on the other hand, is supported by continuous significant cost-saving measures. In our view, these will help Panostaja overcome the current slump, and in the longer term, the recovery of the Finnish economy will support earnings development.

Tomorrow, we might get more clarity on the progress of Corehw pilots and whether they are being scaled up for production. It’s a shame that there are likely non-disclosure agreements in place, and we won’t get to know any customer names. However, it’s safe to assume that the customers are very large players in their respective fields. This can already be inferred from the scale of the pilots.

The scaling of these pilots can normally range from 10x-200x, depending on the industry of the company and the number of targets. There is indeed enormous potential here, which is practically offered with “free” pricing at this stage. Everyone can consider what the valuation could be if, for example, a 400k pilot is scaled 100x, and it’s an own product with high margins, own IP, own design, and manufacturing is done via tsmc. I argue that the margin% will be well over 50% in the long run. At that point, if these pilots are taken into production and we’re talking about tens of millions in revenue, the value of Corehw can be calculated with growth company multipliers. With a 50M revenue, the value could be around half a billion, especially if the EBIT% is high.

Another interesting growth area for the same company is automotive. There has been a clear investment in this sector, and I recall a mention in an interview that the most challenging project to date has been specifically for automotive. The partner is a Fortune500 company. If they can get their own product through there at some point, it will take the company another step forward. When a tier1/OEM adopts a Corehw innovation, we’re talking about multiplying money. This could be, for example, radar/ADAS. More about this or its applications here: 81GHz Radar Transceiver IP | CoreHW

A lot needs to succeed for things to really take off and for one to be on the right horse, but there is potential in this Panostaja ownership. If these pilots scale and are competently brought to completion, they will provide excellent reference customers for the next growth step.

Moreover, Corehw operates in a very hot sector that includes IoT/5G/6G/indoor positioning RTLS, etc.

The risk profile is relatively moderate because the design services themselves practically finance the costs, and the product business comes on top as an option.

By far the most interesting and potential value-exploder is this Corehw.

Oscar is becoming a net debt-free company that has launched a cloud-based version of its ERP system. If some growth can be achieved here, a continuous operating profit of 500k/Q is quite possible; hopefully, growth will continue/accelerate from here.

In my opinion, Grano has now been put in a sellable condition as much as possible in this economic situation and sector rotation. I don’t expect anything groundbreaking on that front. However, an improvement in the Finnish economy would certainly make the sale a bit easier. Sokopro has already been carved out of Grano, and GranoDiesel was also put up for sale. Hopefully, they can sell that company at the right time “in this moment” and focus on developing these technology companies or acquiring potential new ones.

Perhaps I’m looking at things through rose-tinted glasses, but for the first time in a long time, Panostaja, in my opinion, has interesting companies in its portfolio that, if successful, have the potential for significant returns. Let’s hope that 2026 is Corehw’s year👍

I’m also attaching a link here that sheds quite a bit of light on all the areas of operation, as well as mentioning the Fortune500 partnership.

Oscar’s recurring revenue continues to grow, otherwise the economic cycle is not favorable.

CoreHW saw a slight decrease in turnover and especially in operating profit. The reason for this is here:

“CoreHW’s turnover for the review period was EUR 2.5 million, down from the comparison period (EUR 2.9 million).

The operating profit for the review period was slightly negative at EUR -0.1 million (EUR 0.6 million).

The profitability level was particularly affected by the full commencement of planned depreciation for own indoor positioning product solutions during the review period, after product certifications were completed in the previous quarter.

Customer project activity for design services remained at a good level during the review period, and the company won several further development projects for existing customers.

Active sales work for design services has continued during the review period, focusing especially on its own IP portfolio. The workload for design services is expected to remain at a good level in the coming quarters as well.

CoreHW continued commercialization activities for its own products during the review period. Successful pilot installations were carried out for industrial customers in the Japanese market during the review period. Interest in CoreHW’s indoor positioning technology has remained high in the Japanese market. We expect broader industrial installations to take place during 2026. With the pilot installations of the current financial year, we expect to reach an annual turnover of approximately one million euros in product business by the end of the financial year.”

Lenio has only been involved since 1.6.2025, and too much shouldn’t be expected for the initial phase. However, it seems that the start has been a bit slow: 0.2 MEUR in revenue was achieved in 08-10/25, and for the full year 1-10/25, ARR growth is 8%. I compared that to Panostaja’s Q3 report, and at that time, ARR growth for 1-7/25 was 9%. And for comparison, Inderes’ revenue expectation from the comprehensive report for 2025: “In our forecast scenario, we have assumed that in 2025, growth will be approximately 25% and revenue will rise to the level of 0.9 MEUR.”

Lenio’s figures are small and (still) insignificant in Panostaja’s overall context. But noteworthy is the shortfall that immediately begins to emerge and falls short of expectations. In relation to the purchase price paid, the first acquisition in seven years has not started particularly well under Panostaja’s leadership.

You asked good, relevant questions @Olli_Vilppo in the recent interview, thank you.

That Hygga write-down/cleanup turned out to be quite a disaster and a continuation in Panostaja’s track record: Write-downs of receivables close to 7 million euros! Oh my goodness . That certainly burned the parent company’s room for maneuver for new acquisitions in an unfortunate way, to put it mildly. Starting at 13:02 in the video. Such a matter should have been the first sentence of the Q4 report.

It will be interesting to see how the sum of the parts crumbles in Inderes’ analysis and what will be done with the investment company discount. That discount is already a big percentage, but this just got even gloomier.

One would think that the sale of Grano Diesel will yield a decent sum. I don’t believe the room for maneuver will narrow.

For the past 5 years, it hasn’t been about room for maneuver, but about not finding anything to buy . Or perhaps there is, but the price hasn’t been valid for Panostaja.

Hopefully now Corehw will take off big so all efforts can be used for developing the current ones. When looking at the Corehw news from Tommila’s interview, I still had very positive and encouraging thoughts. I still see Corehw as a real game-changer driver for all of Panostaja, and my own view is that it will happen next year.

The entire RTLS sector is believed to grow at an annual rate of 20% until 2030, when the market is seen to be 3 times larger than the current market.

I also see that Corehw has many other potential projects that can still rise to support revenue. Especially the automotive sector.

These various pilots and partnerships are unlikely to be disclosed for a long time due to non-disclosure agreements, but I believe these customers are consistently very large.

Corehw’s employee count has been increased by almost 20% within a year, which strongly suggests that the company is preparing for growing volumes and good prospects.

Who thinks so? If it had been worth a stock exchange release, a stock exchange release would have been issued. In other words, Grano sold its 51% stake to Grano Diesel’s main owner. And Panostaja owns just over 50% of Grano. So the sum will not go to Panostaja, but hopefully Grano’s net debt has decreased.

Nothing has been bought in the last 5 years, except now Lenio in summer/2025. But calculate the administrative costs for five years. The management “didn’t find anything to buy,” but they certainly raised their salaries for the last 5 years.

I don’t want to be mean, but this is the most important thing: Watch Inderes’ Q4 video, time 10:52 - 11:03. What do you think the CEO’s feeling about Corehw looks like?

It would be interesting to hear Inde’s analyst’s opinion on the fact that nothing suitable for acquisition has been found in five years.

My impression is that the financial market has been particularly favorable for buyers, as it has been very difficult for SMEs to find financing in recent years.

@Olli_Vilppo Is it known if Panostaja has receivables from Gugguu? Its situation is starting to look unsettlingly grim. Chronically loss-making and revenue is still declining. Also, megatrends do not provide support for the coming years: Among affluent young adults, there are fewer families with children in the Nordics than before. Demand for expensive children’s clothing is unlikely to be growing. The balance sheet valuation is EUR 1.5 million, but are there also receivables tied up in Gugguu on top of that?

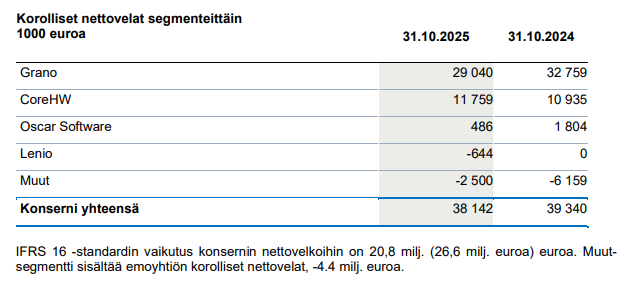

Gugguuta is not consolidated as an associate company into the group, so its interest-bearing debts do not appear in the group’s net debt. In any case, there is now better visibility into Panostaja’s 4.4 MEUR net cash (including interest-bearing receivables), as the parent company’s cash and financial assets, as well as liquid fund units, amount to 1.8 million euros, and a 2.2 MEUR product development loan granted to CoreHW, which already totals 4 MEUR. That 7 MEUR intercompany receivable granted to Hygga was indeed hidden, as by summing up the net debts of the group companies, intercompany receivables appeared to be a total of 7 MEUR from all group companies in the previous report, but now it turned out that they were all granted to Hygga. As I wrote in the report, the scale was a very negative surprise. I called the CFO about this on Friday evening, asking why it doesn’t go through the income statement. It’s because, from the group’s income statement perspective, no money was lost when Hygga Flow received a 7 MEUR loan write-off and the parent company’s cash decreased by 7 MEUR, leaving the group’s net debt unchanged at 38 MEUR, even though this was a cold shower for Panostaja’s owners, as Hygga Flow’s value hardly increased.

@Olli_Vilppo What about the expected sale price of the clinic business, 2.8 MEUR? If the deal goes through, will it increase the parent company’s net cash by 2.8 MEUR at the turn of January-February? Or is that sum already “baked into” some line item?

As I understand it, it only reduces debts, as Hygga had 9.7 MEUR in net debt before the deal, and subtracting the 2.8 MEUR received from this leaves exactly 7 MEUR in losses, which came from cash.

As a general comment from a small investor to Panostaja, I would say that the Q4 reporting was not, in my opinion, entirely honest. Clearly stating the 7 MEUR write-down is part of the responsibility that Panostaja itself emphasizes. Instead, it had to be deduced from various figures and the placement of the ‘other - discontinued’ segments. Not like this. A big minus for ESG, and bad news should not be hidden, even if the last 10 years have gone more or less poorly.

In my opinion, this should also have been explained more clearly. But at least now we were able to properly fulfill our mission and serve both the company and you, the investors, by making investor communications clearer.

The reason that investment targets ‘have not been found’. Is, in reality, that there has been no cash? The reporting of net cash has misled the owners.