4,500 + 700 car benefit vs. a salary of 5,200 without a car benefit. The side costs for the company are exactly the same.

In that case, side costs are paid on the 5,200, and mileage is paid tax-free without side costs. Of course, the mileage allowances are then added to the company’s expenses, which increases variable costs.

That’s right. However, the actual costs of the car to the company can be more or less than that taxable value, and side costs are still calculated according to the taxable value.

Taxable values for zero-emission cars have been reduced for the years 2021-2025 by €170/month for the limited car benefit (käyttöetu) and by €290/month for the full car benefit (vapaa autoetu). (The reduction in the taxable value of the full car benefit is €120/month if the car’s only power source is electricity. And for fully electric cars first registered after 2020, there is an additional €170/month deduction from the car benefit.)

Providing such an electric vehicle company car benefit to an employee feels particularly tax-efficient.

Hourly wage is just over €16. Working as a nurse in specialized healthcare. Work experience is just under five years. Next raises in summer '23 (thanks to the SOTE agreement), and a small raise is also coming when I hit the five-year mark at this place.

Sometimes I do think that for this salary, I wouldn’t be very tempted to work 8–4 shifts from Monday to Friday (currently doing shift work). Why I enjoy the field—probably the interesting work, a good team, the public sector vacation policy, and shift differentials play an important part!

Working in product development in the financial sector, with total annual earnings of 85-90k (monthly + bonus + lunch). Almost 35 years old with a UAS (University of Applied Sciences) background. I live outside the Ring Roads.

10 years ago when I was at the start of my career, I earned €2600/month. Now I earn €4600/month. I pay the same amount for my mortgage as I did back then. My son has grown up, and that obviously brings expenses. However, I’m thinking that even though my gross is 2k higher, my quality of life is still the same. Granted, it’s still a small salary, but still. Should I stop chasing the euros and settle for a job I enjoy and where I can take it as easy as possible? Of course, every euro invested is a plus, and you can invest more if your salary allows for it.

It would be interesting to hear from people in different income brackets:

-Gross income

-Net income

-Percentage of taxes and tax-like expenses

-Amount and details of various tax deductions.

I’ll start:

-Gross €2630

-Net €2121

-Taxes and other fees 19.4%

-Tax deduction for commuting (approx. 85km/workday) + approx. once a year some small renovation/other task, which qualifies for a small household deduction.

Good earnings in product development Out here in the periphery, branch managers are barely at those income levels. Although, if the title is something like ‘Head of…’ in an insurance company, for example, you’re quickly at those levels and even above.

Small salary? If you’re more than a thousand over the median, that’s pretty far from small.

I’ve personally found the perfect balance for my daily life. My net is about two grand a month, or maybe a bit more. Investments and such cover any occasional larger expenses. The missus earns a bit less.

You can’t have expensive hobbies or drive new cars with that, but I’ve never had a need for those anyway. Tax-wise, it’s at a pretty optimal level, as the tax rate is low but starts rising very quickly after this. Extra income would require overtime and long weekends, which isn’t very appealing.

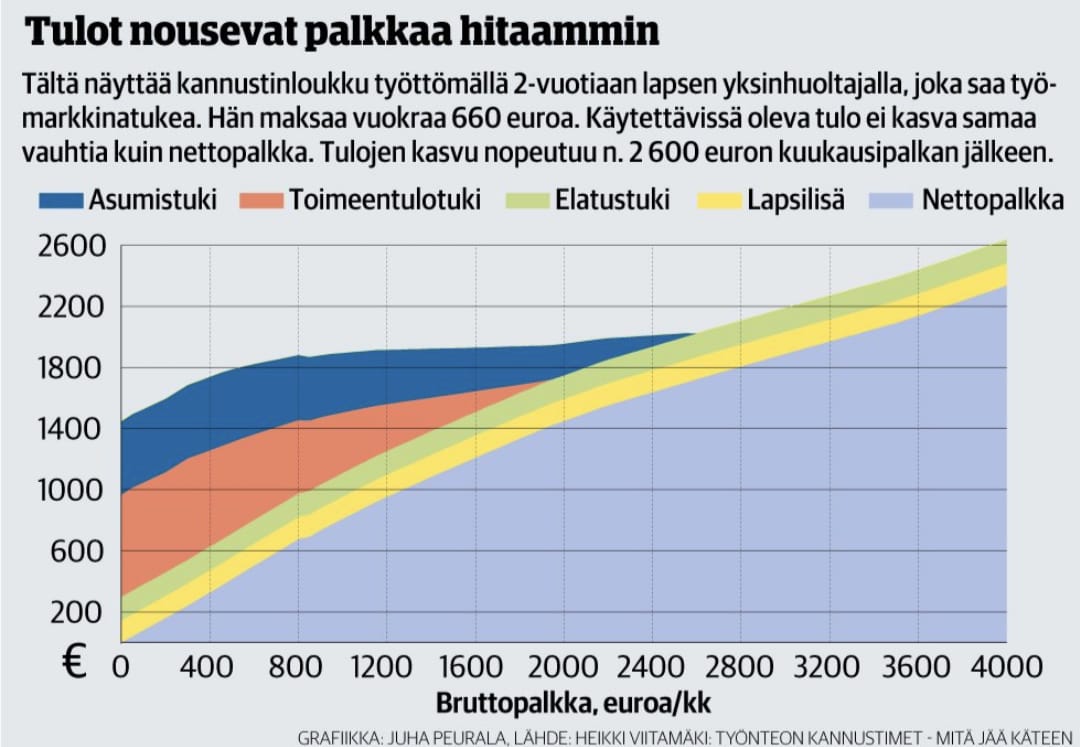

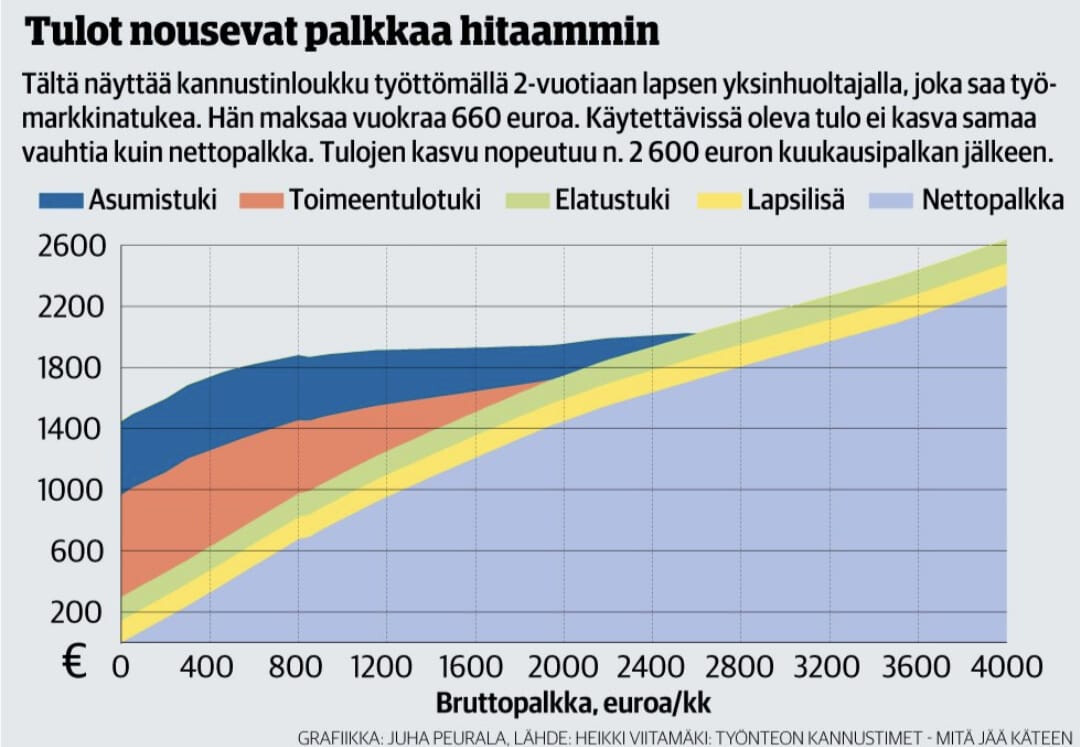

The incentive trap reminded me of this news story:

Then I did my own calculations on the matter, specifically the net income of a single parent with two children at different salary levels and benefit amounts. This trap looks quite grim and it certainly doesn’t encourage working.

Case 1:

Gross salary €1,500/month

Basic allowance €19.6/day x 21.5 days = €421/month

Child benefits 95+105 = €200/month

Housing allowance €740/month

Taxes 16.4% i.e. €315/month

Net income €2,546/month

Case 2:

Gross salary €2,500/month

Daily allowances €0/month

Child benefits €200/month

Housing allowance €545/month

Taxes 22.5% i.e. €586/month

Net income €2,659/month

So if you were working 60% hours, switching to full-time would only increase your disposable net income by €113/month.

This can also be extended upwards:

Salary 3500

Daily allowance 0

Child benefits 200

Housing allowance 209

Tax 29% i.e. 1057

Net income €2,852/month

Salary 4500

Daily allowance 0

Child benefits 200

Housing allowance 0

Taxes 33.6% i.e. 1575

Net income €3,125/month

When you triple the gross salary, the take-home pay only increases by 22%.

If you look further ahead and try to see the benefits of aiming for a higher salary, when children turn 17, €200 disappears from your income; a year later, the child increments on daily allowances end, and as the children move out, the housing allowance also decreases. Additionally, if you still believe in pensions, a €2,500/month salary adds €15/month more to your pension for every year worked compared to a €1,500/month salary.

Well yeah, but to put it bluntly, I’d say that no one should pay more than 25% in tax. I’d like to know what we do differently in Finland compared to, for example, Denmark and Sweden. I’ve always worked hard myself. I’ve almost always held two jobs, one of which was a so-called “crap job,” such as cleaning, security, and property maintenance. Even now, four years after quitting, I get calls asking if I want to come to work because they can’t find workers for these jobs. I’ve sometimes wondered if I lived in a rental and did one of these as a day job, would I even bother going to work.

I don’t know what working life in Sweden looks like, for example, but someone posted a study here showing that the Swedes are getting wealthier, and we aren’t. I’m guessing we’ll see a lot of strikes in the future, especially if inflation continues.

I’d take that. Last year, however, income taxes and these other tax-like charges (pension contributions, etc.) accounted for over 45% of my gross salary.

Having an extra 2500€/month in take-home pay with those taxes would certainly be quite nice.

And if only it were understood at the decision-making level that the extra €2,500 in the example brings in tax revenue through consumption to boost the state economy.

Thanks to the wonderful stock option taxation, I ended up with a tax rate of over a hundred percent on my salary in 2021. And yeah, some illiquid stocks.

What part of the graph would people here change to eliminate that incentive trap? I personally find this topic/problem really difficult, because if you reduce benefits at, for example, that mentioned €1,500 (gross income) point, the incentive trap just shifts.

I see that regarding social assistance, there could perhaps be some trimming across the board; I believe a single parent of a 2-year-old can manage while unemployed on less than that €1,400, which appears to be the minimum possible disposable income.

The biggest problem is probably when a person moves onto social assistance.

When you have 550-600€ left in hand from basic unemployment allowance after taxes, + possible housing supplement, according to the housing allowance calculator, a single parent of two living in Helsinki with a 750 euro rent would get 550€ in housing allowance, from which the taxman takes about 100€? and child benefit 200€, then in my opinion, in this equation of 1250 euros net income where the rent share is 750€, doing extra work already starts to interest you. Having been on basic unemployment allowance for a long time myself, the biggest motivation is the decrease in the tax rate, as benefits are taxed significantly more than earned income, meaning you benefit from even a small amount of work for the rest of the year.

The fact that at some point, as work increases, an “incentive trap” might occur when benefits are dropped one by one, is in my opinion a lesser evil than someone not starting work at all.

Regarding social assistance, on the other hand, about ten years ago when friends graduated from school, I know many who stayed living on social assistance. Living alone, you got that same approx. 1200€ in hand per month, and if someone thinks this is a little, we’re talking about people who before this had lived on a 450 euro combination of student grant + housing supplement. 750€ more in hand per month for the effort of having to haul all the bills to the employment office, so there was simply no motivation there to do anything. At the end of the month, they would sit in the cinema for hours just so that the account could be emptied during the month.

It looks like it’s from 2017, so it is an older chart. It illustrates the situation visually, but the details might not necessarily be accurate.

No, and in addition, the calculation is missing the single-parent supplement to the child benefit and any potential maintenance payments or child support.

Just to clarify: the image is indeed from the internet and contains what it contains. My own calculations were made using 2023 data, which doesn’t take into account all the same factors as the graph, but only those specifically mentioned in the calculations.