Thomas has provided a preview as Orthex reports its Q1 results on Thursday, May 7th.

We expect the company’s revenue to have returned to a growth path after a weak end to the year. The company is facing a soft comparison period, during which sales in European export markets fell sharply as a result of increased customer credit risks and the consequent restricted deliveries. Our focus in the report is particularly on the impact of raw material inflation caused by the Iran conflict on the outlook for the rest of the year, as well as the company’s pricing strategy to mitigate these effects.

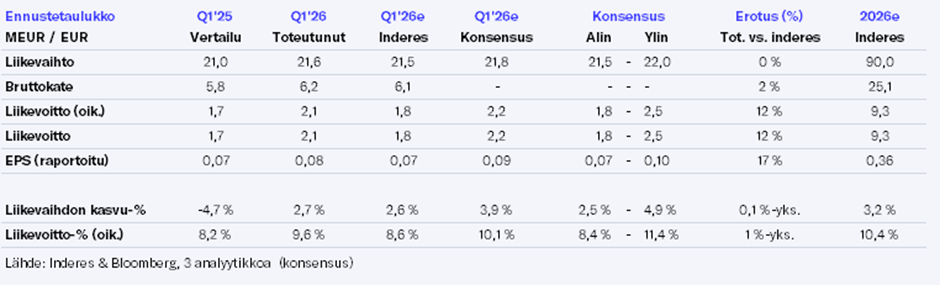

Net sales increased by 2.7% to EUR 21.6 million (21.0)

Adjusted EBITDA was EUR 3.4 million (2.9)

Adjusted EBITA was EUR 2.1 million (1.7), or 9.6% of net sales (8.2)

Net cash flow from operating activities was EUR 3.5 million (4.7)

Net debt / Adjusted EBITDA was 1.0x (1.2x)

Earnings per share, basic, was EUR 0.08 (0.07)

As a result of higher oil prices due to the crisis in the Strait of Hormuz, raw material prices began to rise in March, but this did not yet have an impact on the company’s profitability.

The realized figures were good, but the comments regarding the future outlook and raw material prices were not very pleasant reading. Although not surprising.

It’s a shame, as otherwise there now seems to be good development in Europe.

The results exceeded my forecasts but fell slightly short of the consensus. There was solid 16% growth in Rest of Europe markets, and the Rest of the World also came back to life during the quarter. Regarding growth, it is worth noting that exchange rates provided a tailwind in Q1, and currency-adjusted revenue actually contracted by 0.4%. Raw material prices still supported profitability development in Q1. A better-than-expected gross margin and a lighter cost structure drove an earnings beat relative to my forecasts. Overall, I think it was a good report; regarding growth, it is of course a pity that the exchange rate effect played such a central role.

Compared to the review period, the outlook naturally paints a more subdued picture. Management commented quite directly that from Q2 onwards, the impact of raw material prices will be visible in the figures. Consequently, price increases have already been initiated, but these will take effect with a lag, and I don’t believe they will be fully passed on to own prices. Therefore, margins will presumably be under pressure until oil prices decline.

Am I misremembering, or was it once mentioned that regarding price increases, the goal is to maintain a single permanent direction? In which case, one could think that moderation and back-loading are the price paid to ensure they aren’t immediately adjusted back down.

Alexia could challenge them a bit in the Q&A regarding price pressures and whether she is ready to flush the 2026 results down the toilet again through inaction? The increase in price pressure was already visible during the previous earnings release, and some kind of hedging measures should have been taken as part of cost risk management.

At the same time, it should be asked how they are failing to keep up even with general economic growth in their main markets. The atmosphere seems a bit too patient (inactive), and the company desperately needs an activist investor or a private equity firm in the driver’s seat. Conficap has proven to be quite passive as well.

One can always blame the circumstances, but there are now 5 wasted years behind us.

Why is the company even listed?

Edit: personally, it bothers me that she leads the talk at Rapala (this company is also on the ropes) and can’t get “her own” going either. Time for a change.

I can’t quite formulate a specific question right now, but it would be interesting to get a sense of the potential for international growth (outside the Nordics)—specifically, how much the company can realistically grow internationally with its current products, factories, logistics, and pricing. At the current pace, it would only take about 10 years for international sales to overtake Nordic sales, provided nothing changes and such growth remains feasible.

There seems to be a constant bottleneck in operations right now, so it would be good to hear how the company itself intends to achieve sustainable momentum in its execution.

00:00 Introduction

00:16 Q1 Key Highlights

01:38 Growth & Risk Appetite

04:35 Competitive Landscape

05:52 Development in the Nordic Countries

08:21 Growth in Export Markets

10:20 Bottlenecks in the European Market

11:31 Sales Outside Europe

12:12 Impact of the Middle East Crisis

13:56 Raw Material Costs and Pricing

15:00 The Role of Campaigns in the Future

15:43 Consumer Demand

16:23 Raw Material Availability

Good interview @Thomas_Westerholm, 5/5. For once, there was a bit more substance and emphasis.

Of course, the recommendation remains at “reduce” and the target price might even drop a bit, but Orthex needs to start reaping the rewards of the long-term work that Alexander emphasizes despite the headwinds.

The Container Store returning as a customer, or an ordering customer, was quite interesting. Apparently, Bed, Bath & Beyond has acquired it, and at least for now, Orthex’s branded products are not found in the BB&B online store. For a moment, I also imagined the potential was huge, until I remembered that BB&B has also suffered from severe financial challenges in recent years and has practically been revived as an e-commerce concept by new owners following a bankruptcy. And The Container Store’s Orthex selection is also very limited, so there is plenty of work to do to secure a larger piece of the pie.