Antti’s comment on the guidance:

14 Likes

Siltanen has also produced a company report ![]()

Orion published on Wednesday its outlook for 2026 and an estimate of the revenue potential for its blockbuster prostate cancer drug Nubeqa. The guidance exceeded our expectations in terms of revenue, and the midpoint of the earnings guidance is also higher than our forecasts. Additionally, the company specified Nubeqa’s long-term revenue potential to over EUR 1 billion. The potential is in line with our forecasts (2030). The market rewarded shareholders with a sharp rise in the share price. We are raising our forecasts following the new information. Corresponding to the forecast hikes, we raise our target price to EUR 75 (prev. 66) and reiterate our Accumulate recommendation.

9 Likes

Siltanen’s thoughts on Orion and Nubeqa’s strong momentum can also be heard in a new video filmed today. ![]()

“The success of the cancer drug Nubeqa is like a story written in the stars. Orion estimates its share of Nubeqa sales will exceed the one billion euro mark by the end of the decade. The stock is at all-time highs and growth drivers are in place, but where will future returns be built from when Nubeqa’s patent protections eventually expire?”

Topics:

00:00 Introduction

00:23 Nubeqa sales are only accelerating

02:02 Strong earnings leverage

02:41 Long-term return potential

03:57 Political and regulatory risks in the United States

05:45 What after Nubeqa?

09:25 Is Orion still cheap?

10 Likes

This was a good overview of the long-term outlook:

-One could say that until around the turn of the 2020s and 2030s, aided by Nubeqa and the expansion of its indications, massive amounts of money will be pouring into Orion from all sides.

-Then the patents for this drug will expire by the mid-2030s, and new products may emerge from the R&D pipeline.

-It should also be noted that currently, all of Orion’s divisions are in quite good shape, meaning no catastrophe is in sight, even if the R&D pipeline doesn’t produce a new blockbuster hit.

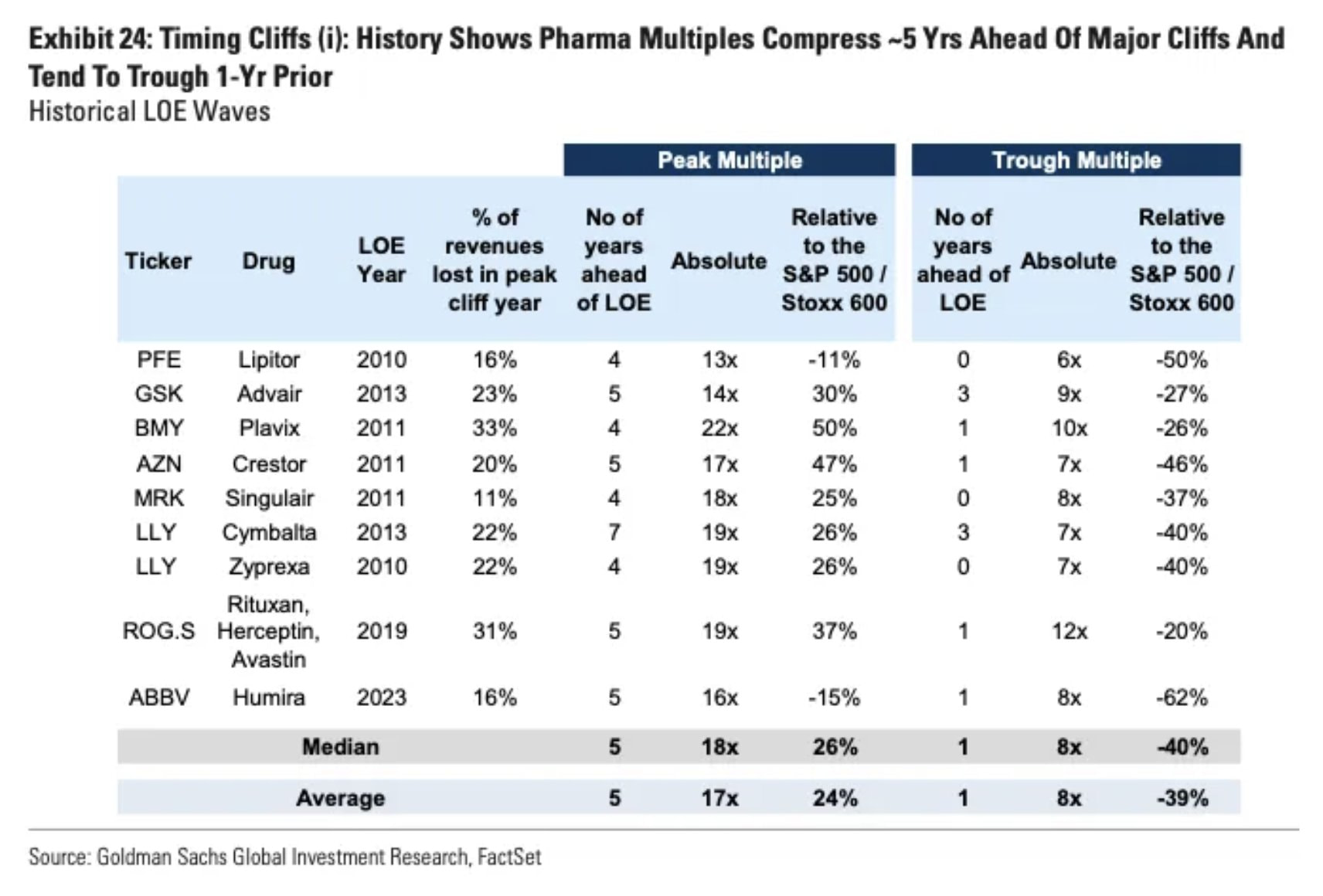

-The information in the report was interesting: the impact of an expiring patent starts to show in the company’s stock pricing 4–6 years before the actual expiration. In Orion’s case, this would mean the very end of the 2020s, but at the same time, the expansions of Nubeqa’s indications might materialize. So, would this create an offset?

-I was left wondering where all that money pouring in will be invested: acquisitions, implementing the global strategy, extra dividends, or what? My guess is that something will happen on this front, meaning we will see some new initiatives from the company in the coming years.

-The timing of this video’s release was relevant in that the trade war scenario discussed in it landed right in our laps immediately. This morning’s news cycle from the US reported that Trump has set his sights on those pharmaceutical companies that haven’t yet reached an agreement with him on drug price reductions. These include, among others, Bayer/Orion. So, it’s not out of the question that “more is to follow” and we’ll soon need to create new future projections for Orion as well.

11 Likes

I personally see Orion’s major risk lying in acquisitions. They might buy some drug development company at a high price, only for the drug to ultimately fail. Of course, their own drug development doesn’t always succeed either. So while everything looks good now, there are risks along the way.

4 Likes

Here is the data I was recalling from memory in the interview:

7 Likes

Nubeqa’s patent protection is expected to remain in effect beyond 2030. Xtandi, which is Nubeqa’s direct competitor in the US prostate cancer market, currently holds the largest market share and is expected to face generic competition at the end of 2027, which will likely lead to a significant price reduction for Xtandi.

In this situation, would it be reasonable to assume that pricing pressure on Nubeqa could begin as early as the end of 2027, well before the expiration of its own patent protection, if Bayer is forced to lower its price to defend its market share against a cheaper generic competitor?

5 Likes

On Orion’s outlook and stock pricing:

“Despite high expectations, Orion’s share is not yet particularly expensive, and not necessarily even fully priced. The valuation of the share, which has strengthened by nearly 40 percent over the year, has tightened, but the pricing has not become excessive.”

4 Likes

Posting this here as well: @Marianne_Palmu and @Kaisa_Vanha-Perttula added Orion to the Femme Portfolio. ![]()

4 Likes

Here are Antti’s preview comments as Orion reports its Q4 results on Thursday. ![]()

We expect a very strong finish to 2025 for Orion, driven particularly by the excellent sales performance of the prostate cancer drug Nubeqa. The company already provided preliminary information on the 2026 outlook in January, which suggests that Nubeqa’s success story will continue into the current year.

3 Likes

And here is the result itself:

Highlights:

October-December 2025:

Net sales totalled EUR 695.3 (October–December 2024: 434.4) million

• Operating profit was EUR 328.1 (92.7) million

• Basic earnings per share were EUR 1.85 (0.52)

• Cash flow from operating activities per share was EUR 0.58 (0.63)

• The outlook for 2026 (provided on 14 January 2026): Net sales are estimated to be EUR

1,900 million to EUR 2,100 million. Operating profit is estimated to be EUR 550 million to

EUR 750 million.

January–December 2025 Highlights

• Net sales totalled EUR 1,889.5 (January–December 2024: 1,542.4) million

• Operating profit was EUR 631.6 (416.6) million

• Basic earnings per share were EUR 3.56 (2.35)

• Cash flow from operating activities per share was EUR 2.25 (2.09)

• The Board of Directors proposes a dividend of EUR 1.80 (1.64) to be paid for 2025. The dividend is proposed to be paid in two instalments.

9 Likes

Verneri Pulkkinen interviewed Orion’s CEO Liisa Hurme about how the company is doing. ![]()

Topics:

00:00 Q4

01:00 Proprietary products

03:20 Easyhaler

04:00 Nubeqa

04:40 Expenses

05:50 China

07:08 Dividend

08:15 Guidance 2026

5 Likes

Here are Antti’s comments on an unsurprising Q4 ![]()

Orion’s Q4 report and the full financial year were strong, even though the end of the year fell slightly short of market expectations. The quarter was characterized by a 180 MEUR milestone payment, adjusted for which the result improved by 59%. The report offered no major surprises or news, and forecast changes remain minimal. The dividend proposal of 1.80 euros (2024: 1.64) met our expectations, and the strong outlook for 2026 was already known before the report. We reiterate our target price of 75 euros and our Accumulate recommendation.

9 Likes

Considering the precarious situation Faron has found itself in, perhaps the possibility of merging it with Orion should be seriously explored. Although Orion might not yet be considered a true Big Pharma (BP) company, a merger with Faron would not be an overwhelming risk for it. Perhaps a couple of million B-shares would be needed for a share swap, which is only just under 1.5 percent of Orion’s share capital, so it would likely hardly weigh on the stock price. It might even raise it. Orion would get more, at least somewhat promising, new candidates for its research pipeline. The EU would probably take an encouraging view of such a solution, and it would also be an interesting step for the development of the Finnish pharmaceutical industry.

8 Likes

And then potentially destroy Orion’s shareholder value in the process. As an Orion shareholder (I don’t own Faron), I do not support such a scenario at all. Deals can be made for interesting drug candidates, if there is potential. On the other hand, if Faron’s performance continues at this level, those assets could be acquired cheaply at some point—if there would even be any sense in that.

And if Faron stays afloat, those who believe in it can certainly continue funding it as an independent company. Drug development is arduous and risky; I trust Orion’s experience in this.

14 Likes

Turku-based Thestra finds a partner in Orion to support its unique invention

Despite decades of research, there have been no targeted treatments for head and neck cancer. A medical startup has invented a method that ensures an accurate diagnosis of the cancer.

11 Likes

Interesting information, the collaboration between Thestra and Orion. The target cancer is a very distressing disease; HNSCC causes great suffering. Head and neck squamous cell carcinoma (HNSCC) can form in the squamous epithelial layers of the oral cavity, larynx, nasopharynx, and oropharynx, from which it can invade and eventually metastasize. It is the eighth most common cancer in the world, and its incidence is expected to grow by 52% by 2045. Those affected by this type of tumor have an average five-year mortality rate of 50%, and survivors have the second-highest suicide rate of all cancers.

3 Likes