Our views on Pfizer and Novo Nordisk in relation to Orion are actually quite similar ![]() , but I have still come to partly different conclusions in these comparisons or I see more uncertainties in the air:

, but I have still come to partly different conclusions in these comparisons or I see more uncertainties in the air:

- The Orion Case

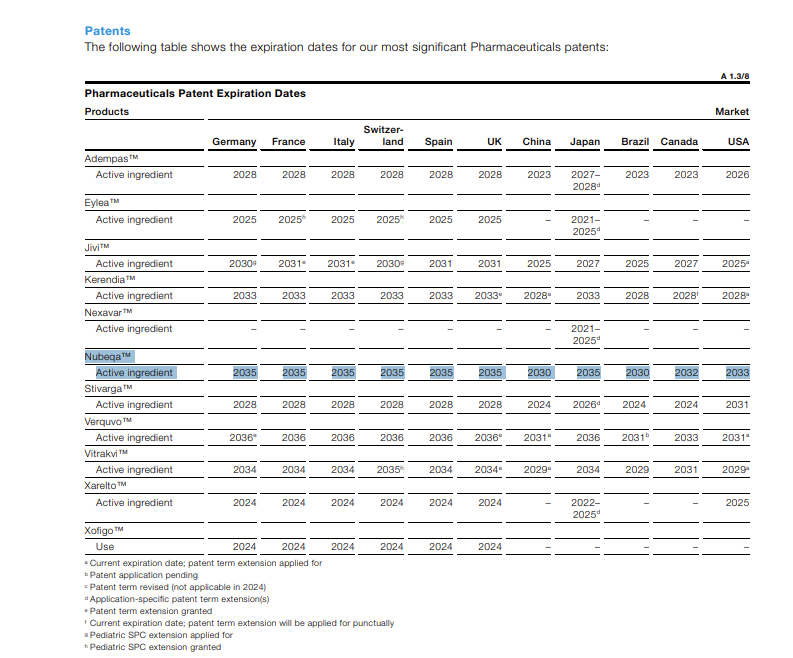

All of Orion’s divisions are comfortably profitable, and Nubeqa is selling like hotcakes. The patents for the latter expire in the 2030s, but its areas of use could potentially be expanded to new targets, and with the company’s other parts operating, expenses remain reasonable, even if not as brilliant as today. This is my own vision, which may prove right or wrong:)

- The Pfizer Case in relation to Orion

It’s cheap, but several patents (about 25% of revenue) are expiring soon, and the entire vaccine business in the USA is under political risk. In addition, for example, the gigantic acquisition of Seagen with its cancer drug focus is still an enigma from a profit perspective. Orion is clearly more expensive, but its robust earning model continues for several years longer, and Pfizer’s outlook is cloudier.

- The Novo Nordisk Case in relation to Orion

It’s cheap, at least compared to before, and many see the share price drop as an overreaction. A stable and profitable company. But, for example, Goldman Sachs estimates that consensus forecasts will have to be revised downwards further until 2028. Morgan Stanley is pessimistic due to fiercely intensifying competition in weight loss drugs, and additionally, MS considers the probability of success for Novo’s Alzheimer’s investments to be rather small. Novo is clearly cheaper than Orion, but even Novo’s near-future prospects raise conflicting assessments. Time will tell which camp of forecasters is right, but Orion’s future prospects are at least a degree brighter until the 2030s.

- The Kenvue Case in relation to Orion

I don’t know Organon, but the other candidate mentioned by @Clark_Kent, Kenvue, is a real wild card. Both Trump and the US Secretary of Health have accused the company’s product of causing autism, causing the share price to plummet. Science does not recognize Trump’s and the minister’s tinfoil hat speeches, and the company is trying to overcome the realization of political risk. If it were to succeed in this, one could now get a potential share price recovery at a low price. It vividly reminds me of Orion’s dip a few years ago when, among other things, operations in Russia ceased, and the stock could be bought for 30+ €.

Thanks @JNivala and @Clark_kent for the good answers!

\n](https://x.com/JuhaVaris/status/1977677892416143670%5Cn!%5Bimage%7C690x170%5D(upload://qDEaA7Kvf4UHnqcTE3Uoaxn2TBl.png)%5Cn!%5Bimage%7C686x500%5D(upload://erVPy3aCNZsvs3PjaH2KO37qpNd.png)){kind=link}