This might be a stupid question, but could Olvi somehow “wash” that money stuck in Belarus by buying back its own shares? By using those funds for that?

The money still needs to be gotten out of Belarus for the purchase regardless. A subsidiary cannot buy the parent company’s shares and cancel them. Sure, it could somehow just buy Olvi shares, but I don’t really see how this would be any easier than any other way of transferring money out of there.

Edit: If the money can be gotten out, then great; otherwise, I think the most sensible thing is to continue operations there until someone buys it out or it goes bankrupt.

3 Likes

I think the original suggestion regarding those shares bought by the subsidiary came from me, and it is indeed a bit of a silly idea as such, but funds can be maneuvered in the most creative ways for the benefit of the parent company.

2 Likes

At least I don’t have a clear understanding of what kind of restrictions are involved here.

Belarus is restricting foreign (mainly Western?) companies in some way.

But are there also restrictions from Western countries against Belarusian companies (Olvi’s subsidiary)?

In which case, cash flow (i.e., out of Belarus) would be squeezed from two directions. Of course, the hit to cash flow from the Belarusian side alone is negative enough.

1 Like

It is indeed one scenario that once peace returns, Finnish trade via Russia and Belarus will also slowly recover. In this way, the pressure on Olvi to leave completely will also gradually decrease.

4 Likes

Since Olvi has been asserting its intent to exit the market for some time, but stating that it is not possible (which it isn’t), reversing that decision would certainly be a significant hit to its reputation. And they would surely hear about it and be reminded of it for a long time. Even though 95% of consumers couldn’t care less about the matter, much like ethical issues in general.

The situation would, of course, be different if Belarus’s political environment were to change completely and democratize. I wouldn’t count on that much.

1 Like

Here is the annual report for those who are interested in reading it.

5 Likes

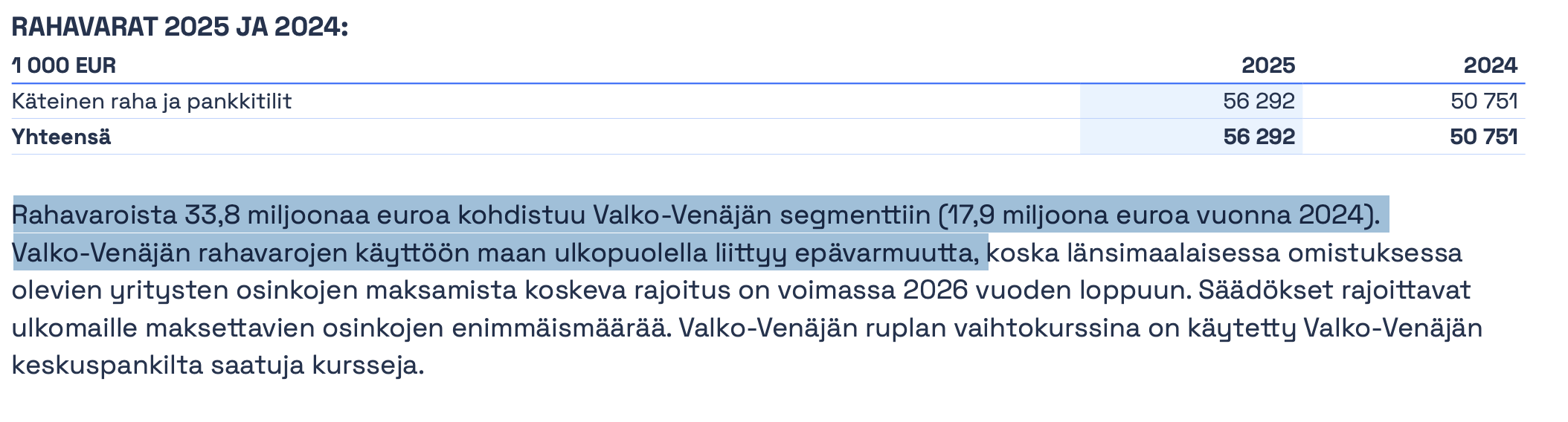

As much as 60% of Olvi’s cash assets are frozen in Belarus. Olvi continues to invest more in other countries than its depreciation and is making acquisitions. As a result, dividends are in practice partially financed by taking on debt. Olvi has indeed become more active in taking out more loans during the 2025 financial year than, for example, in the previous year.

Olvi certainly has a good balance sheet otherwise, but as a shareholder, I want to highlight this issue, just like I did a year ago. Management does not communicate about these matters beyond what is legally required. Everyone has to dig up this information themselves, even though I consider it a quite significant matter.

30 Likes