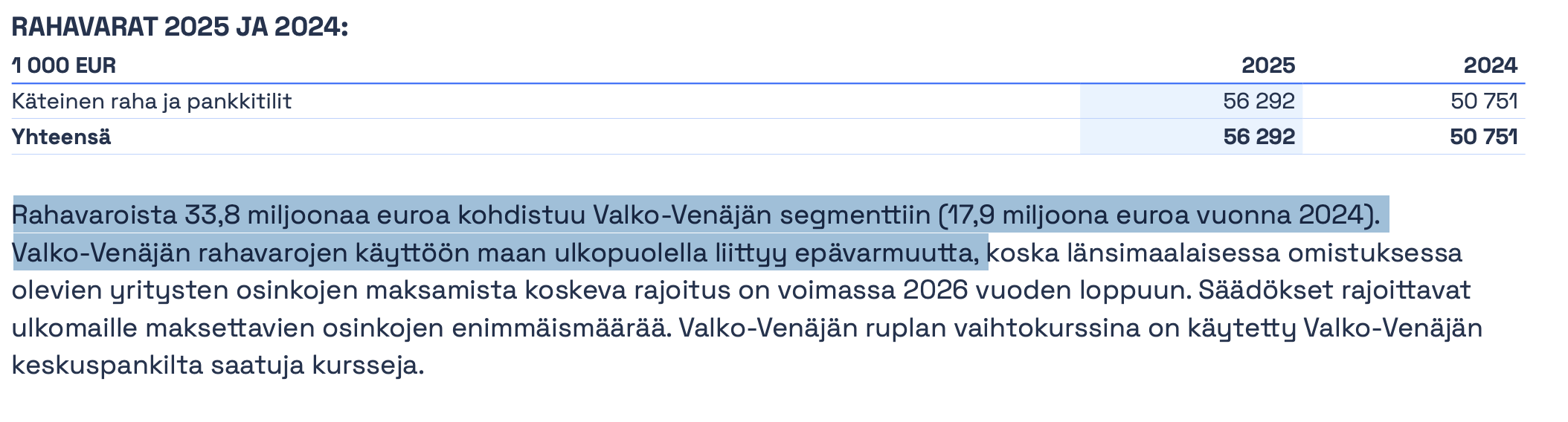

As much as 60% of Olvi’s cash assets are frozen in Belarus. Olvi continues to invest more in other countries than its depreciation and is making acquisitions. As a result, dividends are in practice partially financed by taking on debt. Olvi has indeed become more active in taking out more loans during the 2025 financial year than, for example, in the previous year.

Olvi certainly has a good balance sheet otherwise, but as a shareholder, I want to highlight this issue, just like I did a year ago. Management does not communicate about these matters beyond what is legally required. Everyone has to dig up this information themselves, even though I consider it a quite significant matter.