“Deep dive” sisältää 37 minuutin videon jos ruotsi taipuu

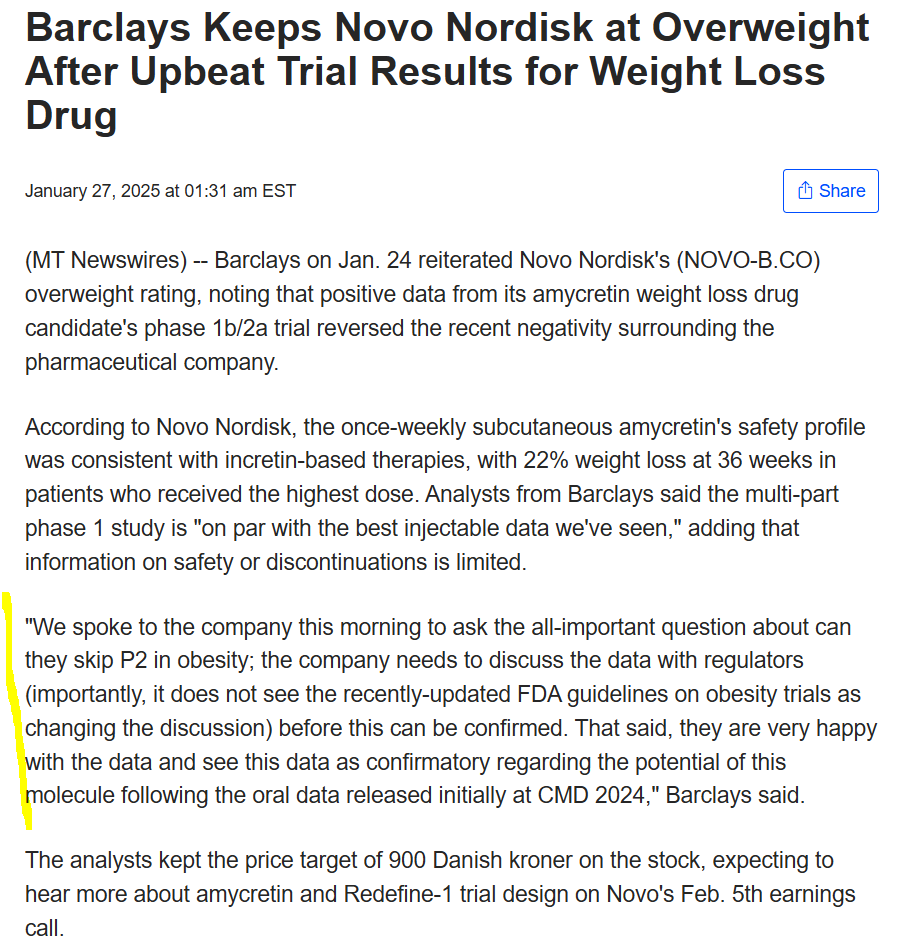

Hän mainitsee helmikuun 5. päivän tilinpäätöksen ratkaisevana laukaisijana. Sen lisäksi, että Novo Nordisk esittelee sitten koko vuoden ennusteensa vuodelle 2025, yhtiö on tuolloin voinut saada käyttöönsä myös vaiheen 3 tutkimuksen tulokset kuuden viikon ajan. Morten Larsenin mukaan ei ole todennäköistä, että Novo Nordisk jakaa tilinpäätöksessä yksityiskohtaisia tietoja suuriannoksisen Cagrisema-ryhmän painonpudotukseen – mitä markkinat todella vaativat. On todennäköisempää, että täydelliset tulokset esitellään konferenssissa kesäkuussa. Samalla tulevat sijoittajatapaamiset 6. ja 18. helmikuuta voivat tarjota arvokkaita oivalluksia.

Tällä hetkellä yhtiö tarjoaa yhden houkuttelevimmista tuloskasvuluvuista, ei vain Skandinaviassa vaan koko terveydenhuoltoalalla.

Tässä on vielä siitä, miten FDA hyväksyi tänään tiistaina Novo Nordiskin Ozempicin käyttöön kroonisen munuaissairauden hoitoon tyypin 2 diabetesta sairastavilla potilailla. Tämä laajentaa lääkkeen käyttöä, sillä se voi nyt estää munuaissairauden pahenemista ja vähentää sydänsairauksiin liittyvää kuolemanriskiä. Ozempic vähensi vakavien munuaissairauksien riskiä 24 prosenttia verrattuna plaseboon.

Ozempic reduced the risk of severe kidney outcomes — including kidney failure, reduction in kidney function, or death from kidney or heart causes — by 24% in diabetic patients with chronic kidney disease compared with a placebo, according to results of a late-stage trial that the approval was based on.

Kyselin Geminiltä, onko parempaa tietoa asiasta?

Novo Nordiskilla on tuotantolaitos Yhdysvalloissa, mutta on epäselvää, tuottaako se lääkkeitä Yhdysvaltain kysynnän verran. Novo Nordisk on maailman johtava diabeteksen hoitoon keskittyvä lääkeyritys, ja sillä on tuotantolaitoksia useissa maissa ympäri maailmaa. Yhtiön verkkosivuston mukaan sillä on 16 tuotantolaitosta yhdeksässä maassa, mukaan lukien Yhdysvallat.

On kuitenkin tärkeää huomata, että lääkkeiden tuotanto on monimutkainen prosessi, johon liittyy monia tekijöitä, kuten raaka-aineiden hankinta, valmistus, pakkaaminen ja jakelu. Lisäksi lääkkeiden kysyntä voi vaihdella suuresti eri maissa. Näistä syistä on vaikea sanoa varmasti, tuottaako Novo Nordisk Yhdysvalloissa lääkkeitä Yhdysvaltain kysynnän verran.

On kuitenkin todennäköistä, että Novo Nordisk tuottaa Yhdysvalloissa merkittävän määrän lääkkeitä, koska Yhdysvallat on yksi yhtiön suurimmista markkinoista. Lisäksi Novo Nordisk on sitoutunut varmistamaan, että sen lääkkeet ovat saatavilla kaikille niitä tarvitseville.

En ainakaan analyytikkoseurannoissa ole nähnyt isommin tulleilla spekulointia. Ennemminkin kilpailutilanne vs. LLY jne. puhuttavat.

Konsensus edelleen käsittääkseni on, että seur. 5v aikana NOVO+LLY vievät noin 95% GLP-1 markkinoista

JPM on pohtinut sitä, että merkittävä osa käyttäjistä lopettaa GLP-1-lääkkeiden käytön vuoden sisällä. Syitä ovat sen sivuvaikutukset (esim. ruoansulatusvaivat), pistosten tiheys ja suun kautta otettavien versioiden heikompi tehokkuus painonpudotuksessa.

https://x.com/TidefallCapital/status/1885272771573186832

Novo Nordisk has had its price target lowered by Danske Bank to DKK 880 from DKK 1075 ahead of its financial results on Wednesday, where the recommendation “buy” will be reiterated.

When publishing the annual report, Danske Bank hopes to get answers to a number of questions.

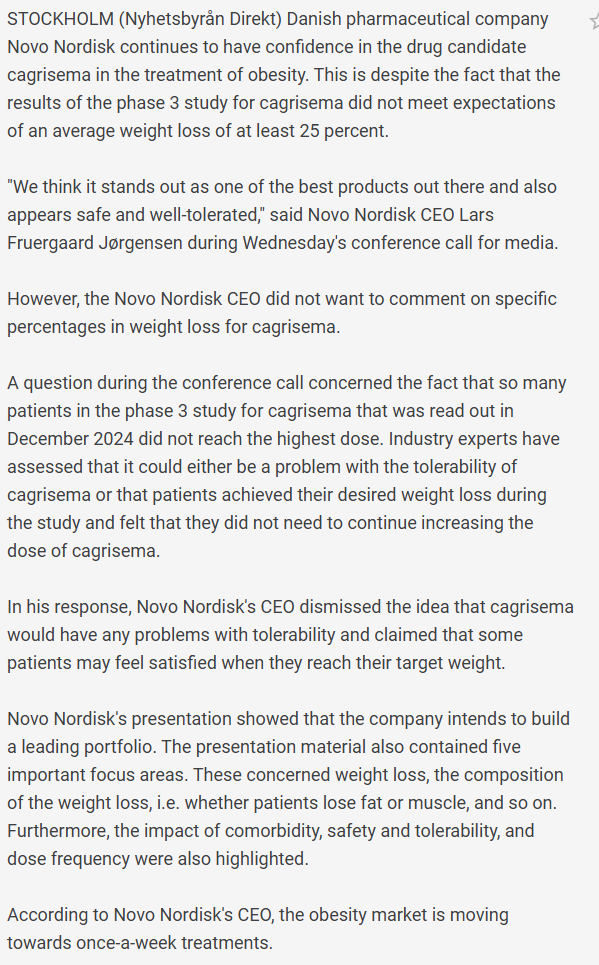

Most notably, there will of course be questions about the recently announced CagriSema phase 3 trial and its lower-than-expected weight loss results. We hope that Novo will be willing to discuss the study design and the impact it had on the results in more detail, the bank writes in the analysis.

In addition, Danske Bank’s analyst also hopes for detailed comments on what Novo will do to avoid losing too much market share to competitor Eli Lilly in 2025, when it seems that the American competitor is ahead in terms of expanding production capacity.

However, there is not much focus from the bank on the financial expectations for 2025, as Novo has already given indications about sales growth, according to Danske Bank.

We do not expect expectations to be a major issue when the company reports, provided we see a top-line forecast that can be interpreted as close to 20 percent, writes Danske Bank.

Novo shares fell 1.7 percent at the opening on Monday to DKK 597.70.

Kova veto Metteltä uhata lopettaa Ozempicin ja Legojen vienti USAan jos Trump yrittää viedä Grönlannin.

Saanko tiedustella onko tullut muutoksia näkemykseen tämän aiemman viestisi jälkeen?

Edelleen GLP-1 analogien ympärillä oleva lääke-pipeline on minusta tosi ruuhkainen,

ja minusta on epätodennäköistä että Novo olisi osunut parhaaseen molekyyliin.

Tämä minusta suurin riski muutaman vuoden aikavälillä.

Lisäksi sivuvaikutukset, kuten nyt tutkittavat harvinaiset haittavaikutukset näkökykyyn, voivat olla molekyylikohtaisia ja tällainen ”musta joutsen” voi viedä lääkkeen pois markkinalta.

Tämä toki harvinaisempaa, mutta yksi esimerkki Vioxx.

Esim tässä yksi nopeasti haettu huonon resoluution kuva tilanteesta:

Lähde, jossa kuva näkyy paremmin.

GLP-1R: Therapeutic Target for Obesity and Metabolic Disorders?

Toki uusilla lääkkeillä jatkuvasti vaikeampaa tulla markkinalle,

mutta lihavuusmarkkinan koko on niin valtava, että myyntilupia haetaan tarvittaessa erilaisista sairauden alaryhmistä ja sitten laajennetaan ylipainon hoitoon.

Näytön saaminen on lisäksi nopeaa, kun lihavuuslääke-tutkimusten kestot ovat kohtalaiset lyhyitä.

(Ja vastuurajauslauseke, en tee kuin hetkittäin suorittavana lääkärinä kliinisiä lääketutkimuksia, joten on oman osaamisen reuna-alueita)

Ja vielä,

minusta ylipäätään lääkeyhtiöiden onnistumisessa on lääkekehityksen luonteesta johtuen niin paljon satunnaisuutta mukana, etten usko Novon onnistuvan pääoman allokaatiossa niin hyvin, että omistama-arvo kasvaisi jatkossakin markkina-arvon vaatimalla tavalla.

Esim. Pfizerin kurssi on nyt taas alempana, kuin vuosituhannen vaiheessa, jolloin Viagra oli muutaman vuoden yhtiön menestyslääke

https://x.com/Th__Nielsen/status/1887033881972310096?s=19

Ennusteista yli ![]()

Katsotaan miten markkina lukee vuoden kasvuohjeistusta, se kai oli jo tiedossa (?)

Novon myynnistä melkein neljännes tulee jo GLP-1 puolelta. Kyllähän tässä riskit kasvaa, että jokin “musta joutsen” lehahtaa paikalle vaikka laajempien haittavaikutusten myötä tms.

Siihen saakka kurssinousut on taattuja, torstaina Eli Lilyn tulos.

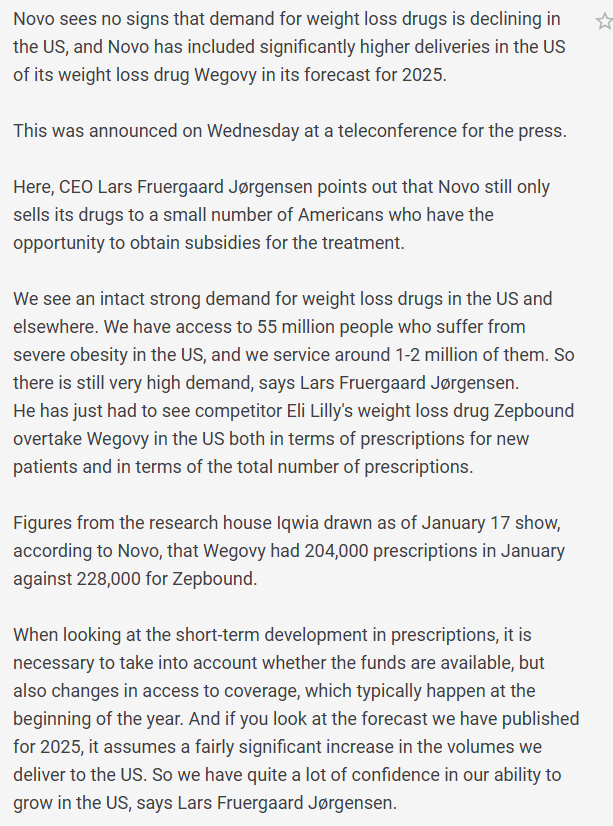

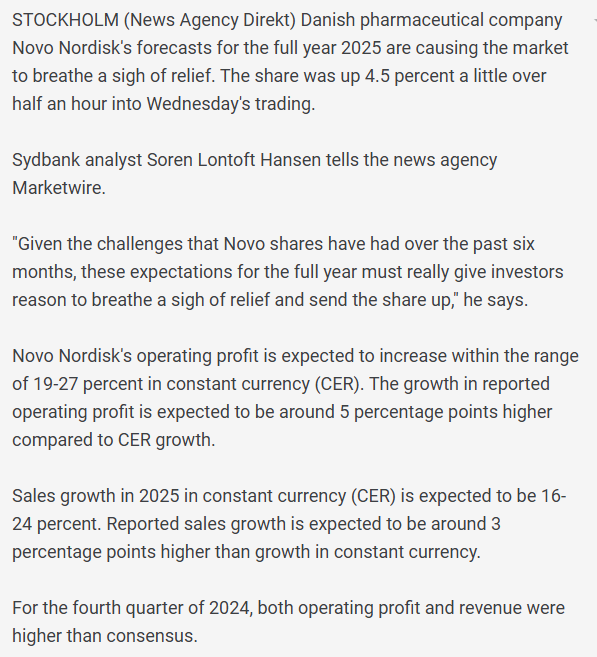

Novo yllätti pääosin markkinoiden odotukset vahvalla tuloksellaan, jonka taustalla oli erityisesti kasvava kysyntä tietysti painonhallintalääkkeelle. Myynti kasvoi merkittävästi ja osakekurssi onkin tätä kirjoittaessa plussalla yli 3 pinnaa, vaikka näkymät ensi vuodelle viittaavat vissiin hieman hitaampaan kasvuun.

Yhtiö pyrkii omien sanojensa mukaan laajentamaan valikoimaansa ja kehittämään parhaillaan suun kautta otettavaa versiota lääkkeestään, joka voisi tarjota kilpailuetua. Novo myös jatkaa uusien yhdistelmätuotteiden testaamista, vaikka tämän yhden keskeisen tutkimuksen tulokset eivät täysin vakuuttaneet markkinoita. Kilpailu alalla kiristyy, mutta yritys luottaa siihen, että tuoteportfolio on laadukas sekä monipuolinen että myös yhtiön ennestään vahva asema pitää vireen positiivisena.

https://x.com/wallstengine/status/1887062434218926259

JP Morgan laskee tavoitehintaa, mutta säilyttää positiivisen suosituksen osakkeelle.

“On Thursday, JPMorgan analysts revised their outlook on Novo Nordisk (NYSE:NVO) stock, reducing the price target to DKK1,000 from DKK1,050. Despite the adjustment, they maintained an Overweight rating on the company’s shares.”

Tässä muita bongauksia tuloksen jälkeen:

Morningstar: TP 640 DKK (600) / HOLD

Jyske Bank: TP: 925 DKK (850) / BUY

DZ Bank: TP 630 DKK (637) / HOLD

Vaan tätä seuraa niin iso joukko lyytikkoja, että katsomalla tänään / maanantaina konensusennusteita näkee jo aika hyvin päivitetyn tilanteen