Greetings @Kasper_Mellas, I was reading Inderes’ brand new Nordea company report. In it, the reduction in OPO’s required rate of return to 9.5% is, in my opinion, very well justified.

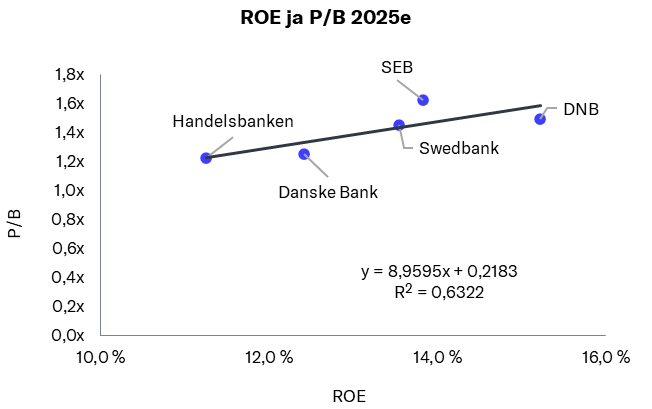

Is there a reason why SEB is missing from the comparable regression model?

It just so happened that the axes of that graph couldn’t keep up with the share price increase. So SEB is included in the calculation, but it was cut out of the image. Here’s the correct version:

Nordea is doing well and there are no problems or storm clouds in sight.

The pricing isn’t bad if PE=10 and dividend 7%, with some share buybacks possibly on top.

But these target price changes unfortunately look a lot like the target price is rising after the stock price.

“We raised our target price to 15.0 euros per share (previously 12.5€) following the results, which is explained by the decreased return requirement”

Stock price rises → target price rises

“Previously, in our valuation, we applied a conservative long-term return on equity expectation of 12–14%, which we have now raised by a notch to 14–15% in line with our forecasts. In addition, we have lowered the discount rate we apply (10.0% → 9.5%), as the increased valuation multiples in the Nordic banking sector indicate that return requirements have decreased across the entire industry.”

Competitors’ stock prices rise → Nordea’s target price rises

In the summer, there was an Inderes video where it was stated that Nordea’s undervaluation had disappeared due to the stock price increase. Now, the stock price increase justifies a higher target price.

I forecast companies’ earnings development 6-8 years ahead. For example, regarding Nordea, my earnings per share forecast for 2031 has risen from the beginning of this year to the present moment from EUR 1.74 to EUR 1.79.

But the expected return has naturally decreased as the share price has risen: At the beginning of this year, with a share price of EUR 10.48, the expected return was 16.5% per annum (by 2031), and now, with a price of EUR 14.04, the expected return is 10.74% per annum (by 2031). The valuation multiple in both cases is P/E 10.

The time horizon for analysts’ target prices is so short and susceptible to changes in market sentiment that they are of no use/help to me.

The new company report forecasts a C/I ratio of 47 percent for the coming years. In the 2022 CMD, the target for the C/I ratio was set at 45-47 percent. Is that ratio chosen for reasons of conservatism (or just to align with the current strategy) or is there an underlying view that Nordea will not improve its cost-to-income ratio in the future.

Above was a quote from OP, which estimated that Nordea would tighten its C/I to 42-44 percent and that the target would be announced at the November CMD.

I would think that in past years, Nordea has had to hire a lot of staff for anti-money laundering supervision. In the future, artificial intelligence could make this work more efficient, potentially reducing staff / outsourced services. In my opinion, artificial intelligence can also bring significant cost savings to large, scalable banks, but system management and maintenance are, of course, not free either.

Out of curiosity, I’d like to ask you how you arrived at an EPS of 1.74-1.79 euros in 2031? I would see that if one looks at comparables, investors might be satisfied with a dividend yield of about 7% on bank shares due to regulatory risk, so if 60% of EPS is distributed as dividends, then DPS would be 1.044-1.074 euros and the share price about 14.91-15.34 euros, which does not promise a very large increase at these prices anymore.

This has likely taken into account that Nordea buys back and cancels its own shares at a rate of approximately 80 million shares per year. In five or six years, the number of shares will thus decrease from the current 3450 million to approximately 3000 million shares.

EPS and DPS will thus grow every year even if the earnings remain constant.

Fortunately, it is not the banks’ job to investigate crimes, but their responsibility is the screening of suspicious financial transactions. Hopefully, new technologies will bring efficiency and savings to this screening.

Revenue growth 2.5%, cost growth 2%, and the number of shares at the end of 2031 is 3056 million shares. Share buybacks reduce the number of shares by 2% per year.

I had a notification in Nordea’s online bank stating that the Nordea Investor program is old and has reached the end of its lifecycle, and it will be discontinued at the beginning of December.

The notification stated that from then on, stock trades should be made in Nordea’s online bank or with the mobile application.

What are people’s thoughts on this? I’ve personally enjoyed making stock trades using Investor. I particularly liked this bid level indicator which shows quantities and prices in real-time. I didn’t find such a feature in the online or mobile bank.

I haven’t even remembered the investor exists, so it doesn’t bother me. Hopefully, they’ll put their development efforts into mobile development and make it more usable. Of course, I have monthly savings in funds and occasionally 4-8 direct shares, so I’m fine with the current one.

I will definitely miss Investor. I think it’s better than the one currently in Nordea’s app. Investor’s strength is its clear structure and that all essential information can be seen at once. Or maybe I’m just used to using it. Many, I recall, criticized Investor, but since I don’t know of a better platform, it has been good enough for me. I’ll probably get used to the new platform too, once I’m forced to start using it I’ve been so satisfied with Nordea’s services that I don’t even bother thinking about switching brokers.

From Nordea’s perspective, it’s obviously foolish to maintain, develop and support two different platforms to do the same thing, so in that sense, it’s a very sensible decision. Provided that the remaining part doesn’t get stuck in the current state and doesn’t receive development funding. I understood that it has shortcomings. (I myself only occasionally buy one ETF there, for which it is quite suitable even with its minor shortcomings.)

Yes, that offer level meter is also on mobile, and I believe it’s in online banking too. I don’t remember now where you could see it in Investor; on mobile, it shows when you are placing an order. I’ve gotten my annual reports from Investor; now I have to hope that similar reports will be available from online banking in the future.

Jyske Bank has raised Nordea’s target price in DKK from 105 to 115 (approx. 15.4 EUR). Marketwire’s news article, run through Google Translate:

"Jyske Bank analysts have raised Nordea’s target price from DKK 105 to DKK 115.

This comes ahead of Nordea’s third-quarter financial statement, to be published on October 16.

In the financial statement, Jyske Bank expects Nordea’s revenue to have decreased moderately by 4.6 percent.

According to Jyske Bank, this is expected to be due to a decrease in net interest income in light of continuously falling key interest rates in the Nordics, a decrease in trading income (after a strong third quarter in 2024), and stable development in commission income, which is typically seasonally lower in the third quarter.

Nordea also has a significant event planned: the bank’s Capital Markets Day on November 5.

We expect Nordea’s cost efficiency to be a key issue, and a credible outlook for improvement in this regard would act as a catalyst for the share. We maintain our buy recommendation and raise the target price to DKK 115 per share until the earnings report, Jyske Bank writes."

Target price adjustments upwards continue, Norwegian “finanshus” (financial house) ABG Sundal Collier raises DKK 106.68 → 112.33 (approx. EUR 15.04) and reiterates its buy recommendation. (MarketWire/Nordnet today at 8 am.)

edit: let’s add this that just appeared on Nordnet:

“Arctic Securities raises its target price for Nordea to SEK 165 from SEK 152. The buy recommendation is reiterated.” i.e., 152 → 165 SEK (approx. EUR 14.96), reiterates its buy recommendation.

edit2: Jyske Bank has apparently issued a positive earnings warning today, which is also lifting other banks. In a news agency Direkt report conveyed by Nordnet this morning: “Jyske Bank’s full-year profit forecast increase on Friday not only lifts its own share, which rises over 4 percent on the Copenhagen Stock Exchange, but also pulls along Danske Bank and Sydbank, both of which are trading up about 2 percent. Nordea, which operates in Denmark, also climbs 1 percent.”

The praises continue as well. Handelsbanken has analyzed the Nordic banks: it states that three of them are worth buying and raises one of them as a favorite.

The first two mentioned are Danske and Swedbank, and the best one is Nordea. More could be gained from Nordea, especially through cost savings.