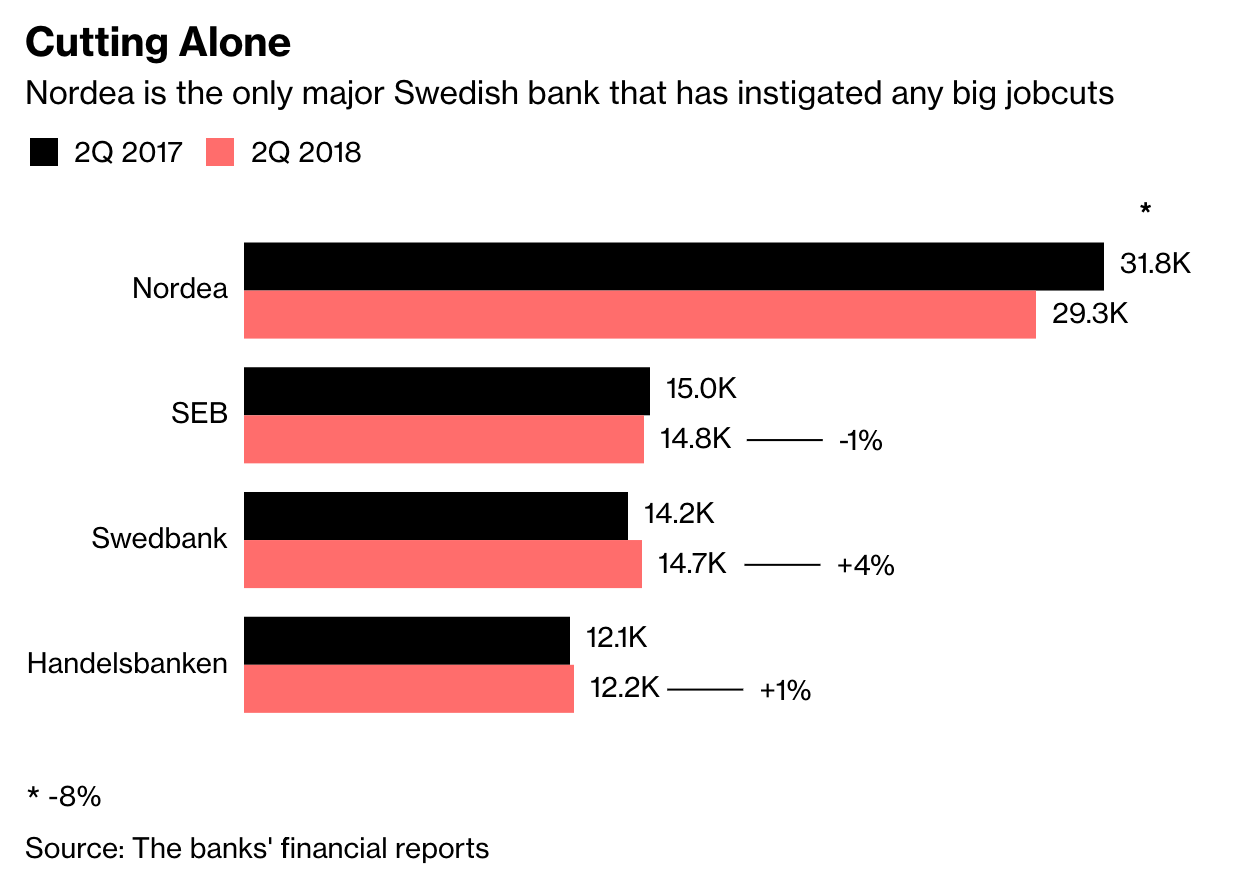

Nordea on ainoa pohjoismainen pankki, joka leikkaa työvoimaansa rajusti. Mielenkiintoinen erottuminen joukosta muiden suurten Nordic-verrokkien kanssa: samaan aikaan Handelsbanken ei aio leikata, ja panostaa edelleen desentraloituun malliinsa (joka historiallisesti on toiminut parhaiten) ja SEB:llä on päällä oikea rekryrynnäkkö.

Nordean tie vaikuttaa oikealta, mutta onko “sitruunan puristaminen” ja loputon leikkaaminen oikea tie? Minkälainen lienee työntekijöiden intohimo saada aikaan loistavia asiakaskokemuksia, samalla kun on selvää että oma työ automatisoidaan heti kun mahdollista?

Vaikea sanoa, pankeilla on fundamentaalisia kysymyksiä edessä oman olemassaolonsa tarkoituksesta ja minkälainen rooli niillä on yhteiskunnassa ja kuluttajien silmissä jatkossa.

Huomenna Sampo julkaisee Q2’18 tuloksensa. Itse tulos tuo tuskin yllätyksiä, mutta mielenkiintoista odottaa Stadighin kommentteja markkinasta ja Nordeasta.

Kaksikko on videon kriittisen alun jälkeen melko luottavaisia Nordean tulevaisuuteen ja kohtuulliseen tuotto-odotukseen.

Sijoittaja voi tietysti aina omalla kohdallaan miettiä, että haluaako salkkuun Nordean tarjoamaa korkeaa osinkotuottoa ja mahdollista pay offia jos/kun it-prokkis saadaan loppuun. Samalla tulee kantaneeksi riskiä, jos Nordea ei onnistukaan asemoitumaan oikein muuttuvassa maailmassa. Pankit ovat myös hyvin alttiita makrotalouden heilahtelulle ja jos sitä riskiä haluaa vähentää salkussa, on pankkien poisjättäminen melko loogista.

Heikkilä & Vilén nostavat paljon hyviä pointteja videolla. Tuntuu että pörssissä tosiaan on yhtiöitä joissa nähdään riskejä ja sitten toisaalta yhtiöitä joissa ei nähdä riskejä ja jotka arvostetaan P/E 20-40 kertoimilla. Finanssimarkkinanoviisina pohdin että laskeva lainakanta vähentää operationaalisia riskejä. Jos korkokate on matala, talouden shokit ja esim. Ruotsin asuntojen hintojen lasku on tuhoisampi asia pankeille. Nordea on pärjännyt hämmentävän hyvin lisäämällä varainhoidon fokusta ja keskittymällä kulupuolen säästöihin. Strategia on juuri oikea riskitietoisen sijoittajan kannalta.

Pohjoismaiden suurinta finanssikonsernia treidataan tasearvolla. Kuinka vähäinen luotto markkinoilla on konsernin johtoon? Ei kai tähän asemaan nyt sattumalta ole päästy?

Minä kyllä haluaisin jonkun vääntävän rautalangasta että mikä tämä “tulevaisuuden finanssimaailma” oikein on. Jotkut pikavippaajat mainostavat olevansa vaihtoehto pankille. Nämä subprime-lainat aloittivat viime kerrallakin finanssikriisin. Regulaatio nähdään uhkana, mutta se varmasti suosii vakavaraisia toimijoita. PSD2:sen muutokset ovat mielettömiä: eikö nyt olisi mahtavaa jos Google ym. tietää kaiken muun lisäksi myös tilisi saldon ja kulutuskäyttäytymisesi ja auliisti levittäisi näitä yhteistyökumppaneilleen palvelun parantamiseksi? Ehkä haluan pitää nämä asiat vain minun ja pankkini välisenä.

Olen myös pihalla näistä IT-järjestelmistä. Käyttöliittymä on tietokoneissa se osa jonka haluaisin viimeisenä vaihtaa. Turvallinen, suorituskykyinen, luotettava ja selkeä käyttöjärjestelmä on paras. Kaikenlainen kilkattimien over-engineering heikentää kaikkia neljää. Kymmenen vuoden takainen plaintextiä sisältävä webbisivu on paljon miellyttävämpi käyttää kuin esim. nämä nykyiset uutispalvelut.

Olen itse osittain PSD2 kanssa tekemisissä työn puolesta. Se on yks iso vitsi. Käytännössä rajapinnat on ollu aina auki. Kukaan ei vaan ole määritellyt yhtä stardardia eikä PSD2 määrittele myöskään vaikka pitäisi… Käytännössä PSD2 ei muuta mitään siis. Pankki-integraatiot on edelleen vaikeita tehä eikä yhtä tapaa ole joten globaalia integraatiota edelleen vaikea tehä. Pankit oikeastaan toivookin tätä että PSD2 feilaa, eikä yhtä stardardia tule ikinä, jolloin Google ja Facebook ei pääse heidän markkinalle.

IT-uudistuksen höydyt tulee erityisesti kuluttajapuolelle kustannussäästöinä ja sen pitäisi parantaa kuluttajapuolen tuottavuutta. Juuri ennen kuin it-uudistuksen pitäisi valmistua, vaihtaa kuluttajapuolen ylin pomo Finnairiin. Onko sellaista skenaariota olemassa, jossa it-uudistus onnistuu ja Topi Manner vaihtaa Finnairiin? Itse en usko.

Hyvää pohdintaa. On kieltämättä kauhistuttava ajatus, että hanke epäonnistuu ja tämän vuoksi Nordeassa on käynnissä johtajapako. Uskoakseni Finnairin toimarin tehtävä on palkkaukseltaan ja muilta eduiltaan kuitenkin sen verran houkutteleva, että siihen on varmasti tunkua muutenkin.

Edit: korjattu automaattisen tekstin korjauksen tekstejä

Pankit on kieltämättä yleensä etulinjassa sijoittajien dumppaus-listoilla, koska ne ovat niin vahvasti kiinni verkottuneessa globaalissa finanssijärjestelmässä. Pankit vihaa epävarmuutta. Pitkäjänteinen sijoittaja voi tietysti nähdä ne tankkauspaikkoina, jos vain luottaa pankin riskienhallintaan joka testataan heikompina aikoina.

First North yhtiöt on melko epälikvidejä, voi tulla rajuja muutoksia suuntaan ja toiseen jos yksityissijoittajien kantti pettää. Fundasijoittaja hieroo käsiään.

Sotketaanpa ketjua hieman Revolutin casella (https://yle.fi/uutiset/3-10397197)! Peruspankkipalvelut ei tietenkään itsessään ole mikään kultakaivos, mutta kuluttajien näkökulmasta nämä asettaa mukavaa painetta. Kai tätä voisi luonnehtia kokonaisuudessaan yhdeksi stepiksi kohti AUMeja, joista on ainakin toistaiseksi saatu pidettyä uudet toimijat melko etäällä…

“Lähiaikoina Revolut lanseeraa ainakin Britanniassa pörssialustan, jolla voi käydä osakekauppaa ilman välityskuluja. Toistaiseksi yhtiön kortti toimii vain maksukorttina, mutta suunnitelmissa on myös luottojen tarjoaminen.”

Kevyesti artikkelissa sivuttiinkin, eli tottakai Revolutin kaltaisille toimijoille (joita löytyy iso liuta all in all) on jo tutut isot pajat hengittämässä taustalla (Facebook to Banks: Give Us Your Data, We’ll Give You Our Users - WSJ). Ja yksi käännekohta tulee varmasti olemaan, kun pankkipalveluita aletaan viemään Sirin, Google Assistantin, Alexan jne. tasolle

Sinne vaan tarjoamaan yhteistyötä. Revolutin käyttäjille Inderesin premium käyttöoikeudet olis sitten täydellinen palvelu ja parantaa Suomen kansankapitalismia.