Nokian Brewery announced on February 18, 2025, its aim to list on First North.

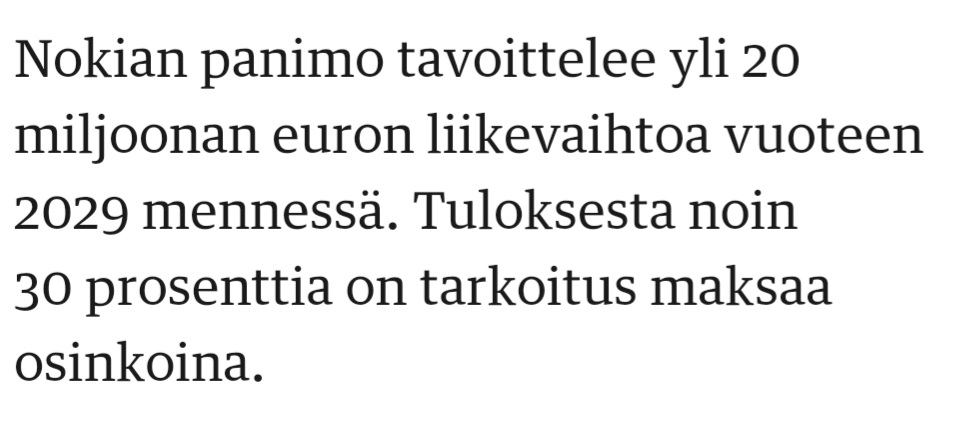

The target is >20 MEUR revenue by 2029.

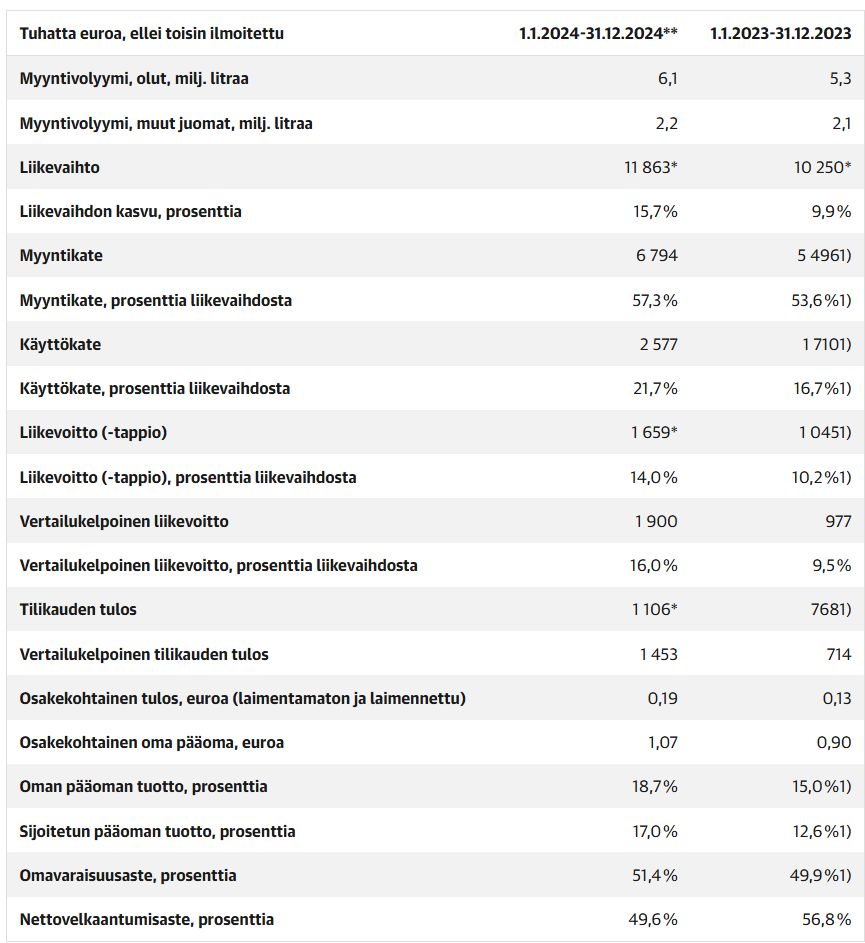

2024 saw just under 12 MEUR, which brought 1.9 MEUR in comparable revenue.

Janne Paavola, CEO of the Company, commented:

”Nokian Brewery is Finland’s second-largest microbrewery by revenue and the fifth-largest brewery overall, and I am particularly pleased that we can announce today our plan to list on Nasdaq Helsinki’s First North Growth Market. We have systematically grown Nokian Brewery organically and profitably, in line with our values, relying on domestic origin and responsibility. The IPO and listing would accelerate the implementation of our growth strategy and our growth investments. Our goal is to even better fulfill our mission of making thirst a pleasure.”

Nokian Brewery aims to achieve a revenue of over 20 million euros by 2029. In addition, the Company targets an annual EBITDA margin of over 18 percent during the strategy period 2025–2029. The Company’s revenue and EBITDA margin targets are primarily based on strategic pillars, namely consumer satisfaction, customer satisfaction, employee satisfaction, and cost-effectiveness.

Nokian Brewery expects its 2025 financial year revenue to grow from the previous year (2024: 11.9 million euros) and its EBITDA margin to be 18–21 percent (2024: 22 percent).

Nokian Brewery has grown strongly, supported by organic growth. As part of its organic growth strategy, the Company has started the construction of a new logistics center, which is scheduled for completion in May 2025. This investment is the largest in the Company’s history, and the total estimated cost of the project is over four million euros. Once completed, the new logistics center will be approximately twice the size of the previous one, and its purpose is to streamline the management of goods flows, such as raw materials and finished products, improve delivery reliability, and reduce logistics costs. The size of previous storage facilities has limited production capacity, and with the additional space, the Company can better prepare for the demand for seasonal products, for example. With the new logistics center, the current storage facilities will be freed up for production use in the future, enabling investments in new equipment and increasing production capacity. The Company plans investments aimed at production capacity and efficiency, responsibility and energy efficiency, as well as other production-related matters supporting competitiveness. Nokian Brewery’s medium-term investment plan, valued at approximately 10 million euros, would enable a production capacity of over 12 million liters of beer while minimizing environmental impacts. This medium-term investment plan includes the ongoing construction project of the logistics center, valued at over 4 million euros.

And if someone doesn’t know the company otherwise, at least from its history, when pleasure was turned into thirst. At that time, however, the operation still took place under the name Pirkanmaan Uusi Panimo:

And around the same time, Matti Nykänen had his own cider.

I’m stopping by Nokia today to interview the company’s management for InderesTV, and if any questions arise at this stage, you can write them in the thread – I’ll try to include as many as possible.

The press conference, by the way, starts at 11 AM and can also be watched via InderesTV.

Interesting, perhaps this should be compared to Marimekko, which also, being banker-driven, started to grow tremendously. Yes, I will also attend the annual general meeting.

After going public, do they still identify as a microbrewery, or do they brand themselves as one of the “big players”? Do they feel that the current number of breweries in Finland (approx. 120) is on a healthy foundation, and is it out of the question for their growth to make acquisitions? Additionally, I’m interested in their current facilities. Is there enough space for growth?

@Opa probably didn’t notice that a thread had already been made for this. No worries. I deleted that other thread because the discussion has started well here

Question: Are hard seltzers coming from Nokian Brewery? Olvi’s annual report mentioned that, regarding product categories, the sales of waters and hard seltzers developed best.

Here’s the promised interview from the brewery on site.

Topics:

00:00 Introduction

01:18 Why are you listing – why go public?

02:26 Identity going forward: microbrewery or not?

03:27 Share of non-alcoholic beverages in sales

03:50 Keisari and other brands

04:41 Nokian Panimo in relation to other microbreweries

05:21 Competitive factors/advantages

06:15 Financial development and key growth drivers

08:30 Investments needed – capacity is a bottleneck

10:27 Growth targets – focus on organic growth in Finland

11:50 Profitability targets – “Good numbers already for this industry”

12:35 Market trends – “Finland is a beer country”

14:00 EU’s new packaging and packaging waste regulation

14:57 What’s next?

So if the categories are beer and others, then the “Others” category would make up about ~30%. There seem to be 5 alcoholic products in that category (3 cocktails, 2 ciders). Would non-alcoholic then be approx. ~25%? Beer volumes are decreasing by 2-3% per year. The volumes of the ‘Others’ category are probably not declining. Of course, if the company’s market share is 2%, there is indeed plenty of room for growth. EBITDA will be under pressure in the coming years due to all investments, especially if that EU packaging waste regulation indeed comes into force.

Well, well. We’re ending up in a situation where from the household garage, it’s a few hundred meters to a publicly traded tire company, and from the sauna, a few hundred meters to another publicly traded company that produces sauna drinks.

Otherwise, I wouldn’t necessarily be enthusiastic, but I guess due to local patriotism and maintaining interest in a local company, I’ll have to take a slice of this Nokia-based company too.

After all, we’ve already picked up several pallets of sauna refreshments from the factory store and listened to bands on the factory’s terrace.

When I started investing, my very first investments were unlisted shares of Nokian Panimo (Nokia Brewery) (what was that site again through which you could still trade them ). I’m looking forward to the listing; at least I’ve been following the company’s operations from the sidelines anyway, and the direction has only been for the better

I noted that Olvi’s EV/EBITDA is about 6x with 5% growth. At its best, it has been 12x, and growth has ranged between 1-20% over the last 8 years.

If Nokian Panimo’s financial targets are met, its revenue in 2029 would be >€20m (11% annual growth) and EBITDA margin 18%. An EV/EBITDA of 8x would result in an enterprise value of €28.8m, and with a 15% required rate of return, the acceptable enterprise value at the IPO in 2025 should be ≤ €14.3m. Growth over the last 5 years has averaged 15%, so that 11% could be achievable. At what enterprise value would you be willing to participate in the offering?

There’s an article in Kauppalehti about the listing. The article covers the same topics already discussed in the thread and video, and a Kauppalehti analyst has estimated the current market value.

The article is behind a paywall, below is a short summary:

\u003e Kauppalehti analyst Ari Rajala has estimated Nokian Panimo’s potential market value by seeking comparisons from, among others, Olvi, Anora, the stock exchange’s food sector, and an average listed company.

Based on this and Nokian Panimo’s 2024 figures, the company’s market value could be around 14–19 million euros before the IPO. The value of the IPO will therefore be added on top of that sum, and the company has not yet disclosed it.

Interesting news. However, the dividend policy below grates on my ears a bit.

Money is being raised for growth, and dividends are planned to be paid at 30% of earnings. I don’t understand the logic. No dividends should be paid at all, but full throttle into growth

It is mentioned that the biggest investment in history is underway for a logistics center. Surely, a good amount of loans will be taken out, so forget those damn dividends.