The development of Nokia Brewery’s new soft drink products has left me a bit confused. My own subjective experience has been that the strength of the company’s sodas has been a certain “natural” impression, or perhaps better put, an illusion of naturalness, considering we are talking about artificial sugary drinks after all. Especially the Vanilla Cola, Cloudy Lemon, and Hometown Lemon have stood out positively to me compared to competitors’ products because of that illusion. And it is specifically for this reason that Nokia’s sodas often end up in my shopping cart.

I was actually quite excited when I noticed they had launched new pear and pineapple sodas, but in the end, I was deeply disappointed. The impression was very artificial and essence-like, whereas my expectation was that these flavors could very well be fresh and full-bodied, somewhat juice-like and natural-seeming… something like competitors’ products, e.g., San Pellegrino’s lemon and blood orange sodas. The fairly recent Nokia Blueberry soda succeeded reasonably well in this, but in my opinion, it doesn’t quite reach the level of the earlier ones either. These pear and pineapple novelties certainly won’t get a second chance from me.

Well, this non-alcoholic side is, of course, a bit of a subplot in the overall picture of the investment case, but I’m still reflecting on this development direction that surprised me. What kind of opinions do others have about these new sodas?

I should test the new beers to see if they’ve hit my taste buds better on that side. As an investment, the company has been on my mind a lot, but I haven’t yet managed to convince myself to hit the buy button.

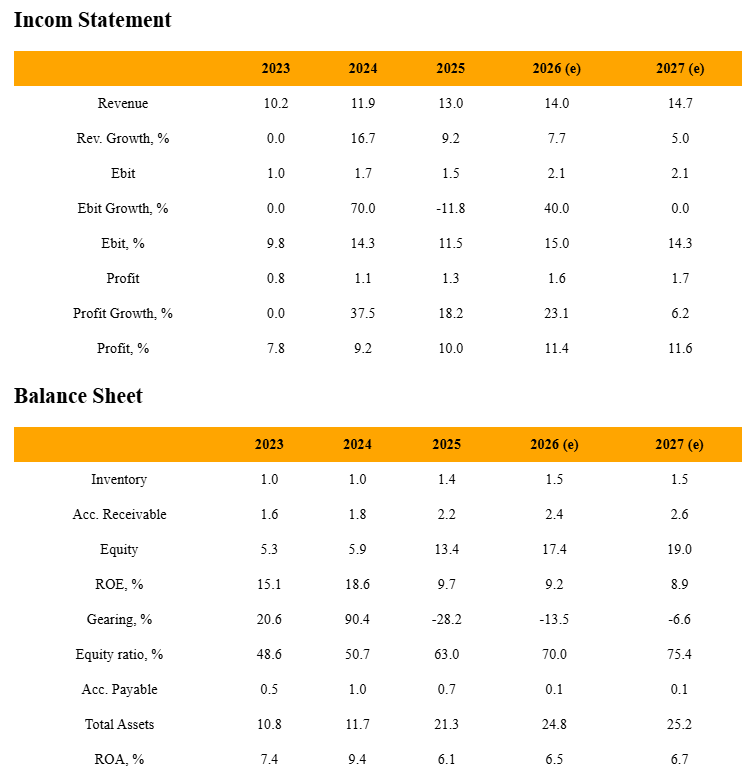

Evli’s forecasts seem to have been exceeded across the board. And earnings per share was 3 cents above Evli’s forecast. It was decided that those 3 cents would be distributed as a dividend, even though Evli predicted a zero dividend.

For the current year, Evli predicts revenue growth of about 10% and an EBITDA margin of over 18%. Nokian Panimo’s new guidance is: “Nokian Panimo expects revenue for the 2026 financial year to grow from the previous year (2025: 12.98 million euros) and the EBITDA margin to be 17–20% (2025: 17.4%).”

H2 went quite well in my opinion. In the guidance, 18–20 would have looked nicer. Of the other observations, the most essential is the strong growth rate of the “other drinks” segment. On an annual level, there was a jump from 2.2 million liters to 2.9 million liters.

I can offer a somewhat contrary opinion on this. My own purchases of Nokian Panimo sodas have increased with these new products. Part of it is certainly that I’ve started boycotting American sodas and buying domestic alternatives instead. Both my wife and I thought the pear and pineapple flavors were good and fit the selection well, even though Hartwall already offers both flavors.

One thing I have also noticed specifically regarding the sodas at my local Prisma is the new small Nokian Panimo refrigerated displays next to the checkouts. It’s a good spot for impulse buys, especially since the visual branding of the products is effective. I wonder if similar setups have appeared elsewhere in Pirkanmaa.

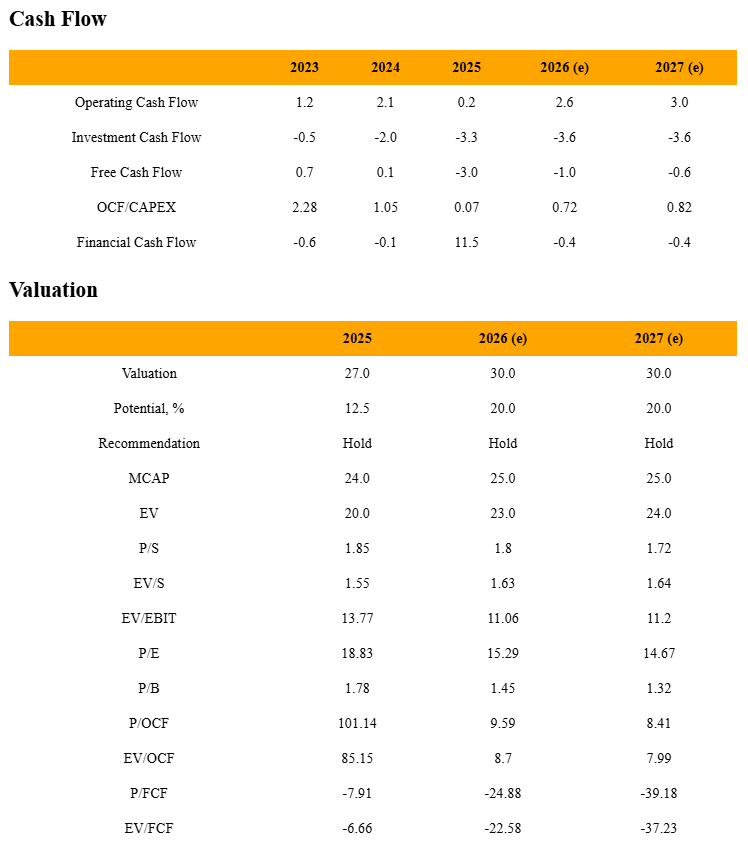

Nokian Panimo’s progress looks good in terms of the numbers. The AI valuation for the stock came out to 30 million. There is an upside of approx. +20% relative to the current share price, and the recommendation narrowly remains on the Hold side.