It’s good that someone sees the positive in Nokia; they still delivered a better result than expected.

7 Likes

Alright, the call started getting to the point as well. Almost everyone is asking only about optical and IP networks—the mobile side has been left almost entirely in the background, and that’s a good thing.

Now Hotard mentions “scale-across” as a big opportunity, and said that Infinera’s factories in the US are very essential, highlighting InP, PIC, and vertical integration. This is exactly what has been highlighted regarding CPO (co-packaged optics) and also in connection with Nvidia’s Rubin platform. This Nvidia theory was certainly reinforced now—let’s see if it’s understood yet—of course, there was no confirmation regarding Nvidia, but someone is going to want those products. However, Hotard said that the larger US capacity will be fully utilized in 2027 (I personally thought it would already be fully utilized this year).

I’ll return to this once the transcript is available. Here is my own excerpt, which may contain minor errors.

Question (DNB Carnegie): I just had a question on the invest in the capex. It’s quite a big step up, and I’m just wondering if it’s all about increasing your capacity, how much would you say that of your capacity is already utilized? So, are you working at full capacity, or how should we think about kind of ramping up production and how you plan from that, you know?

Answer (Hotard): . Thanks for the question. If you think about, you know what we’ve shared? So far, we have an existing Fab in California. Where we’ve been investing and bringing a new Fab online. This is some of the initiative started before we acquired them and we’re continuing to invest, and this was also the place where we got partial funding in the CHIPS Act from the US government; that Indium Phosphide Fab is the one.

The next one is the one we expect to come online later this year. What I would say is that, you know, we’re certainly, well on track to consume capacity in the existing one, and we absolutely need the new Fab that comes online to support the demand that we’re seeing and to meet our forecast. So, or longer-term forecasts, because obviously, as it comes on later this year**, it won’t contribute as much to production this year**.

This is also critical for us, because at the core of our capability and our differentiation is our photonic integrated circuit. It’s one of the key elements of the components of these photonic systems, and it’s a place where we believe we have differentiation in the product itself.

So, what we can do, and what’s a little bit different than when you think about a traditional semiconductor Fab, or the higher volume silicon fabs—you know, you might consider in computational silicon or memory or others—is that our capital investment size tends to be much smaller to add additional capacity, and that’s really just the nature of optical technology and also the nature of Indium Phosphides.

So, hopefully that gives you a couple dimensions to think about, but I would think about the investments we’re making really in that new Fab supporting '27 demand. Starting to ramp during '27, it’ll have some reduction this year, but mostly in '27. And then think about the ability to add capacity in that Fab or in others as being much smaller chunks.

By the way, Hotard used pretty much the same terms as Nvidia…

Previously, I had heard “scale up” being used more often…

21 Likes

So this is what it’s all about, and it likely went unnoticed by many.

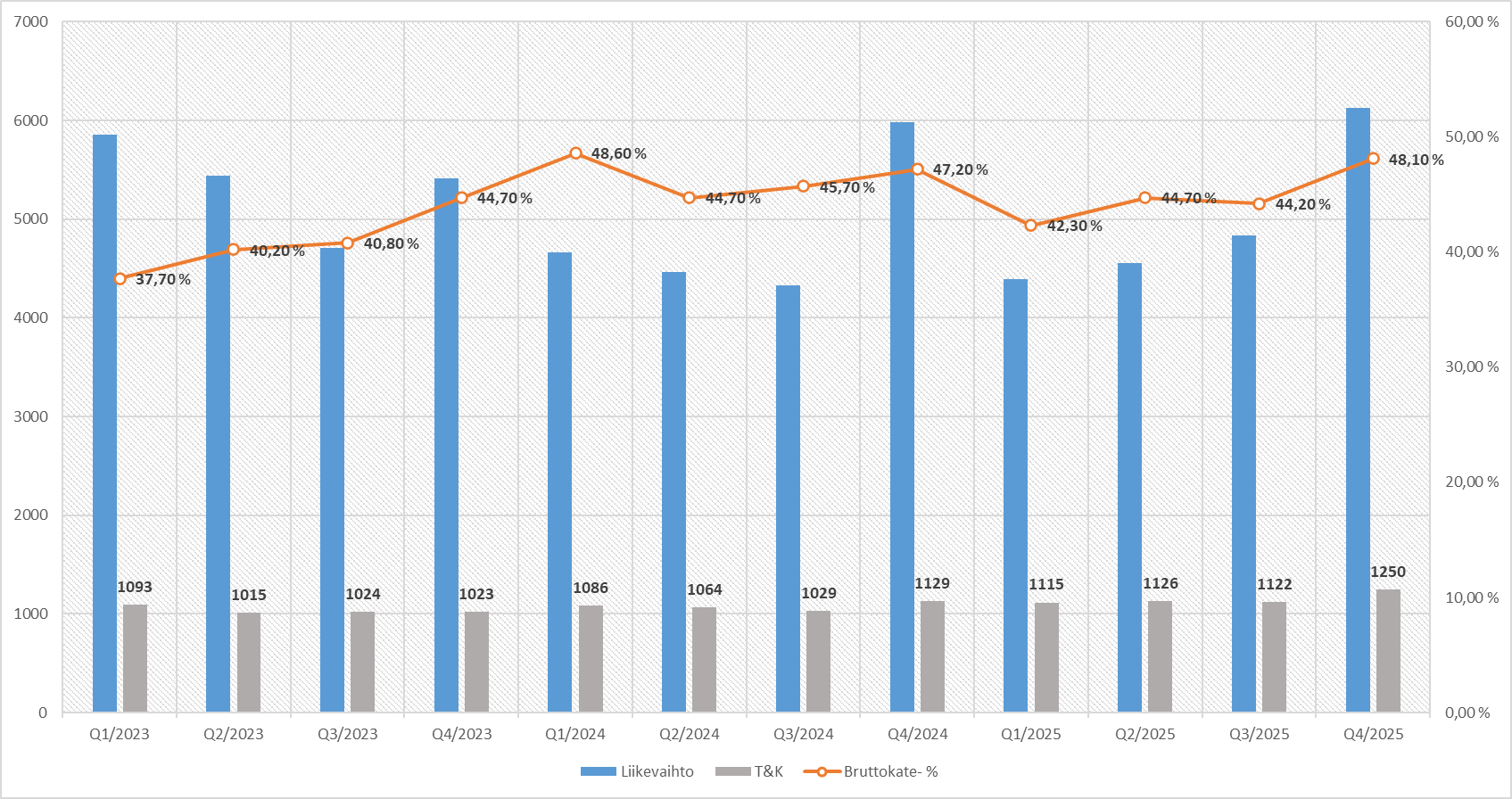

Q4/2025 R&D expenses were increased by more than €100M compared to before. And at the same time, without significant one-off items (such as retroactive patent income), the gross margin % was at a top level. At this rate, all of this will flow through to the bottom line even more significantly.

40 Likes

“Admittedly, Hotard said that the larger US capacity will be fully utilized in 2027”

Infinera has its own factory investments of ~200-270M and they should be completed this year. In November, Nokia decided on a 4 billion currency unit investment in the United States, of which ~500M goes to production infrastructure and the rest to R&D, so perhaps by 2027 there will be ~700M worth of new Nokia factory capacity in the U.S. At least “made in america” won’t be an obstacle anymore, hopefully. Hotard is likely referring to Infinera’s factory currently under construction, and maybe it relates to those pluggables.

AI claimed that the Rubin ecosystem has already been decided, but as per my habit, I hope that I am (it is) wrong. Rubin is supposed to hit the market this year, and I find it hard to believe that Nvidia would want to leave anything to the last minute. More likely, the entire ecosystem has already been decided and established through collaboration during the development phase.

Hmm, so Infinera has one factory that was completed earlier and another that was completed at the end of last year. It came as a surprise that the production ramp-up takes such a long time.

This relates to pluggables because Nokia also needs components for its own products. But looking ahead, it relates to ICE-D components and InP capacity.

Of course, the Rubin infrastructure is already locked in. Even the product has been introduced without detailed specifications.

So Nokia (Infinera) is already making those components, but the new factory will increase capacity tenfold. It’s also worth reading Nokia’s own materials instead of just relying on AI answers.

12 Likes

$550M tied up in the California+Pennsylvania factories, and in 2024 it was estimated that they would be completed in summer 2026. Usually, those aren’t finished ahead of schedule, at least!

It remains to be seen what Nokia’s $4bn investment in the US in November will yield and what it all entails. Infinera’s price was only ~$2.3bn. Part of the ~$500M production financing is going to Pennsylvania, like Infinera’s new factory, so hopefully there won’t be any surprise bills coming from there, but rather production expansion. ![]()

4 Likes

Results commentary on Yle / Danske’s Sarkamies and OP’s Stenvall, plus Justiina through some channel.

At least a weak Q1, growth in infra weaker than competitors.

Earnings performance in the network segment isn’t really valued when it’s not growing, and in the growth segment, i.e., infra, Q4 was flat.

4 Likes

Does the forum think it’s time to start buying Nokia now, and is anyone buying?

I don’t know if it’s time to buy, but it was a classic case again with the earnings report – clearly, it drops more often than not and there’s always something to get caught on. Hope is also always firmly in the future. This certainly isn’t any multibagger.

If you’re planning to buy for a long-term portfolio, there’s no need to rush. It will likely drop further from here as target prices are revised downwards.

1 Like

This is the same old excuse-making that I can’t even be bothered to read anymore; they’re always looking for something to complain about.

2 Likes

I’m annoyed with myself for adding more fuel to the fire during the Jan 21st dip, and now I don’t have the cash to buy “on the cheap”. To me, €5.5/share isn’t a question but an investment decision, but you should still follow your own gut and not take this as investment advice. I’m in it for the long haul, and even though the estimate for 2028 only implies about 15% annual earnings growth, I remain optimistic, as new products and potential expansions into new markets aren’t easily factored into future operating profit projections. Time will tell.

Additionally, if I recall correctly, Mobile is on ice and earnings growth relies on Networks. I look forward to seeing how Mobile performs from 2028 onwards as 6G begins to approach. At the moment, it’s mostly dragging down the share price. Only the future will show what becomes of it.

2 Likes

These buy/sell recommendations could be cleaned out. It’s been done before. Everyone should draw their own conclusions.

4 Likes

I somehow get the feeling that ever since the Nvidia news last autumn, people have just been expecting news related to that partnership from Nokia at every possible opportunity, and if it doesn’t come or isn’t promising enough, the stock drops significantly into the red. I’m almost tempted to opportunistically open a position myself and hold it until the market sees some +10% quick rally on the back of some more significant Nvidia news.

3 Likes

Many people likely also value the growth of the network side. Personally, I’m more interested in that than the Nvidia collaboration, the potential benefits of which are far in the future. Of course, this is partly linked to whether Nokia can gain better traction as Nvidia’s “little brother”. I believe they have enough muscle on their own, and the Nvidia collaboration represents only potential positive surprises on top of the current good outlook.

I personally don’t understand why the market reaction was so drastic even before the results were released. Perhaps the market had higher expectations than I did, as I’m looking 5+ years ahead rather than just at the next year, and to my eye, everything seems to be going as it should.

1 Like

I wouldn’t be so sure. I find it more likely that the aim would be to stay in an uptrend on a monthly level, meaning the benchmark for the Helsinki Stock Exchange would be €5.146 and $6.05 in USD. Of course, the US listing would have more room to fall – and it is likely the dominant one.

If the previous lows @ $5.86 and €5.072 are broken, it can be stated that the previous uptrend wave is already complete… and now it would be time for the 5th wave.

In any case, the consensus for target prices is @ €6.022 – and I personally don’t believe it will drop much from there. Nokia was bullish enough in the conference call regarding the outlook for the coming years, so it takes quite a lot for an analyst to bet against that. And of course, currently 21/33 analysts are of the opinion to add or buy.

Let’s see how it goes.

11 Likes

3 Likes

Here is more reasoning from the Jefferies research firm.

Nokia might be guiding somewhat conservatively due to execution risks associated with meeting strong optical demand, Jefferies analysts write. The Finnish telecom-equipment provider is guiding for 2026 operating profit at between 2 billion and 2.5 billion euros, versus consensus at 2.3 billion euros. “We continue to expect Nokia’s strong optical and IP networks momentum and steady mobile networks performance to re-rate the stock.” Fourth-quarter sales were in line, but gross margin at 48% was well ahead of consensus at 45%, the bank says. Order intake was strong across both optical and IP networks, supported by AI and cloud demand. Mobile networks outperformed expectations on both revenue and margin, reinforcing signs of stabilization, it adds. Shares fall 4.2%.

10 Likes

If the European Union’s toolbox comes into effect, then for example, if I remember correctly, Vodafone/Three announced that Huawei will continue as a supplier in Europe unless it is banned.

Can anyone estimate how much market share Nokia could win on the continent?

If I recall correctly, Nokia clearly gained market share in the UK.

https://www.nokia.com/newsroom/nokia-wins-significant-5g-deal-with-vodafonethree/

4 Likes

Translation highlights and summaries (aided by AI) of analyst questions and answers.

Question (Goldman Sachs):

Optical grew about 20% in the quarter, but the full-year 2026 guidance is only 10–12%. Is this caution, given that order momentum and the AI share are strong?Answer (Justin Hotard):

Optical grew 17% in Q4. The 10–12% guidance covers the IP and Optical businesses combined. The baseline is still telco-heavy (about 70/30). Nokia is building growth from this base and scaling production. The guidance reflects discipline and predictability, not a view of weak demand.Question (Arete):

CapEx is rising to €900 million – €1 billion. Is this based on orders already visible, or will it require new wins from hyperscalers?Answer (Justin Hotard):

CapEx investments in optical and semiconductor manufacturing are based on long-term market trends. Returns are not realized within a single year. Investment decisions rely on long-term confidence in the market and visible demand.Question (Raymond James):

What is Nokia’s position in Scale-Across projects and how is the market evolving?Answer (Justin Hotard):

Scale-Across is seen as part of the long-term optical demand. The market is undergoing a transition from 400G to 800G, and in the future, 1.6T and 3.2T. Scale-Across supports these transitions. Routing benefits from this development, and Nokia is working closely with customers to scale production.Question (SEB):

Are there any supply issues limiting optical growth?Answer (Justin Hotard):

There have been constant bottlenecks in AI infrastructure (power, compute, memory, connectivity). There are also constraints in optics, which is typical at this scale. Nokia is investing in both its own capacity and the ecosystem.Question (DNB Carnegie):

Is capacity already fully utilized and how aggressively is Nokia investing?Answer (Justin Hotard):

Nokia has an existing InP fab in California and a new fab coming online later this year. The new capacity will mainly support demand in 2027. InP and photonic integrated circuits (PIC) are at the core of Nokia’s technology. Increasing capacity in optics is a smaller investment than in the traditional semiconductor industry.Question (BNP Paribas):

How will margins evolve during the year?Answer (Marco Wirén):

New product launches will weigh on margins in the first half of the year. An improvement is expected in the second half as production scales up.

Summing up the analysts’ questions, their focus is clearly on optical and IP networks. And Nokia was very bullish in their commentary. I suspect expectations will shift quite a bit toward 2027 when their own production capacity increases 10x compared to before—specifically InP and PIC.

Something in Nokia’s views has changed since the CMD. Back then, the talk was that their own factories were likely a good decision, and they were fairly confident in this investment. Now, in my opinion, they were more certain—stating that these are at the core of Nokia’s technology and a new factory is needed to meet demand. Clearly, they have more information now. And in my view, reading between the lines, this will start to develop positively toward the end of the year—and above all, during 2027. This point surely became clear to every analyst. It seems a bit like 2026 is a “bridge year” where heavy investments are made for the future, and in 2027, they will increasingly begin to reap the rewards of the work done. I’m still not sure if Nvidia is a customer for Nokia’s InP or ICE-D—though it would be the most logical scenario. But it became clear now that demand will emerge in that area.

So, I think it would be quite bold for analysts to start betting against Nokia, considering the very large valuation discount compared to peers—and yes, even considering that 50% might be the (at least for now) low-margin Mobile side. It seems a bit like those who are critical in their comments are still looking at Nokia through “Mobile lenses”—now would be the opportunity to start looking more through “Infra lenses.”

15 Likes