Does anyone have definite information on whether NoHo is also involved in that Fuengirola restaurant? I wouldn’t be surprised if it were under the name of a separate company, in which NoHo might not be an owner. Does @Arttu_Heikura know, for example?

3 Likes

Noho is involved. Uusi ravintola Fuengirolaan – mukana Jari Kurri, Jukka Laaksonen ja Mika Saukkonen | Fuengirola.fi

5 Likes

At least in Tampere, Ruma, which was owned by Noho, closed at the turn of the year.

4 Likes

This could also be added here, luxury kebab with wine and run by ex-Noho Juha Nieminen. Subjective opinion, that kebab is eaten specifically when hunger is strong and the wallet is not overflowing. Perhaps this concept was doomed to fail.

Secondly, Fafas have also largely closed down. Turnover is therefore high, and it seems that Asian food in various forms is now heavily offered to the public, at least in the Helsinki metropolitan area (Korean BBQ, sushi/Chinese buffet, Vietnamese, and various noodle soups). In addition, chicken seems to be popular, e.g., Pretty Boy Wingery, Chitr Chicken, and the wing places previously mentioned here. There also seems to be no end to the growth of pizza; Luca was never scaled, and Pizzarium also met its fate. Perhaps pizza is too time-consuming to prepare profitably with its dough, and/or the competition is too fierce.

Karaoke is also successful; if Jouni Lanamäki sold the venues to Noho, the man is getting old.

6 Likes

In my opinion, Noho’s business idea involves closing and opening restaurants. Customers constantly crave something new. The restaurant business is like this. While Noho has closed restaurants, it has also opened new ones.

I eagerly await the 2024 results.

18 Likes

The ‘ugly’ one was, at least years ago, the last version of the location, after which it was properly renovated.

In itself, it’s still quite understandable if the restaurant’s concept changes every now and then.

1 Like

Babista’s food is weak compared to “artisan kebab” competitors (Baba Döner, Bröner, DIF Döner). That probably explains the poor success more than the concept itself.

3 Likes

Noho is among OP’s small-cap stock picks, according to the latest Pörssitutka. Other small-cap favorites include Puuilo, Revenio, and Nurminen.

They praise Noho’s ability to defend profitability in a challenging market.

13 Likes

NoHo Partners has acquired the restaurant business of Wanha Satama from PRO Ravintolat Oy. The business will become part of NoHo Partners starting from March 1, 2025. Wanha Satama is a 130-year-old event venue in Helsinki, capable of hosting events for up to 2,000 guests. Wanha Satama attracts over 45,000 visitors annually.

24 Likes

PRO Ravintolat (future Bon Group) is the same entity that was featured in the news in late autumn when Rally World Champion Kalle Rovanperä and investment company Fredman Capital joined the group as owners: linkki

The article heavily painted a picture of Bon Group as a growth company, with plans to multiply its turnover several times over in a few years. Then, however, the company sells off business operations. What could the seller be thinking? Have the new owners brought the idea to the company that the portfolio needs to be simplified: event production out and focus on food and entertainment restaurants? Bon Group seems to have the most of these when browsing their website.

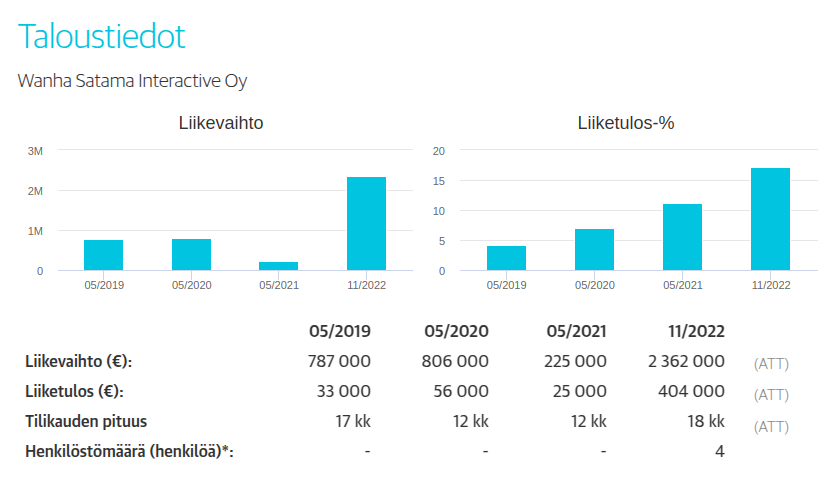

Screenshot from Kauppalehti’s pages, showing Wanha Satama Interactive’s old financial data. I’m not sure if the WS Interactive Oy at the bottom is the restaurant business bought by NoHo, but those are good figures from the corona era

Edit: After deeper investigation, I suspect that the target to be acquired is the catering operation of Wanha Satama: https://www.wanhasatama.fi/catering/ The page refers to Pro Ravintolat as the responsible party.

8 Likes

The Christmas party season was quite good, says Suominen.

According to LinkedIn, Jussi Laakso, restaurateur of Pro Ravintolat / Wanha Satama, has started at NoHo as the operational manager of Messukeskus restaurants. One could conclude from this that the aforementioned Wanha Satama business was acquired cheaply.

20 Likes

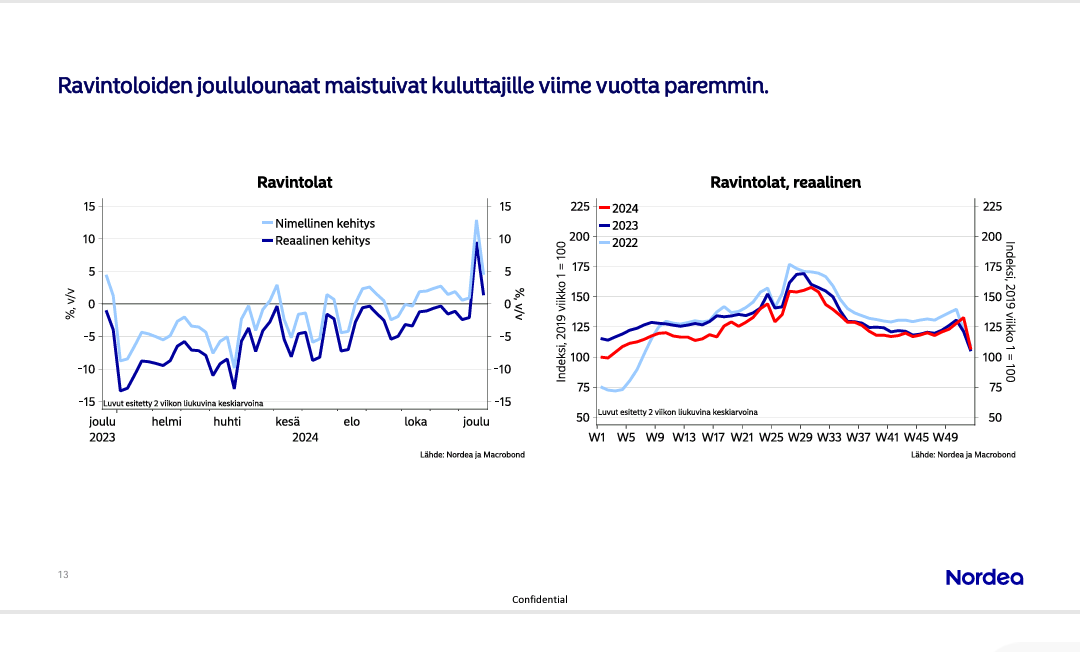

https://corporate.nordea.com/article/96931/kulutusmittari-joulukulutus-jai-piippuun

According to Nordea, Christmas lunches were enjoyed.

29 Likes

Nordea suhtautuu tulosennakossaan edelleen positiivisesti NoHoon. Suorituksen ennakoidaan olevan pehmeää markkinaa parempi ja näkymätkin kuluvalle vuodelle ihan hyvät. Fair Value-haarukkaa nostetaan piirun verran: NoHo Partners: Expecting market outperformance - Nordea - Inderes

Ahead of NoHo’s Q4 2024 report, due out 12 February, we tweak our estimates. We expect the company to reach its guidance of EUR ~430m in net sales, with a ~9.5% EBIT margin, for 2024, as we argue that NoHo’s performance is superior to the sluggish market growth witnessed throughout the year. For 2025, we expect a solid year, characterised by low-single-digit market growth and continued international expansion. With a positive outlook ahead, we derive a higher fair value range of EUR 11.4-14.4 (10.9-13.7) per NoHo share by equally weighting our DCF- and multiples-based valuation methods.

20 Likes

I must correct here that Bon Group (formerly Pro Restaurants Oy) and PRO Ravintolat Oy are two completely different operators, even though the names are similar. So the growth-oriented Bon Group did not sell Wanha Satama. Bon Group currently operates in the Savo and Oulu regions.

3 Likes

A new player is emerging for NOHO, an important part of Tampere’s restaurant scene ![]()

![]() !

!

The Swedish-born, circus-themed tapas restaurant Pincho Nation, founded in 2012, states its goal is to open ten new franchise-operated restaurants in Finland over the next three years. They are already in Turku (since 2018) and Lahti (since 2021), and a restaurant will open in Helsinki in the spring. Perhaps in Tampere later this year too?

We are currently looking for a franchise partner and a suitable location for the restaurant in Tampere. We hope to succeed in this as quickly as possible. I cannot yet say when we will come to Tampere, says Henrik Fischer, the director responsible for Pincho Nation’s chain expansion, to Tamperelainen

The restaurant’s operating model is exceptional - all orders are placed via a mobile application. With the app, customers can book a table, browse the menu, and place orders. Food and drinks can be ordered with one click, and the bill is also paid via the app. In addition, the restaurant has its own bonus program, through which customers can earn, for example, free tapas and other gifts.

This operating model probably somewhat curbs the need for staff, as at least some of the traditional waiter tasks are performed by customers. The company presents its franchise operations on its website and mentions approximately 5-6% better profitability than the industry average We are one of the leading franchise concepts in Sweden and perhaps among the most successful. More than 80% of our restaurants are run by franchisees, local entrepreneurs who love the restaurant they operate. We believe our franchisees are our super power and in general they have a 5–6 % higher profitability than the industry average. Franchise || Pincho Nation

All in all, it seems like an interesting place and will probably at least partially impact NOHO’s restaurant market. I haven’t gone through the menu, but it seems to be quite comprehensive and includes a wide variety of dishes. It should be easy to feed or quench the thirst of people with varying levels of hunger and thirst here. The price level should also fall into a suitable category for many, as the price of individual tapas is likely somewhere between 4-8€. Thus, one can buy a suitable amount for each person according to hunger and price. Regarding the location of business premises, the website states the following:

CITY/LOCATIONS

Normally, we focus our attention on cities with at least 70,000 inhabitants, but there can be exceptions. For example, cities with a lot of tourist activity during the summer or winter season may also be considered. The location should be central. The most important criterion is that it is located in a lively area surrounded by bars, restaurants, and shops. We prefer to open restaurants in areas where people often go out to eat in the evenings.

One final observation is that in Turku, the restaurant at least seems to be popular and its position has somewhat stabilized during its seven years of operation. In Google reviews, the Turku restaurant has 4.3/5 stars and just over 800 reviews.

13 Likes

It’s probably good for Noho that it operates in large arenas. In Tampere at Nokia Arena and Tammela Stadium, as well as in Helsinki at Messukeskus and Old Port. This way, Noho can participate well in large events.

Additional acquisitions may indeed come in that area.

4 Likes

Abroad, this implementation is clearly encountered more often than in Finland. In Helsinki, I have used a similar system in a couple of restaurants. In my opinion, it’s also smooth from a customer experience perspective, as you don’t have to wait for the waiter to be busy. Conceptually, it suits fast food/casual places, but not necessarily fine dining or bistros, where people go to spend time and enjoy the atmosphere.

16 Likes

The former Hartwall Arena or the recently re-initiated Helsinki Garden would be potential next targets for NoHo.

10 Likes

OP raised NoHo’s target price to €9.9 (previously €9) in its Q4 preview and reiterated its BUY recommendation.

Short quote from the report:

“The demand situation remained quite subdued in markets relevant to NoHo during the past year. Based on consumption indicators, market development in Finland was nominally roughly at the level of the comparison period, but real consumption contracted. We expect gradually strengthening purchasing power to broadly support demand for restaurant services during the current year. In our view, this will strongly benefit NoHo, which has operated in a challenging environment, and we anticipate the company’s earnings to continue on a solid growth path in 2025 as well. Our target price rises to 9.90 euros (previously 9.00), with which we reiterate the share’s BUY recommendation.”

16 Likes

There are rumors in the city that the restaurant operations of the former Hartwall Arena would return to Restel, and without competitive bidding. This is, of course, second-hand information.

1 Like