It’s been quiet on the forum regarding this company, but it would be nice to hear some thoughts on it in something other than the other national language [Swedish] via a translator. We are talking about a Swedish pharmaceutical company developing a treatment for nail fungus. Their current drug candidate, MOB-015, successfully cleared Phase 3 and received the green light in several European countries, and as I understand it, the launch should begin in Sweden early this year. The second round of Phase 3 will be completed in January 2025, after which the US markets will hopefully open up.

There is currently no treatment for nail fungus that is both effective and safe at the same time. The most effective treatment is terbinafine in tablet form, but since it is highly hepatotoxic, it is not an ideal drug. Current topical medications, on the other hand, don’t strain the liver, but the fungus tends to remain in the nail with an unnecessarily high probability. With its new topical drug, Moberg has succeeded in delivering the already known effective terbinafine into and through the nail in high concentrations. Terbinafine administered this way gives the fungus the boot, but blood concentrations do not rise high enough to irritate the liver. In Phase 3, MOB-015 achieved healing in 76% of cases (84% in Europe and 70% in the US), while only 42% with the comparator drug were able to live without nail fungus.

So, the commercialization of a promising drug for an ailment lacking good treatment is now ahead. This isn’t the company’s first rodeo with a new product launch; they have previously successfully developed and launched a product called Kerasal Nail and sold it in 2019 for about 1.4 billion SEK.

What I’ve written should be taken with a grain of salt and there may be errors, as behind this pseudonym is a novice investment enthusiast who knows next to nothing. It would be nice to hear what @Vino_Pino@Rushimato@jerej@Clark_kent, who provide expert commentary on pharmaceutical companies and clearly know the industry better than the average person, think about the company and its future.

I’ve had this in my portfolio on and off since 2016, which is also how long I’ve been following it. I’m likely slightly in the green over this period. I recently added it back to my portfolio at 6 SEK but sold it off hastily at 11 SEK, as it rose too quickly for my liking. I’m thinking of buying back in under 10 or if the fundamentals improve.

The product definitely has potential; however, the company’s own estimates for sales etc. are too rosy. In my own calculations, I assume that even though nail fungus (KS) is a common ailment, only about 10% likely seek treatment for it.

In the near future, I hope the terbinafine supplier issue is resolved.

P.S. I’ve been wondering why the company’s long-term CEO Wolpert didn’t subscribe to much in the share issue, despite likely earning tens of millions a few years ago when the OTC business was spun off.

This is quite an interesting case. From a general practitioner’s perspective, nail fungus is indeed somewhat annoying. The condition is almost always practically harmless, but it is nonetheless bothersome to many patients. Patients only come to complain about it once the changes affect the entire nail and/or multiple nails. At that point, the topical preparations currently on the market almost never help. If the patient wants treatment, p.o. (oral) terbinafine is practically the only option. This oral terbinafine is problematic in several ways:

The treatment course is long (approx. 3 months)

The drug has many interactions with other medications (liver metabolism, effect on CYP enzymes)

Nail fungus often occurs specifically in elderly multimorbid patients who are already on many medications

Elevation of liver enzymes, requires some monitoring

As a sum of these factors, the current treatment is long-term, involves some side effects, and requires a lot of effort. And despite all this, treatment response rates are quite poor, in the 50% range. At least as a GP, I would greatly welcome better products for treating nail fungus.

A new, much more effective topical treatment product certainly has a massive market opportunity. The company’s estimate of the sales potential (250-500 MUSD/year) is, of course, very high and probably on the high side. However, the ailment is very common and the company’s current MCAP is 450 MSEK (45 MUSD), which is quite modest relative to the market potential. And since the active ingredient is the same terbinafine, there shouldn’t be an outrageous risk of major setbacks in the remaining trials following the current studies. The current evidence from already published studies is good and will most likely continue to be so. At least according to estimates, more research data was expected by 01/25.

The company’s balance sheet is net debt-free, there is very little debt, and the cash position is at the 100 MSEK level. At the current rate, the cash burn is 20-30 MSEK/year, so the cash should last until MOB-105 starts generating significant cash flow (from sales through partners or from selling the drug). Currently, they have already secured a nice number of partners in different regions (“in Europe (Bayer), South Korea (Dongkoo), Canada (Cipher), Allderma (Scandinavia) and Israel (Padagis)”).

Thank you JNivala for an absolutely excellent summary!

What I started wondering about is that people are quite skeptical of those topicals because their response rates are indeed quite weak, but they are still the benchmark from which we should start gauging the market size. Could someone dig up the sales for a couple of peer products from somewhere?

There’s all kinds of snake oil on the market for that ailment, and some don’t even try to claim they work if you read the label information carefully, but they are still sold in pharmacies nonetheless. I’ve wondered how they are even allowed to be sold when they just claim to “successfully lighten the nail.”

This is a challenging case in the sense that it’s an OTC product, so consumer product principles also apply—meaning marketing, product positioning, and succeeding in communicating that superior efficacy etc. play a significant role.

So, unfortunately, it’s not as straightforward as with prescription drugs where the medical community is aware of the evidence, but then again, those big pharma companies are largely marketing firms anyway, so it shouldn’t be an impossible task if the product is that good.

I’ll have to take a closer look if I ever have time. Thanks for the heads-up and the tag!

The perennial problem with these topical treatments has been that the drug does not reach the nail matrix, from where the nail grows. Even if topical treatment manages to keep the fungus in the visible part of the nail under control, new fungus emerges as the nail continues to grow. Through oral administration—meaning via the bloodstream—the medication reaches the nail matrix. Nevertheless, the results do not show 100% cure rates.

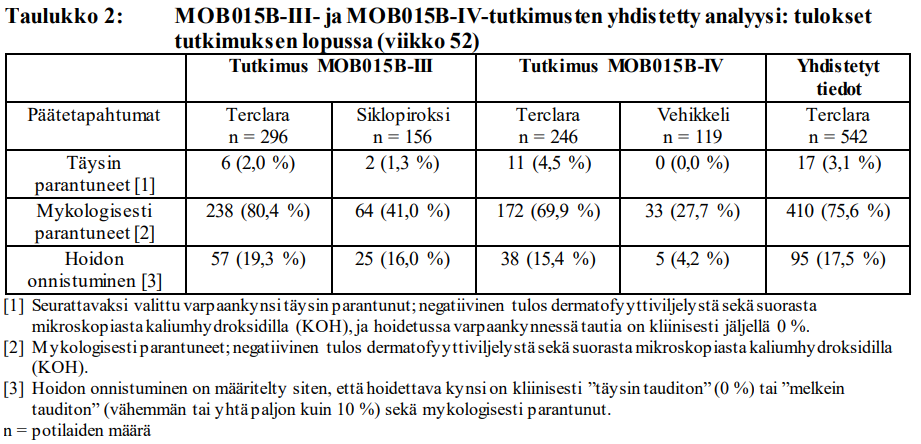

In this Phase 3 study, only fungus at the tip or side of the nail was treated, covering 20–60% of the nail area—not the entire nail, which is the most difficult case. A complete cure was observed in 4.5% of cases. The treatment required 336 daily applications to the nail. Have better results been presented?

This is primarily the treatment of an aesthetic issue. It doesn’t appear to be a particularly effective treatment. Regardless, there might be a business opportunity here; there are likely users for it globally. Use would likely require repeated treatment, which is good for business. Whether this leads to local side effects remains to be seen.

Sales of this will likely start under the name Terclara. I found a summary of the MOB-015 studies on Fimea’s website. Apparently, the superiority over other topical medications is the high proportion of negative fungal culture samples after the treatment period. Proportion of mycological cures (>75%) vs. the best comparator (~40%). I would like to hear from @JNivala@Vino_Pino and others whether this could be a sufficient differentiating factor compared to other treatments? (my profession is not in the medical field)

At one point, I hoped they would have bought out Moberg after the sentiment turned sour following the autumn share issue. Lost potential. However, if MOB-15 is indeed as good as it looks, they would have a good chance of capturing the local market.

The company’s revenue is approximately $20 million and the local nail market is $80 million, so the potential is significant. Cipher also has other business operations and cash, so the company has broader shoulders, and thus the business carries lower risk. The company has also been active with share buybacks recently, so they seem to understand shareholder value creation.

That “mycologically cured” is problematic in that the sample is taken from the nail by scraping/carving from a spot determined by the person taking the sample after topical treatment, meaning the medicine might kill the fungus in the part of the nail where the medicine was applied and successfully penetrated, but as previous writers mentioned, in difficult-to-treat cases, the fungus is deeper in the base where no sample is taken. A toenail takes over half a year to grow, so regarding the results in the table you posted, one should also know when the sample determining the cure was taken.

A sample can be negative for a long time when taken from the tip/surface of the nail after treatment, even if the treatment has essentially failed and the fungus is slowly regrowing from deeper down as the nail grows.

But even without any further information, there is still a clear difference compared to the control, meaning you could say it works better.

Even if it’s an over-the-counter (OTC) drug, word of a working product spreads effectively. Pharmaceutical reps also make their rounds and advertise. A doctor will then recommend the product in question to a patient without a prescription when they can even say by name: go buy this, it’s more effective.

We should think about this from the customer’s, i.e., the patient’s, perspective. They notice that the “nail is ugly.” The doctor sees the same thing. They consider whether the nail is damaged or if there is fungus. A culture is taken. The result is positive, and treatment begins. It lasts 336 days, and after treatment, two out of a hundred patients see that the nail looks healthy. With the competing ciclopirox treatment, it’s 1.3 out of a hundred. Is the difference significant? It doesn’t seem to be. Or as a result after that nearly year-long treatment, where “no more than 10% of the nail is ugly,” the percentages 19.3/16 also don’t seem to differ significantly.

The fact that Terclara, or topical terbinafine, can suppress the fungus enough to achieve a “mycological cure”—meaning nothing grows in the fungal culture—likely won’t mean much to the patient if the nail still doesn’t look healthy. The same story can be applied to treatment done without a doctor, where the patient buys the same drug over-the-counter with the same results. I wouldn’t use that percentage as a measure of the treatment’s effectiveness.

As a layman, I wonder/consider why, for example, ciclopirox medicated nail polish is used at all when its results are so weak? If, instead of bad results, one could get slightly less bad results with Terclara, could this be an option then?

The VIC pages linked by @Jackfin mention that they are trying to improve the cosmetic appearance by changing the dosage size. Time will tell if it succeeds.

“The only issue that MOB had is that it failed the cosmetic parameter – what the nail looks like. As a result, they’re conducting a 2nd trial that lowers the dosage so that it will hopefully not affect nail coloring too much while still maintaining a superior mycological cure rate. If Moberg can hit that complete cure rate target, MOB will be positioned for a lot of success and Cipher’s marketing rights in Canada should be quite valuable. Assuming all goes well, this product is roughly 24-30 months away from commercialization.”

It could very well be an alternative. In your table, the figures do not convince me of its superiority.

By the appearance of the nail, I meant how it looks after the treatment, i.e., it hasn’t healed. As an additional problem, it is mentioned there that terbinafine discolors the nail. They intend to try reducing the strength. The risk there is that it won’t even work that well anymore, even though the concentrations are high to begin with. However, and again, no measurements have been taken from the nail matrix—where the nail grows from out of sight, i.e., near the surface of the bone—so it shouldn’t be compared to the concentrations of orally taken medication.

Why people use these not-so-effective treatments is not a medical question. It is perhaps more of a psychological-sociological one. Everyone likely starts their own experiment full of hope. Why do those perceived as women spend hundreds of euros on day and night creams for their faces year after year? Apparently, many perceived as men do too.

A press release was issued yesterday stating that sales have (finally) started in Sweden and it’s apparently available in most pharmacies now. Sidan kunde inte hittas | Moberg Pharma. It is also available for order from online pharmacies without a prescription, and the price seems reasonable for both the consumer and the seller, i.e., slightly under 40e/package: https://www.kronansapotek.se/Terclara/p/042620/

Based on published studies, the product’s efficacy should be quite good compared to other nail fungus treatments and is comparable to oral terbinafine. The temporary whitening of the nail as nail permeability improves (moisture content increases) shouldn’t be a long-term problem if the mycological efficacy is truly good. The product’s efficacy is based specifically on this improvement in nail permeability. Topical terbinafine alone without excipients has been tested in randomized trials before, and the efficacy was very poor. More will be known about the efficacy and potentially fewer aesthetic drawbacks with reduced dosing after the currently ongoing study in early 2025.

It was also commented above that nail fungus is only an aesthetic issue. This is certainly true for mild cases, but as it progresses, the fungus does cause pain as the nail thickens and changes shape, as well as predisposing to other infections and nail detachment.

Personally, I consider the presented sales potential to be entirely possible if the efficacy is truly as good as the company promises and the product becomes widely available as an over-the-counter (OTC) preparation. In that case, it is possible that Terclara will become the primary treatment for mild and moderate nail fungus worldwide.

Some sales are already happening in Sweden. Marketing authorizations have now been received in all 13 EU countries that participated in the licensing process, and Terclara is coming to market over-the-counter (OTC) in countries like Italy and the Netherlands, though it requires a prescription in Finland, for example. This comment from the CEO seems quite positive: “A majority of ~1,400 Swedish pharmacies now have MOB-015 available on the shelf under the brand name Terclara® and interest is exceeding the chains’ forecasts. The pharmacy chains are increasing their orders after consumer marketing began around the end of March due to the fact that the product occasionally has sold out at several of the pharmacy chains”

Sales in other European countries are starting off sluggishly. Based on previous comments, I thought sales would have started faster at least in the other Nordic countries, but it seems we might have to wait for a new terbinafine supplier before sales can expand. An application for a new terbinafine supplier was submitted in April, and according to the press release, the authorization should be obtained before the end of the year.

The cash position looks poor at a quick glance, but hopefully, the exercise of warrants will fix the situation. The stock has been on a strong upward trend lately, and at these prices, the warrants expiring in June are set to bring a lot of money into the coffers. This is, of course, entirely dependent on the stock price and how many warrants are ultimately exercised. Does anyone here have any insight or previous experience regarding what is likely to happen with the warrants? Will the stock price drop closer to the subscription price, and are the warrants a risky investment in that sense?

A major blow: according to preliminary data, the drug’s efficacy is weaker than expected. The press release still leaves some things open to speculation, but the market has already drawn its conclusions.

A rather vague press release since it doesn’t disclose the number of patients for whom data has been obtained, nor what that “clinical cure rate” was versus what was expected. The data is still blinded (at least that’s how I understand the release), so a fairly essential piece of information would be at least what portion of the study population this data covers.

The information obtained is blinded; no information has been received regarding which patient received active treatment or how many patients in the data subset received active treatment (patients in the study are randomized 2:1 to treatment with MOB-015 and vehicle).

I wonder where the recording or transcript of the conference call mentioned in the release might be found?

In my opinion, it didn’t provide much additional information:

-They are not publishing patient numbers or percentages because they want to “protect” the blinded data (I interpret this to mean that preliminary information about the results shouldn’t influence the results themselves or the analysis of the results).

-The data came as a surprise to the company as well, apparently in connection with some other discussion.

-The data is “disappointing” according to the CEO, but even they don’t have more detailed data yet (e.g., information on mycological efficacy), and no conclusions regarding the US launch can be made yet.

-It does not affect the launch in the EU region. In the EU, getting new terbinafine suppliers approved has a greater impact, and new marketing authorizations in the EU cannot (??) be applied for until there are new suppliers.

-It likely won’t affect launches in Israel, the UK, or Canada either. In Japan, a separate study is apparently needed regardless of the current study. If I recall correctly, the Japanese partner ended the collaboration even before the EU marketing authorizations.

-Market share is now 40% in Sweden (I interpret this as referring to topical treatments) and it is the market leader. Based on this, I would assume that the US study won’t have much of an impact on those countries where Terclara will be sold over-the-counter.

-The launch in EU countries might be delayed until 2026. I thought the explanation for this was very strange: that it needs to be brought to market early in the year when demand is at its peak. I don’t understand the logic here. For example, regarding Southern Europe, it probably doesn’t matter much if the product is released as late as autumn. But increasing sales in Europe seems slow. There is also a delay of about 6 months from pharmacies (they take on new products for sale 2-3 times a year).

Perhaps the share price reaction is a bit of an overreaction (-61%), but on the other hand, the uncertainty will continue until December when the final data is published. Even if marketing authorization is not obtained for the US, Terclara will be sold at least in the EU region.

After the USA disappointment, the strategy is now the EU. The market has punished.

Jan-Mar Oct-Dec Jul-Sep Apr-Jun Jan-Mar

2025 2024 2024 2024 2024

values in thousands SEK

Net revenue 3,869 1,027 3,855 4,109 820

Cost of goods sold -1,304 -1,165 -615 -1,388 -328

Gross profit 2,565 -138 3,240 2,721 492

OPEX is between 5-7 MSEK.

Cash is 269 MSEK. MCAP 394 MSEK.

Terclara is #1 in Sweden and the total market has also grown. This means there is hidden demand that current products have not met. Summer months are the best for sales. This should turn profitable.