H1 2025 on takana ja on aika kurkistaa mitä salkussa on tapahtunut vuoden toisen kvartaalin aikana. Volatiliteetti kasvoi merkittävästi, kun Trump ilmoitti tulleista. Kasvanut epävarmuus oli hyvä hetki tehdä pieniä muutoksia salkkuun, mutta oletin epävarmuuden jatkuvan pidempään, joten tuli myytyä yhtiöitä ilman että ehdin laittaa kaiken vapautuneen käteisen takaisin markkinoille. Tästä heräsi taas kvartaalin aikana kysymys, kannattaako ajoittaminen? ![]()

Suurinta harmia salkulle on kuitenkin aiheuttanut valuutat. Euro on vahvistunut sen verran paljon dollaria vastaan, että vaikka monen yhtiön kurssit ovat palautuneet tai ovat jopa korkeammalla kuin aiemmin, niin valuutat ovat pyyhkineet pois arvonnousun. EUR/USD kehitys onkin vuoden alusta +12%. Tällaisella kehityksellä on jo merkittävä vaikutus omaan salkkuuni, kun 19% sijoituksista on USD:ssä. Ruotsin kruunun vahvistuminen euroa vastaan on myös lopahtanut ja hyötyä on tullut vain noin 2%. Odotan pitkällä ajalla, että valuuttojen vaikutus tasaantuisi, lyhyellä ajalla niiden vaikutus on lähinnä verenpainetta kohottava.

Kotimaiset yhtiöpoiminnat ovat suoriutuneet kohtalaisesti ja tuottaneet vuoden mittaan lähes indeksiä (OMXHGI25) vastaavaa tuottoa. Ulkomaiset yhtiöpoiminnat ovat puolestaan tuottaneet 0% YTD, juuri valuuttojen takia. YTD yhteensä +7,2%. Tähän ei voi olla tyytyväinen, kun Hesuli on pyyhkinyt ohi mennen tullen.

Kvartaalin aikana tuli tehtyä kohtuullisen paljon liikkeitä.

Fortnoxista julkaistiin ostotarjous, joten tästä positiosta sai tehtyä lyhyellä ajalla hyvän tuoton. Tämä oli toki yksittäinen tapaus, mutta taas heräsi ajatus, että vaikka kertoimet ovat korkeita, ei se välttämättä tarkoita, että yhtiö on kallis. Pääomistajat näkevät ilmeisesti, että yhtiössä on edelleen merkittävää arvonluontipotentiaalia.

Salkusta lähti lisäksi Alphabet ja Berkshire. Näiden yhteenlaskettu tulos oli noin +/- 0. Luin uudestaan kirjan Berkshire Beyond Buffett ja minulle tuli vahvasti sellainen tunne, että Berkshiren sisällä on paljon keskinkertaisia yhtiöitä, joilla ei minusta ole kilpailuetua. Buffett on ja tulee aina olemaan minulle roolimalli, mutta se ei tarkoita sitä, että minun on omistettava Berkshireä.

Alphabetissa tein virheen myydessäni, mutta totesin taas myytyäni, että onpa ihanaa kun ei omista yhtiöitä, joista joka päivä kirjoitetaan jotain isoja otsikoita. Se kohinan määrä, mitä pitää Alphabetin omistajan sietää on tuskallista minulle. Sama kaava toistui, kun omistin Novoa. Aina ei voi miettiä pelkästään yhtiön kilpailuetua, vaan on myös pohdittava sijoittajan kilpailuetua. Huomasin taas uuden heikkouden omassa toiminnassani ja tämä on asia mitä pitää ottaa huomioon tulevissa yhtiövalinnoissa.

Atlas Copco käväisi myös salkussani. Ongin sitä salkkuuni muutaman prosentin verran tullihermoilussa. Teesinä oli Euroopan uusi nousu ja Atlas on myös erinomainen yhtiö omalla toimialallaan. Tulin kuitenkin toisiin ajatuksiin, kun halusin vapauttaa tilaa uusille yhtiöille salkussa ja Atlasta on merkittävä määrä Investorissa, joka on valmiiksi salkun suurin omistus. Nämä ulos pienellä voitolla.

Ostin myös Norbitia ja se ehti olla salkussa pari kuukautta. Yhtiö vaikuttaa laadukkaalta yhtiöltä, joka operoi mielenkiintoisissa niche toimialoissa. Vahva suorittaminen palkittiin aika voimakkaalla kurssinousulla ja kahden kuukauden holdilla 45% tuotto sai riittää. Vaikka yhtiö vaikuttaakin laadukkaalta, niin etenkin Oceans segmentin lyhyt näkyvyys ja toimitukset puolustussektorille saivat minut hieman varovaiseksi.

Uudet positiot: Cellavision, Lagercrantz.

Cellavision: Useat sijoituskeissini etenkin medtech yhtiöihin perustuu siihen, että yhtiöllä on markkinajohtajuus omassa nichéssä. Cellavision on juuri tällainen yhtiö. Kasvu on nyt muutaman vuoden ajan jäänyt piippuun, mutta olen varovaisen positiivinen uusista tuotteista ja pienlaboratorioiden markkina voisi herättää tämän yhtiön unesta. Yhtiö on monella tapaa Ruotsin vastine Reveniolle, mutta verianalyysissä.

Lagercrantz: Ruotsissa on joukko erinomaisia sarjayhdistelijöitä ja Lagercrantz kuuluu tähän kalliiseen ja arvostettuun ryhmään. Tulli hermoilussa yhtiötä sai hieman halvemmalla, joten aloitin ostot. Lagercrantz on kiihdyttämässä yritysosto tahtiaan, koska divisioona järjestely mahdollistaa useamman yhtiön D&D ja integroimisen. Yhtiö tekee myös jatkuvaa työtä bruttokatteen parantamiseksi ja orgaaninen kasvu on lopulta taas heräilemässä.

Yhtiö fokusoi huipputeknologiaan ja kaikkeen muuhunkin hypeen, kuten esim alkuvuonna hankittu ORAX AB osoittaa. (saattaa sisältää sarkasmia)

Isossa kuvassa salkku näyttää tutulta. Lisäsin Copartia, kun tulos oli pienimuotoinen pettymys ja kurssi ollut laskussa. Ostin myös lisää: Harvia, Investor, MIPS, Shopify, Moody´s, Visa.

Arvostukset ovat koholla ja uskon sen hillitsevän suurimpia kurssinousuja lähiaikoina. Joulupukille tulen esittämään tänä vuonna sellaisen toiveen, että saisin ostaa Vaisalaa sopivaan hintaan vuoden aikana. Yhtiön tekeminen ja kehitys on yllättänyt minut positiivisesti ja samalla varmistanut sen etten ehtinyt rakentaa riittävän suurta positiota.

Viime salkkukatsauksessa nostin esille kaksi yhtiötä. Medistim ja Marimekko.

Medistim

Medistim julkaisi erittäin vahvan Q1 tuloksen. Konferenssipuhelussa yhtiö jopa hillitsi sijoittajia siinä mielessä, että tämä oli poikkeuksellisen vahva kvartaali ja tällaisia tuloksia ei tulisi odottaa jatkuvasti. Yhtiö suoritti erinomaisesti jokaisella osa-alueella ja tämä luo uskoa, että yhtiön tuotteet ovat laadukkaita ja kilpailukykyisiä.

Pientä huolta minussa herää sen suhteen, että medtech toimialalla olisi ollut tietynlaista ennakoivaa kysyntää tullien takian. Sen verran voimakkaita tuloksia nähtiin Q1:lla. Toimialan yhtiöt kuitenkin puhuivat laajasti kysynnän normalisoitumisesta, joten tulee olemaan mielenkiintoista nähdä miten käy Q2 tuloksien.

Marimekko

Marimekko puolestaan petti omat odotukseni, mutta ylitti hitusen markkinan odotukset. Marimekon tulos vaihtelee toki merkittävästi sen mukaan mille kvartaalille suuremmat tukkutoimitukset ajoittuvat ja tämä tekee kvartaalien välisestä vertailusta hankalaa, mielekkäämpää on siksi tarkastella koko vuoden tulosta. Odotin kuitenkin vahvempaa tulosta Aasiasta, kun uusia liikkeitä ollaan sinne ahkerasti avaamassa. Tätä tulee monitoroida.

Tällä kertaa ajattelin nostaa esille Dynavox nimisen yhtiön.

Dynavox spinnattiin Tobii nimisestä yhtiöstä vuonna 2022, hetken se oli pörssissä nimellä Tobii Dynavox, mutta nykyisin vain Dynavox Group.

Dynavox mahdollistaa kommunikoinnin henkilöille, jotka eivät pysty kommunikoimaan oman äänen avulla, tai tarvitsevat tähän apua. Yhtiö on markkinajohtaja alallaan ja ilmeisesti ainoa, joka tarjoaa kokonaisvaltaisen ratkaisun. Yhtiö myy niin softaa kuin apuvälineitä mm liikkumiseen. Tuotteita myydään 65 maassa ja yhtiöllä on 500 kumppania julkisella ja yksityisellä puolella.

Markkina, jossa yhtiö toimii, on alipalveltu. Yhtiön mukaan vain 2% henkilöistä, joilla vuosittain todetaan kommunikointi hankaluuksia, saavat siihen tarvittavaa apua. Yhtiön tuotteet myydään loppukäyttäjälle lääkäreiden kautta, joten yhtenä tärkeimpänä asiana on, että yhtiö kasvattaa tietoisuutta alan ammattilaisten seurassa. Pörssihistoria omana yhtiönä on ollut toistaiseksi menestys.

Hyvään kehitykseen on syynsä, liikevaihto on kasvanut voimakkaasti ja kannattavuus niin ikään.

Q1 liikevaihto kasvoi peräti 36% ja EBIT 38%. Ilman kertaluonteisia kustannuksia EBIT marginaali olisi parantunut 7,6% → 11,3% verrattuna vuodentakaiseen ensimmäiseen kvartaaliin. Odotan, että EBIT liikkuisi 15% tasolle pitkällä ajalla.

Näin voimakas kasvu herättää minussa aina huolta ja olenkin maltillisen skeptinen sille, että markkina ottaisi Q2 tuloksen yhtä innokkaasti vastaan.

Tässä yhtiössä kiehtoo iso palvelematon markkina ja voimakas kasvu, ilmeisesti hyvät tuotteet, jotka ovat korvauksien piirissä monella markkinalla. Ehkä isoin kysymysmerkki minulle on se, että miten markkina houkuttelee kilpailijoita. Yhtiöllä ei ole mielestäni erittäin vahvoja kilpailuetuja, vaan kilpailutekijät ovat omasta mielestäni yhteistyöt ja kokonaisratkaisu.

Yhtiön mielestä heidän rakentamat verkostot asiakkaiden rahoituksen turvaamiseksi on kilpailuetu. Kun asiakkaiden mahdollisuus ostaa yhtiön tuotteita ja palveluita on sidottu tukiin, on myös huomattava se riski, että yhtiöllä voi olla vaikeaa nostaa hintoja. Toistaiseksi bruttomarginaalia on kuitenkin suojeltu hyvin ja se on nousemassa kohti 70%.

Yhtiön ympärillä on myös riittänyt spekulaatiota siitä, että yhtiö ostettaisiin pois pörssistä. Korkea arvostus on nyt varmasti este tälle.

Salkku

Olen edelleen tyytyväinen salkun läpivalaisuun. Omistamani yhtiöt ovat hyvin kannattavia ja tuottavat vahvasti sijoitetulle pääomalle. Arvostustasot ovat korkeita.

Toisaalta kun mietitään arvostuskertoimia niin näitä pitäisi suhteuttaa kasvuun. Sir Chris Hohn nosti esille erinomaisen asian Moody´sista hiljattain julkaistussa haastattelussa. Moody´s on viimeisen sadan vuoden aikana kasvanut keskimäärin 10% vuodessa ja sen kasvua on aina aliarvioitu. Tällaisista yhtiöistä voi maksaa korkeampaa hintaa, mutta tärkeää on pitää mielessä, että tällaiset yhtiöt ovat erittäin harvinaisia ja kasvu voi loppua seinään. Olenkin varma, että moni salkkuyhtiöistäni ovat lakanneet olemasta seuraavan sadan vuoden aikana, mutta en ikävä kyllä tiedä mitkä niistä. John Wanamaker tunnetusti sanoi ”I know half my advertising budget is wasted; the trouble is I don´t know which half”. Tämä pätee myös sijoittamiseen.

Tästä anekdoottina päästäänkin siihen, että sijoittajan on hankala tietää mitkä yhtiöt tulevat olemaan ne salkun parhaat. Havahdun usein siihen, että pienet positioni suoriutuvat erinomaisesti, kun taas suuret ja omasta mielestäni ”varmat” positiot tuottavat keskinkertaisesti. Oma päätelmäni on se, että on paljon asioita, joita emme sijoittajana tiedä ja pysty kontrolloimaan. Siksi tietynlainen nöyryys on hyväksi ja minun on hyvä pitää salkussa noin 25 yhtiötä. Sillä tavoin saan mukaan myös sellaisia yhtiöitä, jotka tuntuvat hyviltä sijoituksilta, mutta eivät mahtuisi millään salkkuuni, jos minun pitäisi valita vain 5-10 yhtiötä. Tämä lisää optionaalisuutta sen suhteen, että voin vain hävitä 100%, mutta jokin pienemmistä positioista voi kasvaa merkittäväksi positioksi.

Edelleen salkussa on vähän odotteleva tunnelma. Harva omistamisen arvoinen yhtiö näyttää mielestäni houkuttelevalta juuri nyt. Ideoita on ollut vähä heikosti ja pari ideaa ehti karata käsistä…(Nexstim). Tulee olemaan jännittävää seurata miten yhtiöt ovat pärjänneet valuuttojen kanssa, kun Q2 tulokset julkaistaan. Aika monella omistamallani yhtiöllä on paljon myyntiä dollareissa.

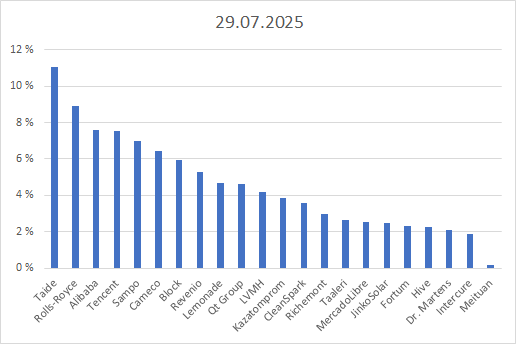

Salkussa on 22 yhtiötä. Kolme paikkaa on auki, mutta näillä kertoimilla tuntuu vaikealta lisätä yhtiöitä. Näissä tunnelmissa kohti Q2 raportteja.

Hyvää kesää kaikille! ![]()