Shouldn’t you just bravely put that portfolio on Shareville too ![]() Apparently it was removed at some point. It’s a bit strange that not even a single analyst is there, except maybe one…They analyze, but they don’t invest themselves

Apparently it was removed at some point. It’s a bit strange that not even a single analyst is there, except maybe one…They analyze, but they don’t invest themselves ![]()

5 Likes

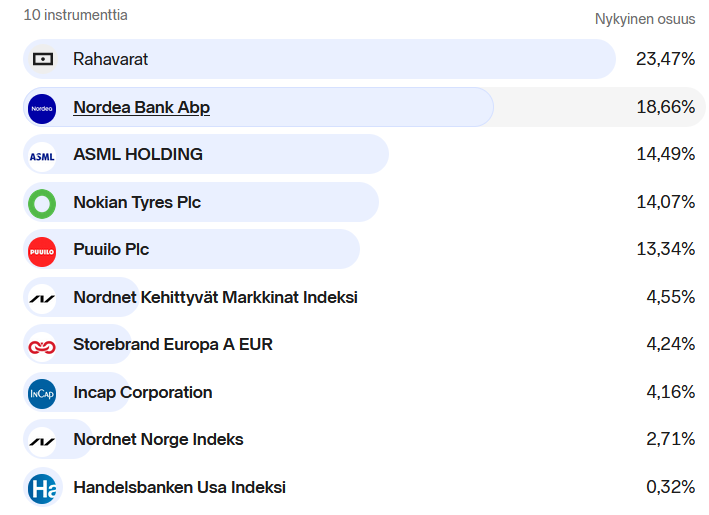

Above is the current portfolio content. In addition to this, the company’s bonus fund, which is the second largest holding.

Nordea - Still the cornerstone of the portfolio.

ASML - A newcomer I grabbed from Nordnet’s offer. A technology leader in an interesting field.

Nokian Renkaat - New factory and strong brand. If a turnaround doesn’t start to show, I’ll sell the shares for something else.

Puuilo - In my opinion, a brilliant concept. However, the valuation is quite tight, so no additions in the near future.

Incap - I definitely intend to add more, but I’ll monitor the current position for a while longer. I hope the management finds use for the massive cash pile.

Funds - On Wednesday, I returned to the US market through a fund. I consider the Oslo stock exchange cheap and, of course, it’s available without fees. I’m very bullish on Europe and emerging markets for diversification. All of these are in monthly savings, which I started rolling again the month before last.

Cash - For once, a situation where not everything is tied up in the market. I’m waiting for buying opportunities and letting the monthly savings roll.

Potential targets - Evolution, which was already in the portfolio. Let’s see the results for the current quarter and then decide. Relais Group has piqued my interest, and I’m keeping an eye on it. There might be a buying opportunity in Novo. I’m particularly interested in the weight loss drug market, but I wouldn’t want (again) a falling knife in the portfolio. Incap addition is probably the most likely next purchase. In addition to these, some domestic engineering company would be of interest.

I like the portfolio holdings. Once we can increase the weight of the funds, I’ll be even more satisfied.

24 Likes

There’s always something at a loss in my portfolio. However, nothing has ever been as much in the red as Neste. Tieto, UPM, and Novo Nordisk are also in the red. Sampo, Kesko, and Faron are in the black. As are the funds, Phoebus, Spiltan Högräntefond, and Selugson’s money market fund. This is what we’re going with.

6 Likes

Another update. Quite a few changes have occurred in the past half-year.

1. ETFs and Funds — 25.29 %

| Fund / ETF | Symbol | Weight |

|---|---|---|

| iShares Core MSCI World ETF | IE00B4L5Y983 | 7.67 % |

| iShares Core MSCI EM IMI ETF | IE00BKM4GZ66 | 6.24 % |

| iShares Core MSCI Europe ETF | IMAE.EURONEXT | 4.66 % |

| iShares Automation & Robotics ETF | IE00BYZK4552 | 4.03 % |

| Svea Index | sve index | 1.98 % |

| Nordea BetaPlus Global Equity | LU0994677119 | 0.71 % |

2. Domestic Stocks — 35.64 %

| Company | Symbol | Weight |

|---|---|---|

| Nordea | NDA FI.HEL | 6.83 % |

| Wärtsilä | WRT1V.HEL | 5.28 % |

| Admicom | ADMCM.HEL | 4.73 % |

| Kempower | KEMPOWR.HEL | 4.48 % |

| Qt Group | QTCOM.HEL | 3.38 % |

| Huhtamäki | HUH1V.HEL | 3.15 % |

| Optomed | OPTOMED.HEL | 3.03 % |

| Neste | NESTE.HEL | 2.83 % |

| Talenom | TNOM.HEL | 1.93 % |

3. Foreign Stocks — 39.07 %

| Company | Symbol | Weight |

|---|---|---|

| British American Tobacco | BATS.LSE | 10.54 % |

| AMD | AMD.NASDAQ | 6.99 % |

| Take-Two Interactive | TTWO.NASDAQ | 5.03 % |

| AstraZeneca | AZN.LSE | 4.85 % |

| Evolution AB | EVO.STO | 4.78 % |

| BAE Systems | BA..LSE | 4.31 % |

| Novo Nordisk | NOVO B.CSE | 2.57 % |

I asked ChatGPT how my previous portfolio differs from the current one:

"1. Structural Changes by Main Category

| Group | Previous Weight (%) | Current Weight (%) | Change |

|---|---|---|---|

| ETFs and Funds | 23.22 % | 25.29 % | |

| Domestic Stocks | 44.02 % | 35.64 % | |

| Foreign Stocks | 32.76 % | 39.07 % |

Summary:

Your portfolio has shifted towards a more international and ETF-heavy direction. The share of Finnish stocks has clearly decreased, and the emphasis on high-quality foreign companies has increased."

I agree with that. I have consciously aimed to reduce the weight of Finnish stocks. There is still an overweight in them, of course.

Then:

" 2. Most Significant Individual Changes

Sold or Removed Stocks

Sold or Removed Stocks

| Stock | Comment |

|---|---|

| TietoEVRY | Sold – weak performance, sensible decision |

| Valmet | Sold – share price near target, cyclical |

| Nokian Renkaat | Sold – good decision due to difficult outlook |

| Harvia | No longer in portfolio – possibly sold, not visible in current one |

| Palantir | No longer visible – you have likely sold (or significantly reduced) |

It’s nice when ChatGPT praises my investment decisions!

" ![]() New Stocks

New Stocks

| Stock | Comment |

|---|---|

| AstraZeneca | Defensive, high-quality – good ISA choice |

| Evolution AB | Technology-driven growth, excellent replacement for Tietoevry |

| BAE Systems | Defense industry – timely and strategic addition |

| Novo Nordisk | Top quality, low risk – excellent new company |

| Huhtamäki | Stable cash flow and dividends – good ISA investment |

Indeed, quite a few new stocks have been added to the portfolio. AstraZeneca and Novo Nordisk bring diversification to the pharmaceutical markets. AstraZeneca has good drugs and a strong pipeline. For example, the use of dapagliflozin (Forxiga) is constantly increasing, and new indications seem to be emerging all the time. Novo Nordisk is at the forefront of obesity treatment, with Ozempic as the spearhead. The share price has been beaten down quite a bit now, and thus it is also currently at a loss. But there is faith in the future.

I wanted to buy BAE Systems because Europe (hopefully/likely) is also starting to prepare militarily, and Germany is beginning to stimulate its economy, and the EU is also planning joint funding, etc. BAE also has the aerodefence and similar sectors involved, possibly participating in the drone business in the future?

Evolution started to interest me when the share price had been beaten down and the numbers started to look reasonably good. I don’t know the company in great depth, but there’s probably some so-called “safety margin” already? Pyysing also seemed to be buying. Kempower brings more growth to the portfolio.

25 Likes

Well, it turned out that I put the rest of my cash into Faron during the previous dip, and now the portfolio is full of it, so with this, we’re going somewhere (to the moon? ![]() ), but let’s see calmly how it goes

), but let’s see calmly how it goes ![]()

![]()

53 Likes

So it happened that the curve swung above the target level. At the current level, one could quite carefree live life without the rat race of working life.

Inspired by exceeding the target, I also tentatively set the date 6.6.2026. It’s not set in stone by any means, but now the target would be known. A year to thoroughly think about my own dreams and aspirations to be realized after my career. Perhaps the goal is to try to slow down even during the last year at work, so as not to get entangled in all work anymore. And work in the future is not ruled out, but a complete detachment for some time is indeed the goal. Perhaps some of my own work projects or then some lighter occupation.

One extra year would bring an emergency buffer and risk provision. In practice, living would be solely on the portfolio’s dividends and interest. A debt-free two-room apartment could also be added as a buffer.

So what changes to the portfolio?! There is no longer a need to actually accumulate wealth, but rather to start protecting it. So the short-term goal is to grow boring and stable dividend machines and purely a “war chest” for bills.

Unnecessary hasty sales should be avoided. After declines, prices tend to rise in due course…

Whew! Quite something, when the goals actually start to be met and one should wonder about the next 20 years ![]()

70 Likes

The dividend strategy has become somewhat fragmented, as Iris Energy and Fluence Energy have been added as new holdings since the previous review. And LVMH cannot really be called a dividend stock either.

In addition to these, there is an index portfolio in Nordnet with a market value of 12k, including:

Nordnet Global Index,

Nordnet Sweden Index, and

Nordnet Finland Index.

24 Likes

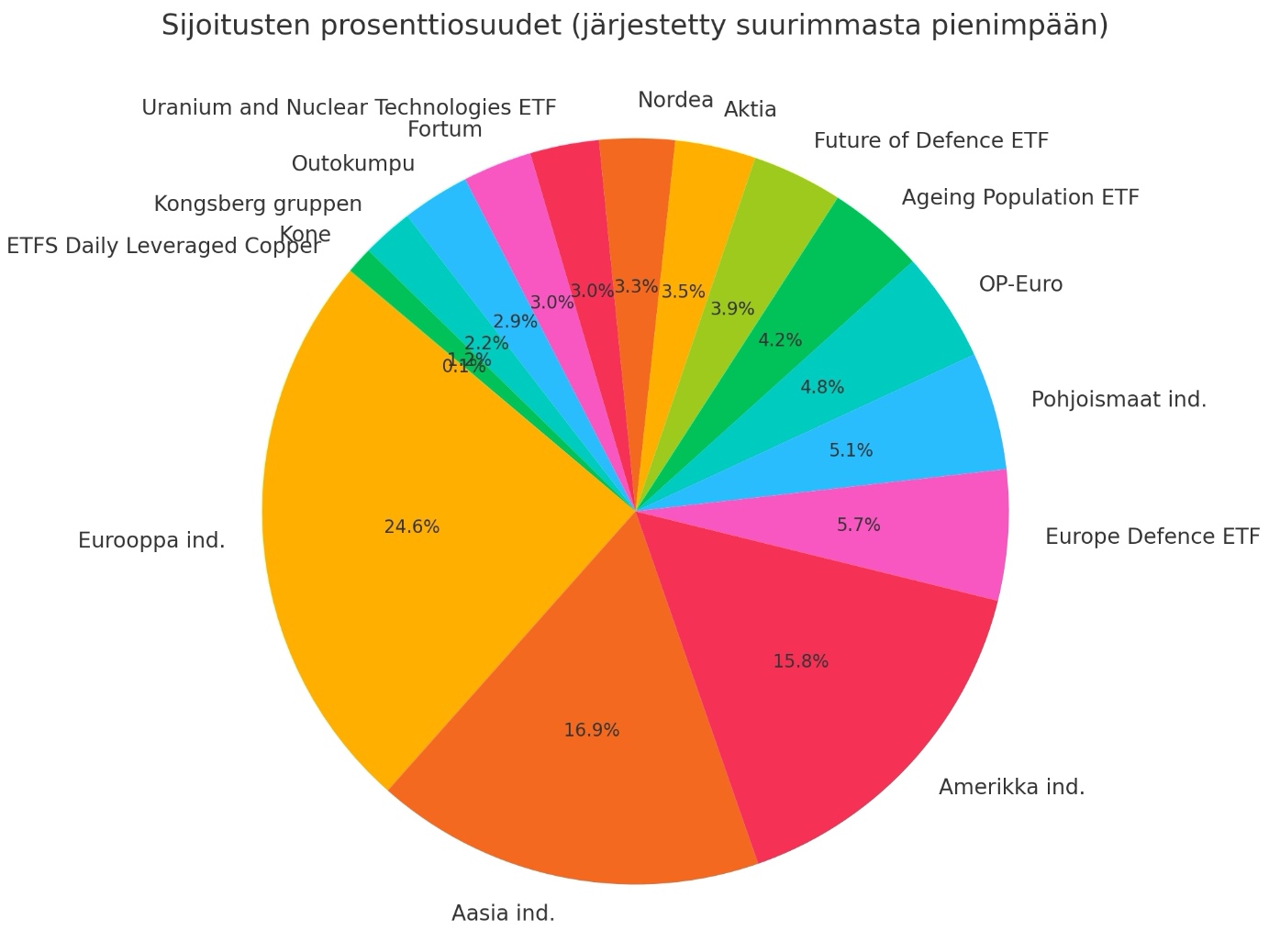

Europe heavily overweight! 49.3% of the portfolio.

14 Likes

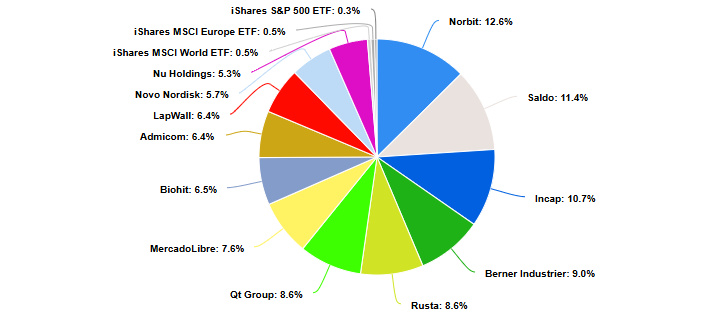

Portfolio review time! The latest from January, and again some small changes have occurred. I probably won’t bother with any grand poetry, but a few words per holding. I’ve written something in most of the company threads, so there’s probably no need to explain the business operations.

Norbit (12.6%) continues to be the largest holding in the portfolio. I’m head over heels in love with the stock (and its performance). It gives me '21 vibes and reminds me of Harvia, and soon we’ll probably be riding a white horse down a cliff without realizing we should lighten up. The valuation is, in my opinion, very tight due to recent rises, but I’ve also learned that you shouldn’t sell a rising stock (I lightened up around 150NOK and bought back later at a higher price). Let’s enjoy now, cry later. Norbit’s thread probably best explains why I’m involved as an investor.

Saldo (11.4%). Does this need explaining? I’m operating with an unusually large cash position, and yet YTD is hovering around 15-17%. I feel serene about this.

Incap (10.7%) has suffered from a few weaker years due to its largest customer reducing orders. Now, however, the direction may have changed, and orders from the European security sector could be a positive surprise. Incap, which generates good profitability in its sector and (hopefully) will achieve double-digit growth in the coming years, is a quality company with a quite reasonable valuation.

Berner (9.0%) has many thoughts about the company in its thread, but in short, jumping back into the M&A bandwagon was a very pleasant event in April. Although the stock is no longer incredibly cheap, it’s not expensive either (P/E 17x with this year’s forecasts).

With Rusta (8.6%), it happened that after initial enthusiasm, the excitement dried up. I perceive the company as a very defensive and safe holding, which isn’t significantly hit by consumers’ thinning wallets. The departure of the long-term CEO was an unpleasant surprise, but on the other hand, bringing in a new perspective might also be appropriate. The stock has practically been languishing for 18 months. I’ll probably watch an earnings report or two, and then make decisions about the holding.

Qt group (8.6%) valuation has plummeted from its golden age (21’ never forget). The sharp slowdown in growth is not pleasing, but I still believe the company has all the prerequisites for better performance. EV/EBIT is around 20x, which I don’t consider unreasonable. The profitability “hockey stick” should continue to materialize, so there’s potential for returns here.

MercadoLibre (7.6%) is the Amazon of Latin America! Practically a significant player in that region, doing pretty much everything. Valuation is tight, and one shouldn’t expect a boost from multiple expansion. The main thesis is long-term sustained growth and the company’s ability to constantly innovate and develop new businesses around its core. Somehow, companies like this appeal to me greatly, and currently, I’m actually researching a similar player…

Biohit (6.5%) is awaiting new geographical openings for its excellent product portfolio. The valuation is moderate, considering that there will certainly be continued demand for its products in cancer screening. TOP100 owners have been steadily adding recently. I could have more of this in my portfolio.

Admicom (6.4%) is probably one of the biggest sufferers due to the market situation. The product is presumably still in good shape and needed. When the market situation brightens and bankruptcies decrease, Admicom could get back on a stronger growth path. International growth should gradually start to materialize, as relying on a single market has been somewhat sluggish recently.

LapWall (6.4%) is also one of the sufferers of the market situation. When new construction isn’t happening, elements don’t move. The company has performed surprisingly well during the recent difficult times, and when the sun eventually rises, its market position is quite excellent. I really like the CEO and his communication style.

Novo Nordisk (5.7%) is the most recently built holding in the portfolio. I bought the first position when the bottom seemed to have been reached, and have since added twice. The company produces exactly what will be needed in the future: help for people’s overweight issues. I hope that the company’s obesity drugs wouldn’t sell, but that people would invest in their own health and watch what’s on their plate. Although obesity is not a choice, what one puts in their mouth is (I’m betting my money that a pill is easier than broccoli).

Nu Holdings (5.3%) provides banking services to those who don’t have them yet. And in LatAm countries, there are still many of them. Great track record, growth prospects, and a well-managed company. I would probably own more if some of its services didn’t overlap a bit with MercadoLibre.

ETF holdings (1.3%) diversifying across S&P500, global, and European indices. Gradually understanding my own mortality in stock picking, and as capital accumulates, some form of capital “protection” into slightly safer assets. Still a significant emphasis on stocks, but gradually over the years, a shift will occur. ![]()

So, here’s a review for now. I won’t write much about the business operations, as quality threads have been created for practically all my companies, where one can learn about the firm. I quite like the composition of my portfolio, and the high cash position has suited my mind quite nicely! Later, I’ll try to jot down a few words about the portfolio’s returns.

E.

52 Likes

Vuoden ensimmäisen salkkukatsauksen aika. Tähän mennessä vuotta voi pitää tapahtumarikkaana. Olin keväällä ihan luottavainen salkun sisällöstä yhtiöiden ollessa enimmäkseen laadukkaan puoleisia ja näkymien ollessa suotuisia.

Kuinka tilanne muuttuikaan kun selvisi, että Yhdysvaltojen vanha-uusi presidentti on vulgaarimpi ja fasistisempi kuin koskaan. Ensimmäinen herätys tuli Munichin kokouksen jäljestä Vancen pidettyä palopuheensa euroopan pilalla olevista arvoista.

Varmaan niitä ainoita hetkiä kun kauhun tunteista oli oikeasti hyötyä sijoittamisen kannalta sillä oli helppo samaistua eurooppalaiseen päättäjään kun Yhdysvaltojen varapresidentti toteaa, että suurin uhka ei ole rajojen ulkopuolella vaan sisäpuolella. Totuuden siemen siinäkin toki, mutta vertaat hidasta taantumista vs eksistentiaalista uhkaa toisiinsa - aivan eri asiat.

Lähdin seulomaan eurooppalaisia puolustusyhtiöitä kovalla tahdilla. Koska ukrainan sota on jatkunut jo jonkin aikaa oli vaikea löytää niin sanottuja “laggardeja”. Helpoin olisi toki ostaa sitä suurinta yhtiötä eli Rheinmetallia koska iso raha käyttää sitä treidin ilmaisuun ajoneuvona ja valuaatiolla ei ole niinkään merkitystä. Halusin kuitenkin turvamarginaalia enemmän joten päädyin työläämpään lähestymistapaan.

Päädyin lopulta ostamaan Exosensiä, Theonia sekä triplaamaan Alzchem position. Parhaimmillaan minulla oli yhtiötä 30 % salkusta. Hitusen myöhemmin ostin myös Ceotronicsin osaketta jonka näen seuraavan sektoria jäljessä. Lähinnä pienen koon sekä sijoittajaviestinnän vähyyden takia. Odottelen tilanteen korjaantuvan Q4-Q1 aikana kun Saksan armeija sekä muut eurooppalaiset armeijat alkavat todenteolla tekemään hankintoja.

Pelikenttä euroopassa jatkui muutostaan kun Saksan Merz ajoi velkajarrun ja fiskaalielvytyksen kiistanalaisella tavalla läpi. Tuolloin omistin kasan optioita sekä epälikvidejä saksalaisia teollisuusyhtiöitä sillä ajatuksella, että paketti on pakko saada läpi. Politiikasta ennestään kaukana pysyvänä oli todella kiinnostavaa seurata erilaisia näkökulmia asiasta.

Erityisen kiinnostavaa, toki subjektiivistä oli keskusteltuani Suomessa töitä tekevän Saksalaispariskunnan kanssa asiasta. He näkivät lähinnä taas yhden politiikon joka ei pidä lupauksiaan ja ottaa vastuuttomasti velkaa. Minä näin älykkään valtion johtajan joka ymmärtää talouspolitiikan päälle sekä pyrkii korjaamaan yli puoluerajojen Saksan rakenteellisia ongelmia.

Rauha ei kestänyt kauaa kun Trump päätti julkaista tullinsa. Aloin sulkemaan optioita aika nopeasti haistettuani palaneen käryä.

Olen ollut aina todella huono ottamaan kaiken irti dipeistä ja salkkuun jäi lovi suojien käytön takia. Tänäkin vuonna kynnän passiivisemman backtest salkun takana noin 15 % joka puhuu sen puolesta, että oma vahvuuteni on long puolella osakkeiden omistus eikä johdannaisten käyttö ainakaan huomattavissa määrin.

Hitusen salkun nykyisestä sisällöstä. Jossain määrin Trump on lahja sijoittajalle. Suuret muutokset Status quohon aiheuttavat myös uusia mahdollisuuksia. Salkku on helppo jakaa erilaisiin koreihin.

Euroopan puolustus sekä infra

Alzchem, Ceotronics, Vossloh ja Qbeyond tulevat suoraan hyötymään euroopan fiskaalielvytyksestä. Sen seurauksena pidän näitä ideoita suhteellisen matalariskisinä. Mm Ceotronicsia uskallan pitää suuressa painossa koska tiedän, että tilaukset kyllä tulevat. Lähinnä niiden kokoluokka ja ajoitus ovat se suurin kysymysmerkki. Olen erityisen innoissani Vosslohista riski/tuotto näkökulmasta, mutta siinä ei ole samanlaista skaalautuvuutta kuin Ceotronicsissa.

Metallit

Mkango, Taseko sekä Sandstorm. Länsi näyttää selvästi heränneen riippuvuuteen Kiinasta kriittisten metallien sekä magneettien suhteen. Valitsin Mkangon koska näen tuotannon kiistatta kannattavimpana sekä valuaation ollessa edullinen. Aika näytää ostinko oikeasti yhden suurimmista voittajista alalla vaiko spekulatiivisen pommin.

Sandstorm on ollut ehkä turhauttavimmista sijoituskohteistani tänä vuonna sillä osake treidasi vielä ennen tullipelleilyä todella huonosti ja tuotannon kanssa oli ongelmia. Kultaralli on kuitenkin auttanut tähänkin ongelmaan samalla kun näkökulmani kultaa kohtaan on muuttunut. Aijon pitää osakkeen painon ennallaan koska näen asenteiden muuttuneen dollaria kohtaan kevään aikana.

Trump jatkaa eri näkökulmasta, mutta samaan suuntaan kuin edeltäjänsä käyttämällä dollaria aseena. Myöskään alijaamien leikkaamisesta ei ole ole mitään merkkejä. Päinvastoin - enemmän vain. Eri rahastonhoitajat ovat alkaneet edellisinä kuukausina myös valittelemaan velkamassan kestämättömyyttä. Samalla velkamarkkinat ovat alkaneet osoittamaan mieltään selvien talouspoliittisten virheiden ( tullit ) edessä. En tiedä milloin velkakirjamarkkinat alkavat oikeasti taistelemaan vastaan vai onko vastaus dollarin devalvoituminen. Jokatapauksessa kulta on mielestän hyvä suoja tuota skenaariota vastaan. Lyhyellä aikavälillä olen huolestunut kullan momentumista. Se nousi säälittävät 2 % Iraniin hyökkäyksen johdosta samalla kun öljy oli 15 % nousussa. Mainitsemani rakenteelliset tekijä ovat kuitenkin taustalla ennallaan.

Tasekosta ei enempää. Avasin keissiä senverta paljon ketjussa.

Muuta

Ensivuonna tapahtuu jotain mikä saa edellisten vuosienkin mullistukset näyttämään pieneltä. Grand theft auto 6 julkaistaan. Pelaamiseen liittyvät lisälaitevalmistajat kohtasivat koronan jälkeen aikamoisen krapulan kun kaikki päivittivät setuppejaan. Siitä on kuitenkin jo viitisen vuotta ja olisi jo aika päivittää laitteistoa. pelkästään laitteiden käyttöikä alkaa tulemaan vähitellen vastaan. ostin muunmuassa itse juuri uuden hiiren vaikka pyrinkin käyttämään laitteet siihen asti, että ne eivät enää toimi kunnolla.

Ohjaimet, kuulokkeet yms ovat syklinen ala ei pelkästään kuluttajien ostovoiman vaihteluiden takia vaan koska ostopäätökset seuraavat uusien konsoleiden ja merkittävien pelien julkaisua. Niinpä sektorilla saattaa olla edessään todella kova käänne uuden Nintendo konsolin, mutta myös GTA 6:n julkaisun lähestyessä.

Turtle beach on siitä hyvä kohde, että johto on todistanut kykynsä pääoman allokoinnin suhteen. Tekivät muunmuassa edullisen yritysjärjestelyn noin vuosi sitten sekä ovat ostaneet omia osakkeita pois. Yrityksellä on tällä hetkellä käynnissä osakkeiden osto-ohjelma joka kattaa 30 % yrityksen markkina-arvosta. Ihan hieno asia tehdä varsinkin jos sykli on kääntymässä.

Lyhyellä aikavälillä päänvaivaa tuottaa kuluttajien käytös, mutta myös kauppasota. Yrityksen johto hoiti hommat sen suhteen mallikkaasti, että ostivat varastot täyteen ennen tulleja sekä siirsivät valmistuksen lähestulkoon kokonaan Kiinasta Vietnamiin. Kysymyksiä kuitenkin herättävät edelleen se kuinka tullineuvottelut Vietnamin kanssa menevät ja paljonko tuotannosta on todellisuudessa paikallista ja paljonko tulee todellisuudessa Kiinasta.

Öljy ja Mattr

Alokkaan haastattelussa puhuin mahdollisesta hyökkäyksestä Iraniin. Se toteutuikin yllättävällä voimalla ja täytyy myöntää, että sössin keissiin valmistautumisen pahan kerran. Näin jälkikäteen näen, että olisi pitänyt tehdä enemmän taustatyötä jolloin alhaalla roikkuvia omenia olisi ollut helppo poimia. Minun olisi pitänyt löytää tämä yhtiö:

Nyt olen jokseenkin epämukavassa tilaneessa koska nyt pitäisi alkaa lyömään vetoa epätodennäköisemmistä skenaarioista. Jos Iranissa tapahtuu vallanvaihto se aiheuttaa varmasti sisäisiä levottomuuksia ja öljyn tuotanto laskee. Se seurauksena öljyn hinta tietenkin nousee.

Kysymys kuuluu kannattako tuohonkaan edes luottaa sillä Opecilla näyttää olevan varakapasiteettiä vaikka kuinka. Olen kuullut edelliset neljä vuotta samaa tarinaa siitä kuinka Opecilla ei ole todellisuudessa kapasiteettiä ja alalle ei olla investoitu tarpeeksi. Silti öljyn hinnat ovat olleet erittäin matalat inflaatioon nähden kaikki nämä vuodet.

Toinen vielä epätodennäköisempi keissi olisi se, että Hormuzin salmi suljettaisiin. Se tarkoittaisi, että tilanne olisi eskaloitunut.

Aikani treidailtuani kahden välillä ja tuhottuani vähän pääomaa päätin, että lyön jälkimmäisestä keissistä vetoa. Miksi? Koska molemmat skenaariot ovat binäärisiä paras tapa on mielestäni käyttää optioita. Tuotannon lasku skenaariossa saadakseni huomattavan tuoton minun pitää ostaa optioita reilun 2 % painolla salkusta. Saatan herätä aamusta huomatakseni, että Trump on alkanut neuvottelemaan ja option arvo on puolittunut. Kuitenkin koska jälkimmäinen skenaario on epätodennäköisempi kertoimet ovat myös korkeat.

Saan saman nimellisen tuoton riskeeraamalla vain 0,2 % salkusta. Kun toinen skenaario on 10:100 ja toinen 1:100 ei ole niin merkitystä kumman valitsee.

Mattr saattaa saada tästä pientä lisäapua sillä yhtiön liiketoiminnasta kolmannes liittyy pohjois-amerikan öljyn tuotannon tasoon. Todennäköisesti kyseinen segmentti on pohjannut sillä öljy tulee pitämään kevyttä riskipreemiota jatkossa sekä yhtiö laajentaa ensivuonna tuotetarjontaansa minkä pitäisi tukea segmenttiä.

Tähän liittyen yhtiö antoi myös optimistisen näkökulman ensivuodelle The 15th Annual East Coast IDEAS Conferencenssa viikko takaperin. Kuulemma tulleilla on vain vain rajallinen vaikutus tämän vuoden tulokseen ja asiakkaat segmentistä riippuen ovat optimistisia. Yhtiö uskoo pääsevänsä -26 lähelle tavoitteitaan marginaaleissa sekä liikevaihdossa. Se tarkoittaisi, että ensivuoden arvostus olisi P/FCF 4-6. Järjettömän halpaa jos yhtiö suorittaa.

Humanoidirobootit

Kuuntelin jokin aika sitten podkastin joka esitti realistisen keissin humanoidirobooteista.

Kaikessa hiljaisuudessa roboottien kehitys on edennyt yllättävän pitkälle. Kuulen tässä pientä vuoden -23 AI teeman kaikua. Yllättäen roboottien suurin kuluerä ovat nivelet yms ja näiden valmistajat ovat autoalan arvoketjussa. Niinpä edessä saattaa olla se, että edelliset vuodet paineessa ollut ala saattaa kohdata rakenteellisen muutoksen.

Niinkuin raportissa mainitaan alalla alkoi muutenkin olemaan jo käänteen merkkejä. Arvostukset ovat kaikilla yhtiöillä syklisille ominaisesti koholla. Seulottuani osakkeita läpi halvimpia olivat Infinion, Onsemi sekä Allient. Olen Allientista kiinostunut varsinkin koska johto vaikutti puhelussa luotettavalta sekä osake on edullinen.

Tähän mennessä vuotta salkku on tuottanut ytd +28. Haluaisin päästä tänävuonna reiluun 40 % prosenttiin. Saa nähdä mikä on lopputulos.

56 Likes

France

Airbus SE

OSE Immunotherapeutics SA

Peugeot Invest Société anonyme

Netherlands

Akzo Nobel N.V.

BE Semiconductor Industries N.V.

Fugro N.V.

Canada

Altius Minerals Corporation

Amerigo Resources Ltd.

ARC Resources Ltd.

Dynacor Group Inc.

McCoy Global Inc.

Methanex Corporation

Orezone Gold Corporation

Pembina Pipeline Corporation

Suncor Energy Inc.

USA

Amazon.com, Inc.

Finland

Atria Oyj

Kemira Oyj

Sweden

Concejo AB (publ)

Softronic AB (publ)

Germany

Deutsche Beteiligungs AG

Francotyp-Postalia Holding AG

Henkel AG & Co. KGaA

Kontron AG

M1 Kliniken AG

TUI AG

Italy

Italian Wine Brands S.p.A.

Stellantis N.V.

Denmark

Novo Nordisk A/S

Portugal

Semapa - Sociedade de Investimento e Gestão, SGPS, S.A.

Belgium

Sofina Société Anonyme

Spain

Tubos Reunidos, S.A.

Here is my current portfolio regarding direct stock investments. In addition to this, I also have ETF funds, but I’m not really sure what to do with them. It’s possible that I will build this investment portfolio into one purely focused on value stocks.

Each company has its own target price already set, and when it’s met, I sell. Then I invest the money + profit from the sale into a new investment, and off we go again. There are a total of 32 companies currently.

13 Likes

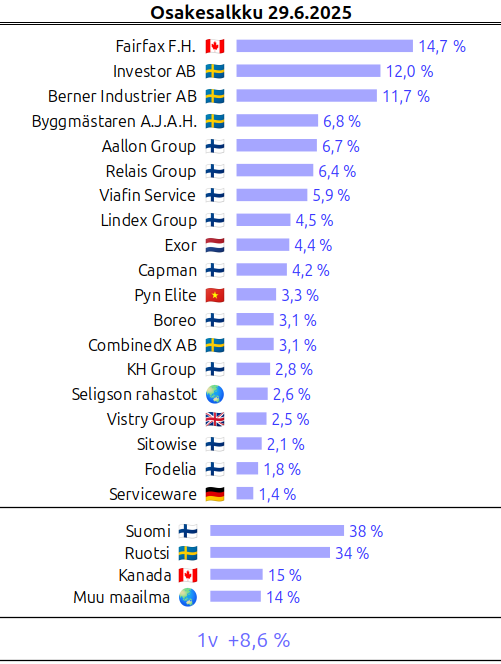

Portfolio Review 25H1: Excellent Start to the Year

The investment year has progressed well so far, despite a lot of political turmoil and fluctuation. Nordnet’s YTD shows +14.2%.

Sales from the portfolio: Neste, Berkshire, Markel

Purchases: Exor (new), Fairfax (addition), Investor (addition), Byggmästare (addition), Boreo (addition), Relais (addition)

In Neste’s case, I decided to invest the funds elsewhere. Berkshire and Markel, on the other hand, are excellent companies. Due to political uncertainty, the dollar’s decline, and high valuations, I decided to divest all US investments, i.e., the aforementioned companies. I bought Exor as a new addition to the portfolio. Exor’s automotive business is currently suffering somewhat from Trump’s tariff decisions. Let’s see where the tariffs eventually settle. Exor’s NAV discount is significant, around 50% at the time of my share purchase. The company sold Ferrari shares worth 3 billion and bought back its own shares for one billion, which corresponded to 5.5% of the share capital. 2 billion is still available for investment, for which the company is looking for a new investment target.

I made small additions to Investor, Fairfax, Byggmästare, and Relais because I thought the shares were cheap. If Relais isn’t at rock-bottom prices, it’s at least affordable when looking at the valuation after the pending acquisitions are completed. Debt has accumulated a bit more due to the acquisitions. In investments, low indebtedness is always more comfortable than high. In Relais’s case, the situation is understandable, as the business is based on continuous acquisitions, and the latest purchase is not small. Due to the low valuation of the stock, it is not attractive to use a lot of its own shares to finance the deals. Byggmästare’s investment company discount was over 20%, and I thought it was a very attractive opportunity to buy more. Byggmästare received a significant amount of cash when selling part of its largest investment (Safe Life) to another investor. Now there is a lot of money to put into new investments. So, a somewhat similar situation to Exor. Boreo’s situation has also improved, and the company’s earning power is recovering, which justified a moderate addition to myself.

Diversification ideas have changed during the spring. New investments are currently largely going to Europe or Canada. The USA is not a must for me in this situation. Valuations are high. Previously, one was willing to pay for a stable and efficiently operating investment market. Now the situation has changed for the worse. In Europe and Finland, the valuations of several companies are attractive, and there’s no need to bear dollar risk either. I don’t have new investments in sight, but I might make small additions if shares fall again at some point.

e: Neste removed from portfolio graph

56 Likes

With those returns, one would probably dare to put the portfolio on Shareville too. Surprisingly few dare to ![]()

Banks and insurance companies have also performed well this year, but I don’t have them in my portfolio. So, I’ve underperformed YTD once again. Many older investors probably have traumas from them from back in the day (1992), and the fact is that their balance sheets are difficult to read. In the US, they also collapsed in 2008.

Indeed, I don’t have any of the same stocks as the previous ones. It’s interesting how people’s brains end up with completely different stocks. Among my top 6 investments (all from Shareville), as many as four are the same as in Inderes’ model portfolio. Given the recent returns of the model portfolio, it’s perhaps not surprising that no one would want to advertise owning them. I have still tried to include both clear value stocks and growth companies in my portfolio; they work well perhaps at slightly different times. Nokian Renkaat and Rapala have a very low P/B. Tietoevry is a value stock that also has a growth option in software, while QT Group (though not in the top 6) is probably the most convincing growth company in light of recent years’ figures, even though its share price has fallen.

US small cap value ETFs don’t feel expensive at all, perhaps on par with Finland. The stocks that are talked about the most are then expensive in terms of figures. However, that doesn’t tell you anything about where you should invest. Stocks are a strange hobby (compare it to tennis, for example); the time spent doesn’t necessarily correlate with skill at all. A complete amateur who bought Apple 15 years ago because they liked their Apple phone has beaten most professionals, or probably all of them ![]()

14 Likes

A quick 2025 Q2 portfolio update would be timely again, even though the US stock market is still open for a couple of hours.

Evolution gaming 9.9 %

Qt 5.5 %

Puuilo 5.5 %

Svenska Handelsbanken 5.5 %

Revenio 5.3 %

Talenom 4.9 %

Sampo 3.6 %

Tractor Supply 3.6 %

Harvia 3.5 %

Gofore 3.2%

Atlas Copco 2.5%

Nokian Renkaat 2.5 %

Sandvik 2.5 %

Tieto 2.3 %

Berkshire Hathaway 1.3 %

Fastenal 1.0 %

Vaisala 0.7%

ADP 0.4 %

Graco 0.3 %

Nordea 0.3 %

Cash/fixed income investments 12.2%.

Funds and ETFs (Seligson, Pyn Elite, Splitan, EUNL, EUNK, IUSN, Seligson & Co OMX Helsinki 25, XACT Norden) 21.3%

New investments in portfolio: XACT Norden

Additions: Atlas Copco, Sandvik, Qt, Evolution

Sold: -

Reductions: -

Short-term trades: -

The portfolio’s cash/fixed income position has slightly decreased during the quarter to 12.2%. The intention is to gradually put more cash to work. One new investment, XACT Norden, entered my portfolio during the quarter. The idea for this new ETF came to mind when I was following Novo Nordisk’s recent development and its share price drop. I didn’t want to invest in it directly, but the thought occurred to me that I could invest in it through a new ETF suitable for my portfolio. Novo Nordisk’s share in XACT Norden’s portfolio is 12.55%. I added Atlas Copco and Qt to my portfolio in several tranches. I also picked up a bit of Sandvik from the April dip. Evolution’s share price dropped enough that I decided to catch the falling knife one more time.

The theme for the rest of the year in the portfolio will continue to be the gradual increase in the share of ETFs and funds. At this rate, their share in my portfolio would be approximately 24% at the turn of the year. I will continue with the same theme next year as well.

I am currently monitoring the development of 3-5 companies a bit more closely. Not all of them will necessarily still be in my portfolio a year from now when I write the next portfolio update. However, I am not in any great hurry with them. The appearance of new positions, on the other hand, is not as likely, as my goal is to reduce the number of direct investments in my portfolio. Of course, if share prices in the USA drop a bit more, quality company/companies might find their way into my portfolio.

Let’s also note here that the median P/B 2025 for Finnish companies followed by Inderes, calculated from Inderes’ website, is 1.75 (P/B 2026 median 1.66). Inderes has 16 buy recommendations and 7 sell recommendations. CNN’s Fear & Greed index was 65 (Greed) at the turn of the quarter.

18 Likes

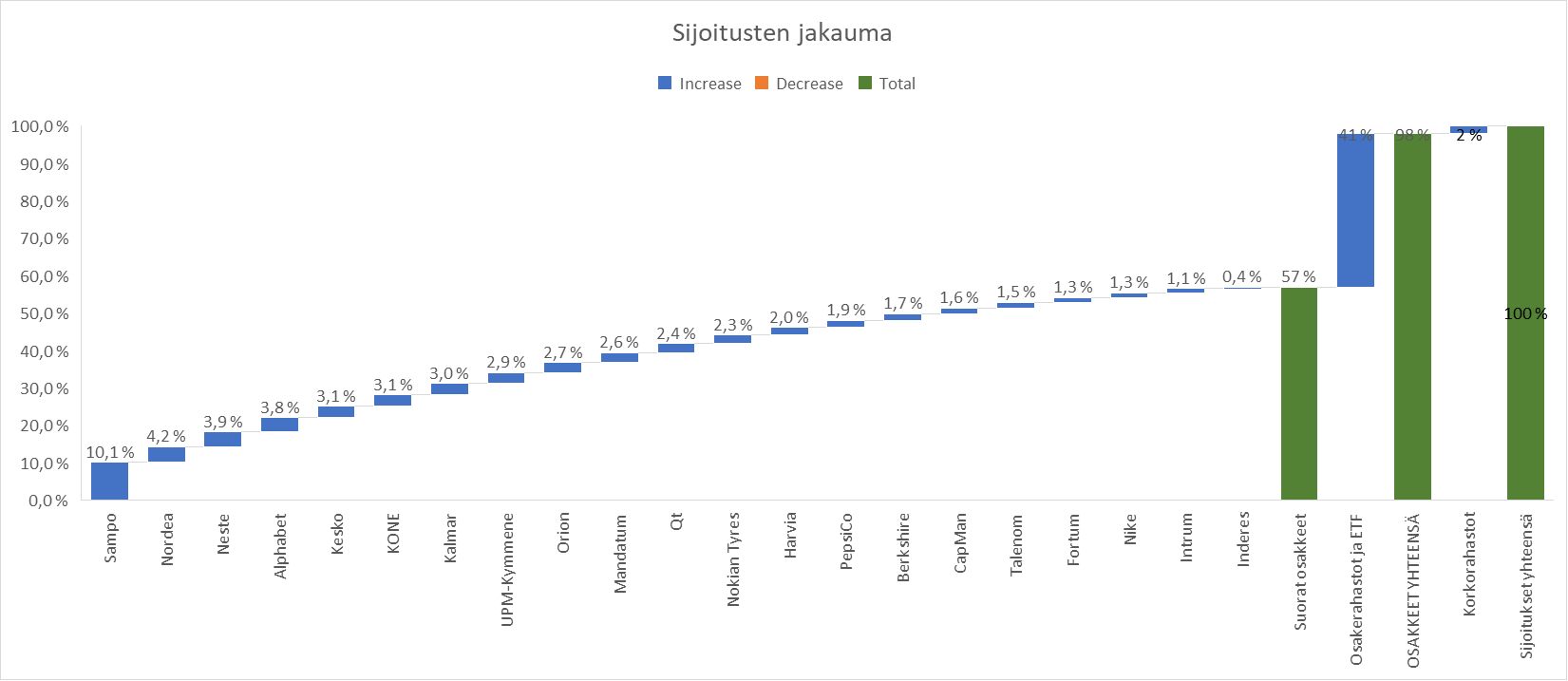

Portfolio Review H1 2025

During the beginning of the year, many purchases have been made, especially in the Finnish stock market, but also in the US. Fund and ETF purchases have also continued as usual monthly + a few extra purchases when the market dipped in April. I reduced bond funds and shifted weighting to stocks.

New to the portfolio:

- QT, Pepsico, Nike

Additions:

- Alphabet, Nokian Tyres, UPM, Kalmar, Talenom, Capman, Neste, Inderes

Reductions:

- Kesko and bond funds

Return has been approx. +9.5% in the beginning of the year.

A personal annual record has been broken in received dividends, and a few more dividends are coming during H2.

During H1, the Private Banking doors also opened at Nordnet.

24 Likes

| Company | Share |

|---|---|

| Fairfax Financial | 41.4 % |

| Linamar | 11.4 % |

| International General Insurance | 7.9 % |

| AerCap | 4.9 % |

| Investor B | 1.6 % |

| - | - |

| Canadian oil companies | 6.8 % |

| Nicotine companies | 6.6 % |

| - | - |

| Cash | 19.5 % |

| Total | 100.0 % |

YTD +2.88 %

Q2/2025 was a different kind of quarter. I spent by far the least amount of time on stock picking and pondering it in years – simultaneously both an excellent and a terrible quarter for such a change. It’s a minor miracle that with this much effort and decision-making, we managed to end the quarter in the black, but the age of miracles is not over yet.

Sales, Q2:

Last year, I implemented strict stop losses as part of my investment strategy. Well, as a result, the portfolio experienced an absolute hellish storm when Trump started to stir things up – almost all newer positions (Exor, NewtekOne, a few additions made to AOT in the spring) hit their stop-losses. In addition, in the same turmoil, I manually sold off some companies (Secure, Valeura). Why? The reasoning I wrote in a private conversation at the beginning of April is shown in the quote below.

I left the first group of my previous portfolio allocation in the portfolio (Fairfax-IGIC-PMI-Investor), and sold everything else. […] now, from a sleep-policy perspective, the only right option was to sell everything that wouldn’t withstand time and Trump excellently. Was it an optimal move? Hell no. Did it feel like the right move? Yes.

I already knew then that perhaps I shouldn’t have made the sales. But in the investment strategy – as erratic as it has been – it is unequivocally stated that if stock positions disproportionately affect daily life, relationships, or mood, then the stock weighting should be reduced, regardless of whether returns are achievable in some corner of the market. It’s all the same: I wasn’t going to sleep poorly because of oil company stock prices.

Brief comments on portfolio companies:

Fairfax: Q1 was a strong defensive victory even after the California fires. Operational performance remains at a high level, and I added to the stock a couple of times on dips. The position size is starting to be comical, but when the company’s performance and share price development are of this magnitude, let it grow. It is no longer blatantly undervalued, but the long-term value creation components are so well in place that there is no reason to start selling yet. Including dividends, my initial purchases have approximately quadrupled in three years.

Linamar: One solid success also occurred on the buying side when I managed to fish Linamar back into the portfolio almost from the bottom. In Q1, operations were in slowing markets, which varied from soft to utter destruction depending on the segment, but the company defended its profitability and ended up growing its earnings compared to a year ago. Looking at the Industrial segment’s figures, it’s hard to understand how this company can trade at the cost of fixed equity and 6x this year’s earnings estimates.

I’ve said this before, but I see similarities here with Fairfax’s investment story – an unpopular company, profitability under pressure, a long-term approach, an aim to expand business into different sectors. And when the initial valuation is this low (from my purchases P/E 5, P/B 0.55), the position is deservedly larger. The company’s buybacks have been on hold, which is a big change compared to the brisk pace at the beginning of the year – hopefully, this foreshadows acquisitions, as the balance sheet is strong and there would be enough liquidity for acquisitions that develop the investment story. If the development continues to be promising, the position will grow significantly from its current level.

IGIC: Q1 was slightly soft due to increased catastrophe losses, but almost every company in the sector reported that story. That’s the main thing. The stock price has remained stable, I added a little to the stock from current levels. P/E 9, huge net cash, capital returned – no problems.

AerCap: During the quarter, the British court ordered AerCap to be paid a billion dollars in insurance compensation for equipment lost in Russia in 2022. That gives the company more firepower for buybacks. Otherwise, nothing particularly new to say about the company. Still the best in its field, still cheap, still superbly managed.

Investor AB: This is still in the portfolio. Nothing more to say about it.

Then, different reporting.

Nicotine companies: Philip Morris got a friend in its portfolio – surprise, surprise – BTI, as I wanted to increase exposure to nicotine pouches. The company had previously been in the portfolio with good success – hopefully, round number two goes just as well. BTI’s valuation is deservedly about half of PMI’s due to its product portfolio, but a 10 percent free cash flow yield is a rather cheap price tag for Velo and the company’s other pricing-power brands. Dividend people should also like it.

Since there are unlikely to be huge changes in the investment thesis for either company, I will write about them together in the future. I have also been researching a third company in the sector, which will join the group later – if it is to join. Perhaps more on that someday.

Canadian oil companies: Canada’s well-managed, long-term, and lowly valued energy companies will be found here in the future (Valeura, Strathcona, IPCO). There are plenty of affordable names available in the sector, so owning just one name is not necessarily the most sensible solution. Free cash flow yields are at best around 15-20 percent, and even for higher-quality companies, we are talking about double-digit figures – not a bad deal in the current market, even if commodity prices fluctuate.

By the way, selling IPCO last year has proven to be a mistake, but fortunately, Valeura’s strong performance before April somewhat compensated for the damages.

At the beginning of the year, I expressed a cautious wish for about 5-10 percent positive development for this year. That can still be achieved quite well, but it’s no secret that the year could have gone better. However, I don’t know if anything other than a faster recovery from the April turmoil could have been achieved with this effort – who knows.

Valuation levels in the market are sky-high, but fortunately, they are still very moderate in my own portfolio (weighted 2025e P/E approx. 10.4). If I owned hype companies, I would be watching the situation with excitement, but fortunately, I don’t have to. ![]()

Let’s revisit this in September – hopefully with profitable results.

34 Likes

After years, another portfolio update here; here’s the situation this morning, July 1st.

Over the past year, I’ve finally bought stocks from the big US, which has proven to be an absolutely excellent decision. Previously, I already made good profits with HIMS, and although the timing of the sale was frankly terrible, that money has been successfully put to work in AMD, SoFi, and Evolution. Among fintech firms, NU also ended up in the portfolio with a relatively small weighting earlier, and together with SoFi, I had thought of these as an “ETF” since I couldn’t choose between the two.

Among companies from our western neighbor, I still have strong confidence in Verve, even though a small reduction was made in the spring. Further west, Magnora and Elliptic Labs have, frankly, been somewhat of forum speculations, whose business I understand too little about, but then again, the weightings aren’t very large either.

Among Finnish companies, I could mention NoHo, whose performance seems to be consistently good, even though it hasn’t been reflected in a rocket-like surge in its stock price. Is it a good investment or not? I don’t know. My thoughts on LapWall are very similar.

The portfolio is quite small, just over €40,000 right now, and returns from recent years (3-5 years) would certainly have been better with index investing. OP’s return curves are what they are, but intuitively, the development over the last year has been clearly better than before, and as a hobby and a tool for self-development, this is truly unparalleled activity.

Thanks to the forum and happy summer to all!

25 Likes

Salkun edellisestä päivityksestä on reilu puoli vuotta joten huvikseni hakkasin exceliin taas päivitetyn salkkukatsauksen. Salkun sisältö näyttää tällä hetkellä tältä, suuruusjärjestyksessä:

| Osake | Osuus salkusta | Tuotto |

|---|---|---|

| Handelsbanken USA Index | 27,1 % | 48,7 % |

| Hims & Hers Health Inc A | 8,1 % | 98,4 % |

| Games Workshop Group | 4,5 % | 10,7 % |

| Harvia Oyj | 3,9 % | 69,8 % |

| Puuilo Oyj | 3,2 % | 58,6 % |

| Texas Roadhouse | 3,2 % | -3,5 % |

| Applied Materials | 3,1 % | 9,1 % |

| Vaisala Oyj A | 3,0 % | 8,6 % |

| Qt Group Oyj | 2,9 % | -15,9 % |

| Olvi Oyj A | 2,9 % | 8,6 % |

| Revenio Group Oyj | 2,8 % | 4,0 % |

| Remedy Entertainment Oyj | 2,8 % | -18,8 % |

| ASML Holding | 2,7 % | 4,9 % |

| Mettler-Toledo International | 2,6 % | -19,3 % |

| Paradox Interactive | 2,5 % | 8,7 % |

| LapWall Oyj | 2,5 % | 6,5 % |

| Marimekko Oyj | 2,4 % | 16,8 % |

| Visa | 2,4 % | 10,9 % |

| S&P Global | 2,4 % | -8,8 % |

| Uber Technologies Inc | 2,3 % | 26,5 % |

| eQ Oyj | 2,2 % | -27,6 % |

| Evolution | 2,0 % | -6,5 % |

| Titanium Oyj | 1,9 % | -43,3 % |

| MSCI | 1,9 % | -9,5 % |

| Applied Nutrition | 1,7 % | 1,7 % |

| Medpace Holdings Inc | 1,1 % | -4,0 % |

| Canatu Oyj A | 0,7 % | -13,4 % |

| Betsson B | 0,5 % | 25,8 % |

| Nordnet | 0,4 % | 0,0 % |

| Käteinen | 0,2 % |

Erittäin vahvalla kasvu- ja laatukulmalla mennään edelleenkin. Salkun YTD on noin 5% mikä on mielestäni hyvä tilanne koska vertailuindeksini (iShares Core S&P 500 ETF USD Acc eli SXR8) on tuottanut vuoden alusta -6.8%, ja iso osa sijoituksista on dollarimääräisissä arvopapereissa, joka on aiheuttanut tänä vuonna melko ikävää vastatuulta salkun tuottoihin. Käteistä minulla on oikeasti noin 11%, mutta tämä on puskurirahastossa odottamassa “pahaa päivää” enkä sitä aio osakkeisiin sijoittaa joten jätin sen tämän salkkukatsauksen ulkopuolelle.

Suoria osakkeita on tällä hetkellä 28. Edelliseen katsaukseen verrattuna salkusta on poistuneet seuraavat osakkeet:

- Admicom

- Orthex

- F-Secure

- Nike

- Fenix Outdoor

- Björn Borg

Orthex, F-Secure ja Admicom poistuivat epävarmojen kasvunäkymien takia salkusta kun yritin siivota mielestäni “heikoimpia” yrityksiä pois. Samoin Nike, Fenix Outdoor ja Björn Borg poistuivat myös osittain samasta syystä, osittain siksi että pitkällisen pohdinnan jälkeen tulin siihen lopputulokseen että brändiarvo on mielestäni yksi huonoimpia vallihautoja yrityksellä. Esimerkiksi verkostovaikutukset tai vaihtamisen vaikeus (sulautetut järjestelmät tai vastaavat) ovat mielestäni paljon vahvempia vallihautoja, joten olen yrittänyt panostaa tämän tyyppisiin yrityksiin. Myöskin lähtökohtaisesti pidän esimerkiksi datapalveluita houkuttelevampana liiketoimintana kuin “tavaran myymistä”, vaatekauppiaan pitää liikevaihtoa kasvattaakseen myydä enemmän krääsää mutta datapalveluntarjoajan ei. Marimekon kuitenkin vielä jätin salkkuun, osittain koska se on hyvä kotimainen yritys, osittain koska uskon sen liiketoiminnan olevan hieman paremmalla pohjalla kuin esimerkiksi Niken.

Uusina salkkuun on tullut seuraavat osakkeet:

- ASML Holding

- Applied Materials

- Evolution

- Applied Nutrition

- Medpace Holdings (seurantapositio)

- Canatu Oyj (seurantapositio)

- Betsson B (seurantapositio)

- Nordnet (seurantapositio)

Jotenkin onnistun löytämään aina kiinnostavaa ostettavaa sitä mukaa kun päätän luopua osakkeista. Tässä muutamia ajatuksia uusista riveistä:

Aloin tutustumaan Canatuun, joka johti minut sitten tutustumaan siruteollisuuteen. Uskon että siruteollisuudella on hyvä tulevaisuus ja kasvava kysyntä. Tekoäly ja toisaalta kaikkiin elektronisiin laitteisiin tulevat erilaiset sulautetut järjestelmät varmasti ajavat siruteollisuuden kysyntää ylöspäin. Jonkin aikaa tutkittuani eri firmoja alalta löysin mielestäni 2 salkkuuni sopivaa firmaa, joilla on vahvat kilpailuedut ja mielestäni siedettävä arvostustaso ja tätä kautta päädyin ostamaan ASML ja Applied Materialsia.

Applied Nutrition on vähemmän tunnettu, pieni Brittiläinen lisäravinteiden valmistaja joka listautui viime vuoden loppupuolella. Uskon että vaikka lisäravinnepuoli on todella kilpailtu ala niin sen alla oleva markkina tulee kasvamaan vuosia eteenpäin, ja tälläinen pieni ja ketterä toimija jolla on hyvä historiallinen kasvu ja kannattavuus on mielestäni ihan potentiaalinen sijoitus. Jos tämä herätti mielenkiintoa niin kannattaa lukea seuraava kirjoitus, jossa Pentti Jokinen käy mielestäni ihan hyvin yhtiötä läpi: Applied Nutrition - Kasvuhakuinen lisäravinnebrändi Briteistä | Sijoitustieto.fi

Evolution ja Betsson tuli salkkuun koska halusin päästä mukaan uhkapeliteollisuuteen, jonka uskon olevan hyvin kasvava markkina myös tulevaisuudessa. Evolutionilla on ollut lähihistoriassa ongelmia, mutta uskon niiden olevan väliaikaisia ja siksi ostin isomman siivun 800 SEK tienoilla. Betsson ja Nordnet tulivat ihan pienenä siivuna salkkuun koska ne eivät ole mielestäni olleet erityisen houkuttelevan hintaisia, joten odotan parempaa ostopaikkaa tai kasvatan pikkuhiljaa ajallisesti hajauttaen positiota. Medpace:n kanssa myös sama tilanne, vaikka osaketta onkin viime aikoina mielestäni saanut halvalla niin ajattelin silti aloittaa pienellä siivulla ja seurailla rauhassa, varsinkin kun liiketoiminta näyttää pieniä heikkouksia.

Salkun koostumukseen ja rivien määrään olen tällä hetkellä ihan tyytyväinen. Vaikka uusia rivejä on tullut niin nämä on pääasiassa rahoitettu uudella rahalla, jota en ole kauheasti edes salkkuun lisännyt koska puskurirahastoni tarvitsi täydennystä. Myynneistä tulleet rahat olen yrittänyt kohdistaa salkun “voittajiin” eli vanhoihin omistuksiin joilla liiketoiminta (ja osakekurssi) on mennyt oikeaan suuntaan (Hims, Games Workshop, Harvia, Vaisala, Puuilo jne). Salkun “häviäjiin” tai “putoaviin puukkoihin”, kuten Remedy, Titanium ja eQ, tottakai houkuttelee lisäillä rahaa arvostuksen puolesta, mutta noihin positoihin en tule lisäämään kuin korkeintaan pieniä summia ennen kuin liiketoiminta kääntyy niissä oikeaan suuntaan ja tulos takaisin kasvu-uralle.

Laskin nopeasti että puolessa vuodessa olen myynyt salkusta 12% kokonaisuudesta, eli tuosta laskettuna salkun vuosittainen “churn rate” on noin 24% eli näin laskettuna keskimääräinen pitoaika on 4 vuotta, johon olen sinällään ihan tyytyväinen ottaen huomioon kuinka tapahtumarikas alkuvuosi on ollut markkinalla. Tariffipaniikissa en oikeastaan mitään myynyt, ja uskon että seuraavan puolen vuoden aikana salkussa on myyntien osalta hiljaisempaa muutenkin.

Tässä vielä muutamia ajatuksia joistakin omistamistani osakkeista:

Hims on päässyt kasvamaan muihin osakkeisiin nähden melkoiseen ylipainoon, mutta toisaalta pidän sitä yhtenä salkkuni potentiaalisimmista osakkeista. Vahva kannattavuus ja kasvu, valtava kokonaismarkkina. Tariffidipisissä lisäsin pariinkiin otteeseen osaketta, kerran noin 33$ tienoilla ja kerran noin 26$ tienoilla. Vaikka aina välillä tekisikin kurssinousujen jälkeen mieli kevennellä niin olen päättänyt että annan voittajien juosta niin kauan kuin niiden liiketoiminta menee oikeaan suuntaan ja uskon firman tulevaisuuteen. Vähän kiristynyt arvostus ei ole mielestäni syy myydä osaketta. Mikäli arvostus karkaa jollekkin aivan järjettömälle tasolle (luokkaa P/S 100) niin sitten alan harkitsemaan osakkeen myyntiä arvostuksen perusteella. Ei niitä 10-bäggereitä tai 100-bäggereitä saa muuten salkkuun kuin istumalla voittajien päällä.

Erityismaininta myös Games Workshopille, jonka liiketoiminta on viimeisen vuoden aikana puksuttanut erinomaisesti eteenpäin. Myös tulevaisuus näyttää hyvältä, kysyntä ylittää tarjonnan ja uusi tehdas valmistumassa mahdollisesti ensi vuonna. Astartes 2 ja Henry Cavillin tekemät sarjat tulevat varmasti tuomaan Warhammerille paljon huomiota, ja vaikka melkoisesta nichestä onkin kyse niin en usko että tämä firma on vielä lähellekään sitä pistettä, jolloin se ei pysty saamaan uusia faneja Warhammerille.

Helsingin pörssin yksi mielenkiintoisimpia tarinoita lähivuosilta on kyllä Puuilo. Tämä firma on hauska esimerkki siitä että tehdäkseen hyvää kasvua ja kannattavuutta, yrityksen ei tarvitse ratsastaa huipputeknologian tai tekoälyn aallonharjalla. Riittää kun on hyvin mietitty konsepti, tunnetaan oma asiakaskunta, ja jalkautetaan strategia hyvin.

Uber on jännä osake. Se on tuottanut minulle puolen vuoden aikana todella hyvin, mutta siihen liittyy todella suuri “disruptioriski” autonomisen ajamisen kautta. Uberin omistaminen on myös eräänlainen veto Teslaa vastaan, mikä ei historiallisesti ole ollut ehkä kauhean järkevää. Uskon kuitenkin että todennäköisin skenaario on se, että Tesla ei tule saamaan autonomista ajamista toimimaan siinä ajassa ja skaalassa kuin mitä nyt uskotaan. Uskon että alalla ei ole yhtä voittajaa, ja uskon että Uberin verkostovaikutuksilla ja alustalla on paikkansa myös autonomisen ajamisen tulevaisuudessa. Toisaalta haluaisin silti myydä tämän osakkeen koska tämä disruptioriski on ihan realistinen ja mahdollinen ja voi rapauttaa koko Uberin liiketoiminnan, mutta koska yrityksen liiketoiminta on mennyt historiallisesti hyvään suuntaan niin myymään en todennäköisesti tätä ala ennen kuin yrityksen liiketoiminnan rapautumisesta on oikeita merkkejä. Niin kauan kuin yritys tarjoa joka kvartaali kasvavaa vapaata kassavirtaa, turha hypätä kyydistä pois.

Olen aina pitänyt varainhoitoalaa Helsingin pörssin houkuttelevimpana toimialana: korkea kannattavuus, toisaalta liikevaihdon kasvu voi tulla kahta kautta: joko myynnin kasvuna tai AUM:n (assets under management) kasvun kautta. Kuinka moni firma pystyy kasvattamaan liikevaihtoa ilman että se myy yhtään enempää? Titanium ja eQ ovat mielestäni olleet Helsingin pörssin varainhoitoalan laadukkaimmat ja kiinnostavimmat yritykset, mutta noussut korkotaso ja Suomen kiinteistösektorin ongelmat eivät ole kohdelleet näitä menneiden vuosien tähtiä hyvin. Oma usko on että ollaan hyvin lähellä pohjia näiden liiketoimintojen (ja osakurssien) osalta, ja tuloskasvuun palataan viimeistään ensi vuonna. Jotenkin tuntuu että nyt näitä pitäisi ostaa isosti, mutta olen tullut siihen lopputulokseen että paljon järkevämpi strategia on odottaa että liiketoiminta kääntyy ennen kuin alkaa laittamaan uutta rahaa näihin sisään. Laitetaan uusi raha nyt niihin salkun yhtiöihin joiden liiketoiminta menee jo oikeaan suuntaan.

Ajattelin vain nopeasti kirjoittaa muutaman rivin tekstiä salkun sisällöstä, mutta tästä tuli ikään kuin vahingossa taas todella pitkä kirjoitus. Ajattelin jossain välissä että voisin käydä salkusta kaikki yhtiöt yksi kerrallaan läpi, mutta siitä tulisi varmaan sellainen romaani jota kukaan ei jaksa lukea. Ehkä jätän sen joulukuuhun kun käyn tätä vuotta läpi, jos teen silloin seuraavan salkkukatsauksen ja en muuta kirjoitettavaa keksi.

Loppuvuoden strategia on varmaankin jatkaa vanhoilla tutuilla linjoilla: isoimmaksi osaksi istutaan käsien päällä ja ei tehdä mitään. Jos jotain myydään niin sellaisia firmoja joiden liiketoiminta ei kulje oikeaan suuntaan. Kiristynyt arvostus ei ole syy myydä, ja toisaalta laadusta en ole valmis tinkimään halvan arvostuksen vuoksi. Puskurirahasto on nyt taas onneksi siinä kunnossa että sinne ei tarvitse rahaa laittaa, mutta tariffipaniikissa ärsytyksen aihe ja oppi oli se että salkusta olisi hyvä olla 5-10% käteisenä odottamassa hyviä ostopaikkoja, joten loppuvuonna tulen tekemään vain pieniä ajallisia hajautuksia, ja loput palkkatuloista säästyvät rahat jätän käteiseksi kunnes salkusta on vähintään 5% käteisenä.

27 Likes

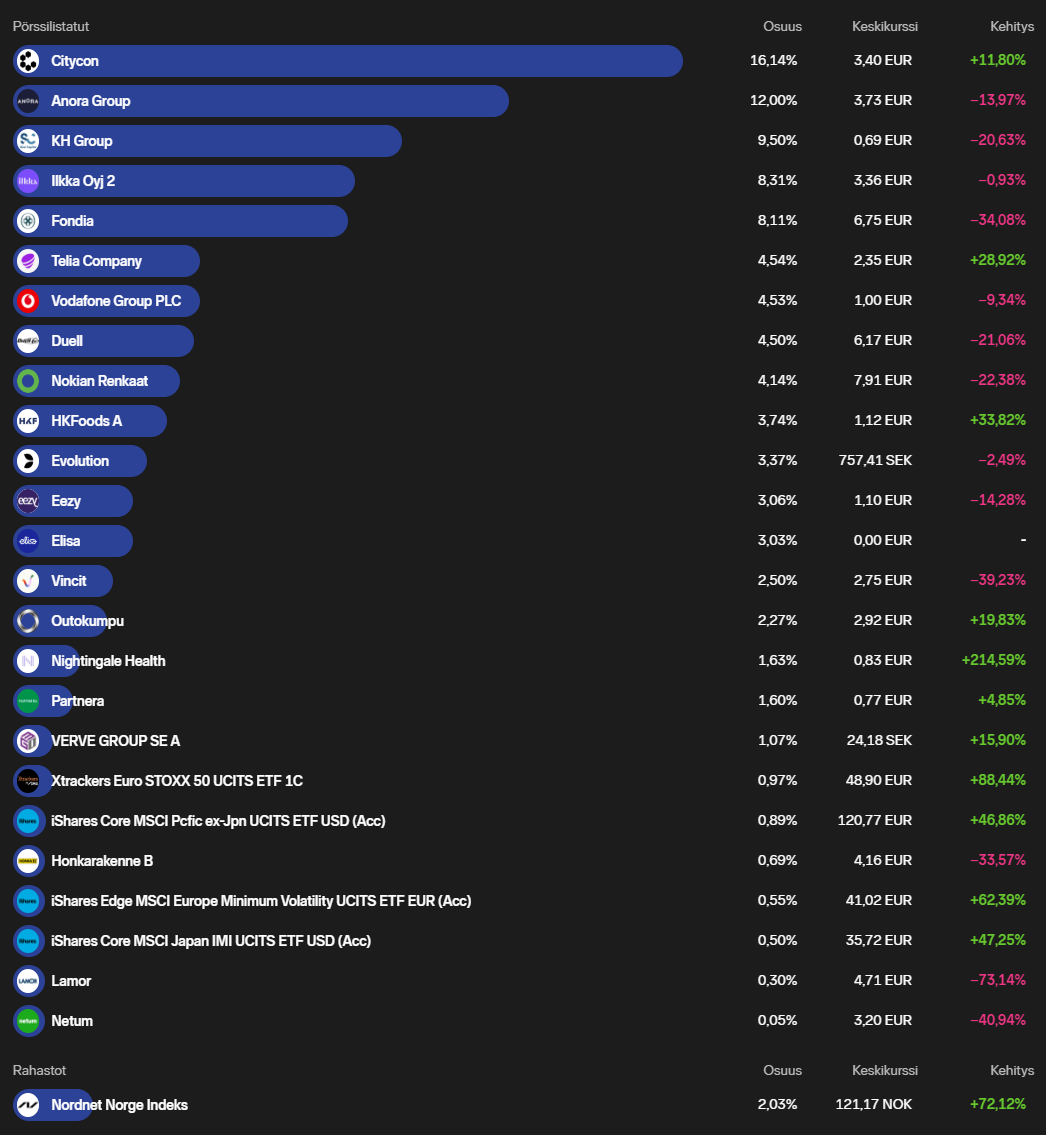

Traditionally, here’s the easiest quarterly update: the current portfolio content. The biggest changes, such as Duell’s collapse (due to the share price collapse), and the trades can be found on Sijoitustieto’s blog (I’ve also posted in the buy/sell thread).

19 Likes