An astonishingly unique portfolio. May I ask where you got the ideas for these and how long you’ve been investing?

I checked several of them on Seeking Alpha. Quite impressive return curves, respect!

An astonishingly unique portfolio. May I ask where you got the ideas for these and how long you’ve been investing?

I checked several of them on Seeking Alpha. Quite impressive return curves, respect!

No stocks in the portfolio. Cryptocurrencies make up about 3% of assets, but they are not in the chart. The portfolio has performed well, and if indices continue to decline, I will likely sell interest-bearing assets and move more money into indices. I personally expect the S&P500 to hit new lows in the coming months, unless Trump surprises and starts making decisions whose permanence can be trusted.

I have been investing in my current way for about two years. Ideas have been gathered mainly from Fintwitter and Substack writings, although, for example, the initial acquaintance with investment companies was made several years ago.

A quarterly review is traditionally easiest to start with the portfolio’s current holdings. Taking into account pending dividends of €3730 - taxes, the investment rate is 201%.

I do have these investments, probably too many. 54 in total. The intention is to trim them down at some point and consolidate positions, but currently, the market is so volatile, and I’m not keen on selling at a loss. However, for example, I’d like to sell Besi and invest that money directly into the VanEck Semiconductor ETF, but now is a bit of a bad time. A return of approximately 7% has been achieved this quarter, which I think is quite good; most of it came from active trading and selling.

The TOP3 best investments are Magellan Aerospace Corporation, JDE Peet’s N.V, and Veren Inc.

The TOP3 worst investments are Stellantis N.V, VanEck Crypto& Blockchain Innovators ETF, and BE Semiconductor Industries N.V.

The goal for the next quarter could be to consolidate positions and reduce the number of investments; for example, 40 could be a good target.

Quick Q1 2025 portfolio update.

Evolution gaming 10.0 %

Qt 5.5 %

Svenska Handelsbanken 5.3 %

Puuilo 5.0 %

Revenio 5.0 %

Tractor Supply 4.2 %

Talenom 4.0 %

Gofore 3.7%

Sampo 3.6 %

Harvia 3.3 %

Nokian Renkaat 2.7 %

Tieto 2.4 %

Sandvik 2.1 %

Berkshire Hathaway 1.6 %

Fastenal 1.0 %

Vaisala 0.6%

ADP 0.4 %

Graco 0.4 %

Atlas Copco 0.3%

Nordea 0.3 %

Cash/fixed-income investments 16.2%.

Funds and ETFs (Seligson, Pyn Elite, Splitan, EUNL, EUNK, IUSN, Seligson & Co OMX Helsinki 25) 19.7%

New investments in the portfolio: Vaisala, Atlas Copco

Additions: Evo, Qt (addition before strong earnings report)

Sold off: eQ

Reductions: Tieto, Qt (after earnings report)

Short-term trades at a loss: Nokian Renkaat

The portfolio’s cash/fixed-income position has grown slightly. The proportion of cash is currently too large. I aim to buy more quality companies when the price is right.

During the last quarter, I finally bought a small position in Vaisala. It would have been available much cheaper before, but I just hadn’t pulled the trigger. However, the company is of such high quality that I finally dared to jump on board even at these prices. Similarly, Atlas Copco has been on my watchlists as a quality company for a longer time. As a result of a price drop, it also found its way into my portfolio.

I ended up selling eQ from my portfolio on a somewhat accelerated schedule. The schedule, however, could have been faster, in which case I would have incurred smaller capital losses. The company’s ownership structure is simply not to my liking, so it has no place in my portfolio.

Although the number of companies in my portfolio increased by one, my intention is to gradually reduce the number while increasing the average quality. I will increase diversification by simultaneously growing the proportion of ETFs and passive funds. Monthly savings into funds/ETFs will therefore continue.

Currently, Tieto, Talenom, and Nokian Renkaat are most under fire among my portfolio companies. I have been following Tieto’s stumbling for long enough, and it is not high-quality enough for my portfolio. Nokian Renkaat’s special situation got a bit of an extension. The company was not originally intended for a long-term portfolio, so it can go when the time is right. I will own Tieto and Nokian Renkaat in the future through a Finland ETF. I will follow Talenom’s operations with great interest this year. If there is no clear turnaround during 2025, the company will very likely fly out of my portfolio.

Let’s also note here that the median P/B 2025 for Finnish companies followed by Inderes, calculated from Inderes’ website, is 1.68 (P/B 2026 median 1.63), and Inderes has 19 buy recommendations and 12 sell recommendations. CNN’s Fear & Greed index was 19 (Extreme Fear) at the turn of the quarter. However, the number of Inderes’ buy recommendations has again decreased during the past quarter: 24 → 14 → 10 → 25 → 19. As a long-term investor, I interpret “add” and “reduce” recommendations to some extent as “hold” recommendations.

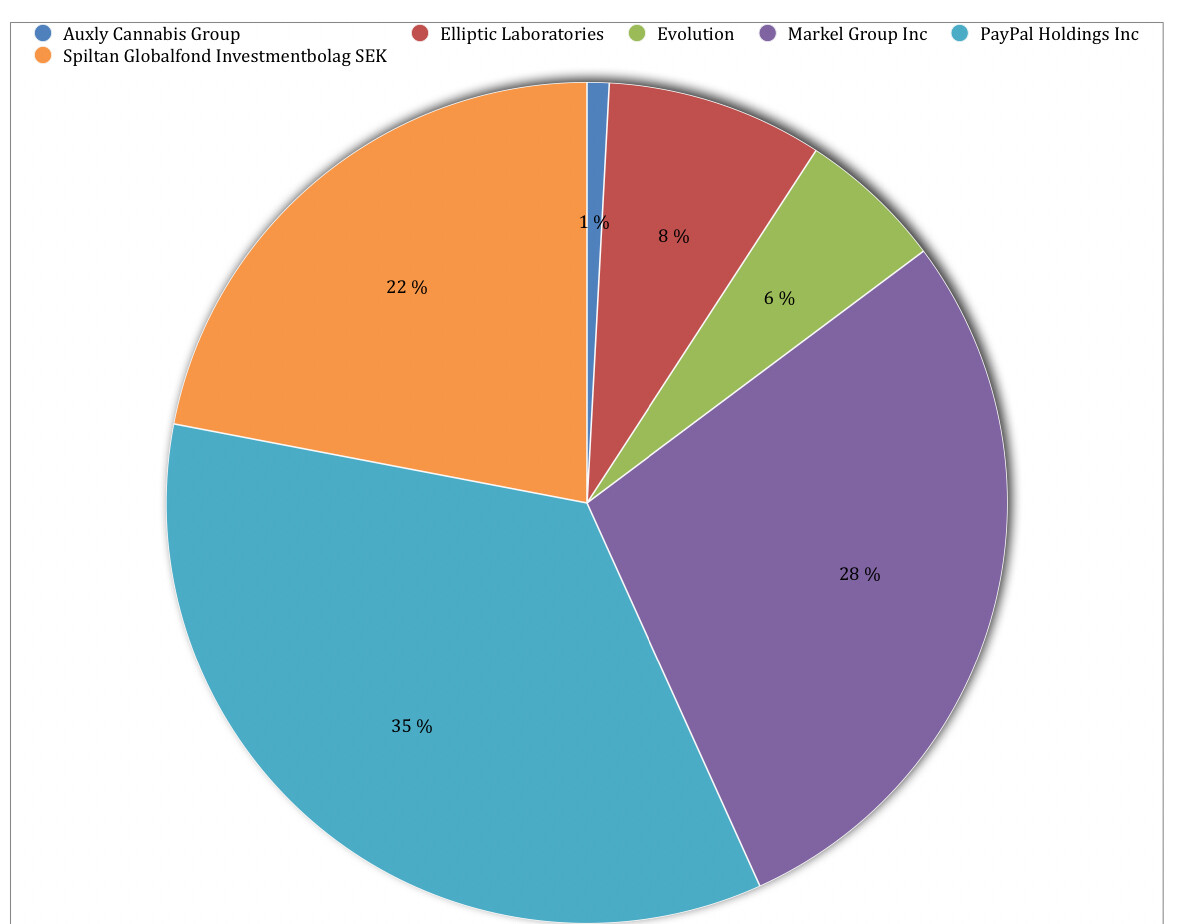

Exceptional situation in the portfolio. Paypal’s weighting has been raised to 35 percent due to the decline. Just last week it was 15. Sometimes I feel like taking a risk - usually I’ve had to pay the price for it.

Elabs has been added gradually. Evo just came back into the portfolio.

In addition to this Nordea portfolio, there is also a 15% slice of the portfolio in the Phoebus fund, which balances that out.

edit. yesterday 2.4. I got cold feet in the last trading minutes and sold a good 30% of Paypal. Now looking at where the markets are heading, I probably should have sold even more.

Tämä katsaus kattaa vuoden 2025 ensimmäisen vuosineljänneksen. En ole siirtymässä kvartaaliraportointiin, vaan seuraava tulee puolen vuoden päästä syksyllä. Salkun koko on reilut 24 tuhatta euroa. Tästä pääsee suoraa loppuun.

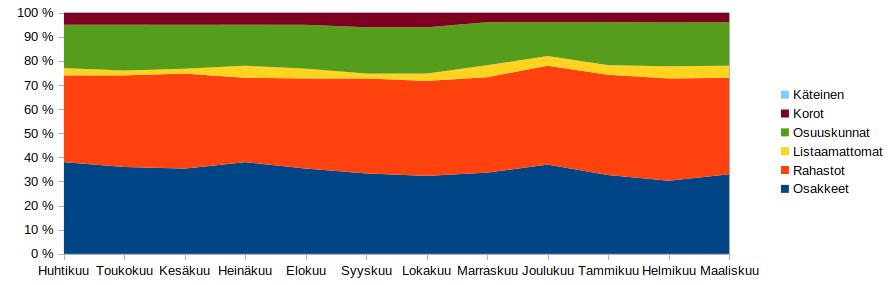

Ostot:

Osakkeet:

Osakeannit:

Rahastot:

ETF:

Osuuskunnat:

Korot:

Myynnit:

Osakkeet:

Rahastot:

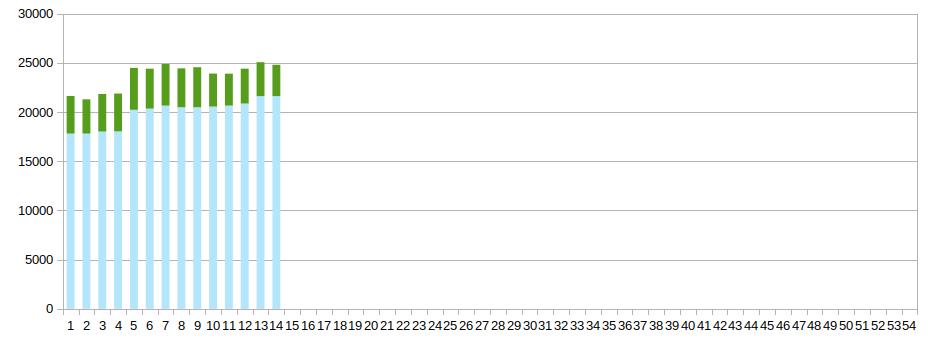

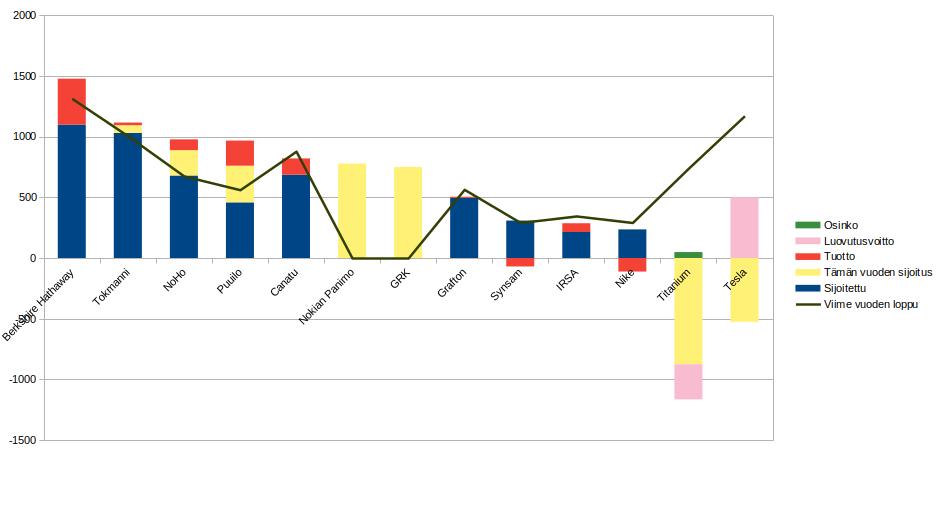

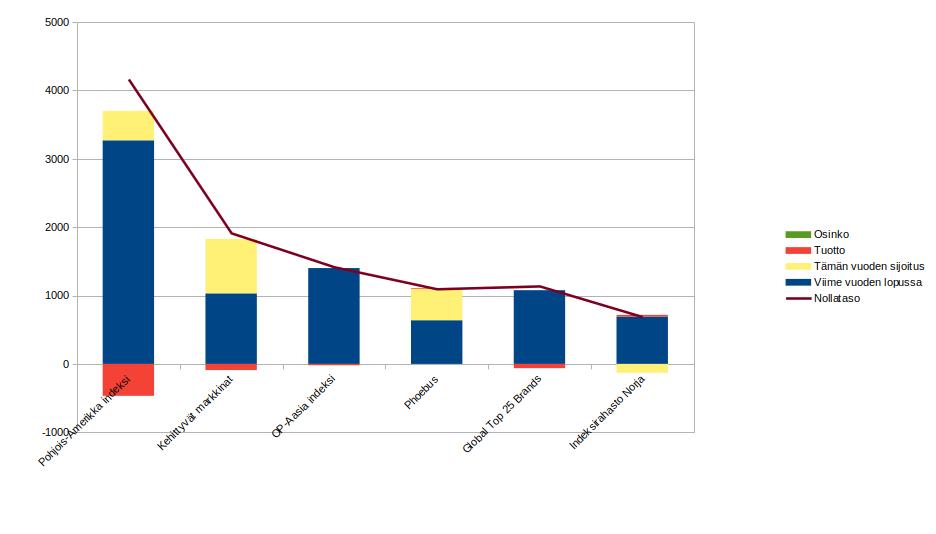

Kuvaan salkun kehitystä viikkopylväinä euroina.

Vaaleansininen on sijoituksen määrä. Kumulatiivinen tuotto näkyy vihreänä. Kun pylväs lähtee punaisena, salkku oli kokonaisuudessa tappiolla.

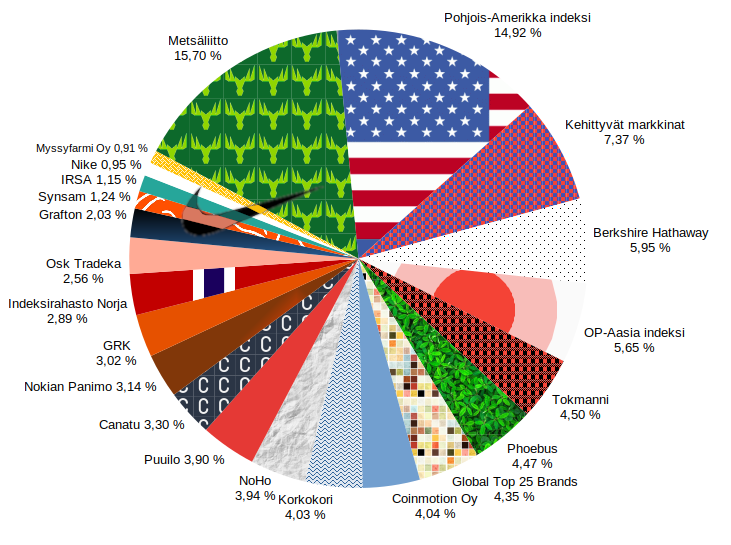

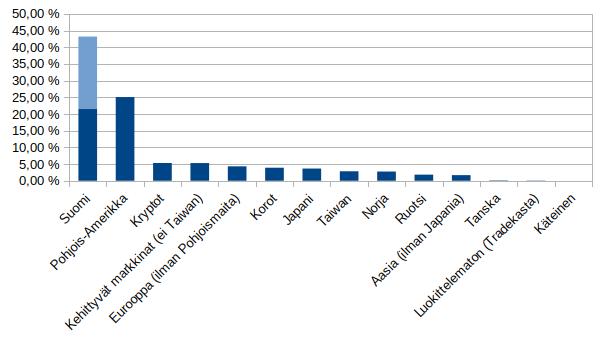

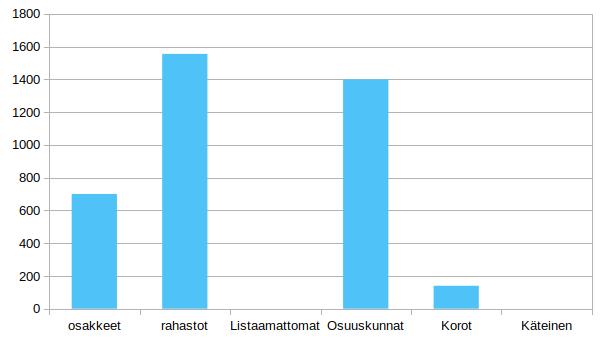

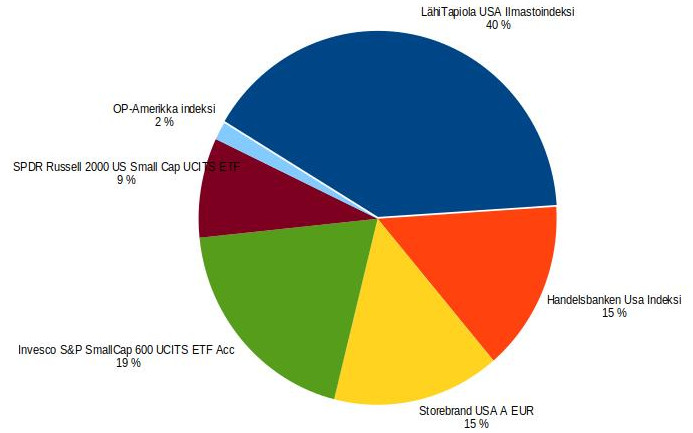

Osakkeiden maantieteellinen hajautus ja omaisuusluokat:

Allokaatio:

Osakkeet 33 %

Rahastot 40 %

Listaamattomat yritykset 5 %

Osuuskunnat 18 %

Korot 4 %

Salkussa ei ole käteistä.

Salkkuni allokaation palautusarvot uusina sijoituksina 2025 lopun tavoite:

Suojan lisäys 2175 euroa

Osakkeiden vähennys 4428 euroa

Likvidoimisprosentti 77 %

Jätän likvidoimisprosentin ulkopuolelle vaikeasti tai hitaasti likvidoitavat kohteet:

-Osuuskuntien tuotto-osuudet

-Listaamattomat yhtiöt

Osinkoa maksavat yhtiöt 73 %

Tässä on mukana listatut ja listaamattomat osakkeet, jotka maksavat osinkoa.

Suojaamattomuusarvo 8,57 %

Tämä arvo on toteutuneen salkun koon ja suojan laskentaan käytettävän tavoitearvon välinen erotus prosentteina.

Uudet sijoitukset ja lunastukset vuonna 2025

En ota foorumilla mitään näkemystä politiikkaan. Katsoin, että ennustin Suomen hallituspohjankin väärin. Totean vain, että minulla ei ole mitään taitoa käsitellä Yhdysvaltojen politiikkaa. Teslan osake kuitenkin politisoitui voimakkaasti Elon Muskin siirtyessä Trumpin hallintoon. Näin Trumpin politiikka epäsuorasti vaikuttaa Teslan brändiin. Euroopassa keskiöön on tullut Trumpin Ukraina-politiikka, joka näyttää pelaavan Venäjän pussiin. Itse kuitenkin tiedän, että toimintani jälkimarkkinassa ei vaikuta mihinkään, koska omistukseni ovat joka suhteessa minimaalisia. Kun myyn osakkeen uudelle omistajalle tai treidaajalle, niin kukaan ei voi tietää onko kyseessä protesti tai voittojen kotiutus. Lisäksi viime vuonna tein myyntejä ihan vain siksi, että rahat loppuivat eli en sinänsä nähnyt yhtiöitä huonoina. Tässä kontekstissa en siis voi pitää Tesla-myyntejäni kovinkaan suurena eleenä.

Tietyllä tavalla voisin nyt ohittaa syyt miksi, Tesla alun perin oli salkussa. Voisin olla puhdas Tesla-häpeästä. Palataan kuitenkin näihin. Ehkä helpoiten perusteltu syy on omistaa Teslaa indeksin mukaan. Kuten olen todennut, niin kaikki USA-indeksirahastot ei omista Teslaa, joten voin perustella suoraa omistamista oikeamman indeksisijoittamisen kautta. Oikeasti minun piti pitää Teslaa salkussani myös siinä tilassa, kun olisin ollut taloudellisessa vaikeuksissa. Pistin Teslan siis hyvin pitkään salkkuun melkeinpä ikuisuussalkkuun. Tämä tietenkin aiheutti sen, että en myynyt aivan heti, kun brändi sai kolhuja Elon Muskin toimista. Ehkä raskain peruste on Elon Musk -fanitukseni, jonka olisin nyt mielelläni ohittanut. Tämä varmaan olisi herkullinen aihe, mutta en pysty nyt kovinkaan syvällisesti tähän tarttumaan. Marraskuun lopulla kuitenkin tarkastelen, mikä olisi Tesla-position koko. Siltä osin täytyy tarkkailla Elon Muskin tekemisiä.

Jos nyt mennään järkisyihin liittyen Tesla-myyntiini, niin korkea arvostus samalla, kun brändi vedettiin vessasta alas. Yhtiön toimitusjohtajalla on liian monta rautaa tulessa ja Tesla on tuuliajolla. Myyntini ehkä suurin este oli Nordnetin korkea kulu, mutta pystyn ohittamaan sen suurella voitolla. Verotuksesta ei tarvinnut huolehtia, koska myin osakkeet tappiollisesta osakesäästötilistä. Sain rahat siis heti käyttöön verottomana. Jos Tesla olisi ollut arvo-osuustilissä, olisin miettinyt vielä toisen kerran myynnin järkevyyttä.

Olisiko kaikki Yhdysvaltojen omistukset pitänyt myydä protestiksi nykyhallintoa kohtaa? Pakko aluksi nostaa humoristinen seikka, että olisin tehnyt myynnit varmaan puhelimella, joka on pumpattu täyteen yhdysvaltalaisia ohjelmistoja ja palveluja. Lähtökohtaisesti en lähde myymään salkusta mitään sellaista, mitä en pysty boikotoimaan. Sanoisin, että pieni boikotti on huomattavasti tehokkaampi tapa kuin myynnit jälkimarkkinassa. Yhtiöt tuskin milläin tavoin reagoi esimerkiksi suomalaisten rahastojen vähennyksiin. Linkki Yhdysvaltojen hallintoon on vielä pidempi. Yhtiökokouksissa sen huomaa, mitkä ovat piensijoittajien vaikutusmahdollisuudet - ei minkäänlaiset. Mutta jos ei ole uskoa Yhdysvaltoihin ja yhdysvaltalaisiin yhtiöihin, niin ei siinä mitään, jos myy tai ei alkuaankaan omista.

Suomen kiinteistömarkkinan ongelmat heijastuivat myös Titaniumin hallinnoimiin rahastoihin. Esimerkiksi Titaniumin Hoivarahastoon kohdistui niin suuret lunastukset, että rahasto suljettiin lunastuksilta toistaiseksi. Tämä johti myös osakkeen kurssin romahtamiseen. Olen hakenut kiinteistöriskiä Titaniumilla ja nyt sitten sain riskit lunastettua. Pakko sanoa, että olen vierastanut yhtiön uutta johtoa ja strategiaa. Strategian onnistettua yhtiöstä tulee huomattavasti vähemmän riippuvainen kiinteistörahastoistaan. Siitä halutaan monipuolinen varainhoitotalo. Kuitenkin valitsin yhtiön kiinteistörahastotalona en varainhoitajana, niin alkuperäinen sijoitusidea ei kanna. Helsingin pörssistä löytyy myös muita paljon pidemmällä olevia varainhoitotaloja, niin miksi jäisin Titaniumiin.

Katsoin myös Inderesin ennusteita ja peilasin sitä omaan sijoitushorisonttiin. Tämän mukaan yhtiö olisi edelleen kuopassa strategisen sijoituskauteni päättyessä vuonna 2028. Ehkä suurimmista riskipesäkkeistä pitää pysyä erossa ja pyrkiä mahdollisimman tasaisiin sijoituksiin.

Kuitenkin menin yhtiökokoukseen vielä haistelemaan tilannetta ennen myyntipäätöksen tekoa. Pidän hyvin tärkeänä yhtiökokouksessa toimitusjohtajan katsausta, mutta se oli varmaan kokonaisuudessaan sama kuin vuositilinpäätöksen tiedotustilaisuudessa, niin eipä tämä mitään suurta elämystä aiheuttanut. Yhtiökokouksen tarjoilussa oli vain pelkkää kahvia ja teetä. Enkä saanut edes mustekynää muistoksi. Eipä tässä saatu päätä käännettyä.

Ehdin jo kertoa, ettei pienosakkaalla ole minkäänlaista vaikutusta, jos osallistuu yhtiökokoukseen. Pidin kuitenkin Tokmannin yhtiökokouksessa voimallisen ja vaikuttavan puheen osinkojen puolesta. Tämä on johtanut siihen, että Tokmanni kertoo tarkemman ajankohdan syysosingonjaolle vuonna 2025 kuin ennen. Syysosinko on siis edelleen hallituksen päätöksen takana ja osinko jaetaan neljännellä vuosineljänneksellä, jos hallitus niin haluaa tehdä. Ennen siis ei oltu edes jakokvartaalia ilmoitettu etukäteen. Kyllä tästä pitäisi saada kunniamerkki Osinkopuolueelta.

Valitettavasti toinen valituksen aiheeni yhtiökokouksessa ei saanut tuulta purjeisiin. Suomenkielisiin tuloswebcasteihin ei palattu, eikä näitä myöskään tekstitetty. Tältä osin siis jatkan passiivista lähestymistapaa sijoitusta kohtaan. Tarkoitus on saada omistus yhteen tiliin, mutta tämä menee ainakin näillä näkymin ensivuoteen. Ajatus on myös, että tämän vuoden yhtiökokous olisi viimeinen toistaiseksi. Tokmannin yhtiökokous on ehdottomasti lempparini, mutta sinne meno on aika iso taloudellinen ponnistus.

USA-sijoittamisesta tuli vähän samat fibat kuin lentämisestä. Vihdoin kuin sain pitkään ajan jälkeen kasvatettua USA-painon tavoitteeseen siitä tuli paheksuttavaa. Tulen toistaiseksi Pohjois-Amerikassa painottamaan indeksien sijaan salkunhoidollisia instrumentteja eli Berkshire Hathawayta ja Phoebusta.

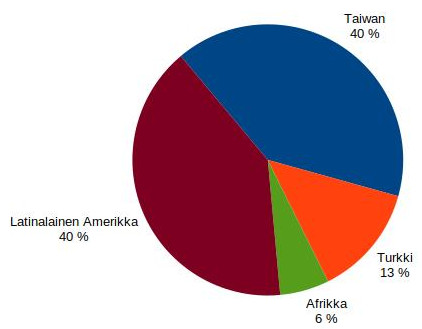

Alkuvuonna lisäsin Tropico LatAm - rahastoa ja Taiwan-ETF:ää. En näe tällä hetkellä mitään sellaista, että painotuksia tarvitsisi muuttaa. Positio kehittyviin on myös oikean kokoinen mielestäni.

Turkki-ETF varmaan olisi pitänyt myydä kokonaan silloin kuin kevensin.

Olen tyytyväinen tuotteeseen, mutta en näe tällä hetkellä tarvetta lisäillä. Olen odottavalla kannalla, koska tarkoituksena on tehdä iso muuvi Japaniin.

Itse uskon edelleen myös osakepoimintaan ja Phoebuksesta sitä saa lompakon paksuutta katsomatta. Minusta tämä sijoittaa vähän samanlaisesti kuin minä. Anders Oldenburg tosin sijoittaa menestyksekkäästi ja minä menettävästi. Kuukausisäästän tällä hetkellä Phoebusiin. Lisäksi olen tehnyt isompia kertalisäyksiä.

Tämä on jäänyt vähän muiden rahastojen jalkoihin. Tämä on kuitenkin edelleen halvin tapa itselleni saada brändejä salkkuun. Nikekin olisi kannattanut nauttia tämän kautta yksistään. Ongelma etten tätä lisää, löytyy Phoebusista, joka mahdollisesti sulautetaan tähän rahastoon. Uskon, että tulevaisuudessa teen päätöksen tämän rahaston ja indeksisijoittamisen välillä.

Kevensin Norjaa, koska ajattelin, että ehkä yhteen maahan sijoittavan rahaston koko ei pidä olla niin suuri. Pidän edelleen tämän rahaston brändejä mielenkiintoisena.

Tämä voisi viitata siihen, että olisin poistumassa foorumilta, mutta olen ainakin tämän vuoden loppuun täällä. Olen yhä täällä (Ainda Estou Aqui) on siis Brasilialainen elokuva, jonka olin katsomassa siskon kanssa. Tositapahtumiin perustuva elokuva kertoo entisestä kongressiedustaja Rubens Paivasta ja etenkin hänen perheestä. Sotilasjuntta vie julmiin kuulusteluihin Rubensin, hänen vaimonsa ja yhden tyttäristä. Rubens ei koskaan palaa kuulusteluista. Valitettavasti tämä aihe tuntuu hyvin ajankohtaiselta.

Tampereen Teatterin suurproduktioon varasin liput jo viime elokuussa. Näytäntöni oli tammikuussa ja suunnitelma oli viettää aikaa Tampere-talossa myös ennen näytäntöä.

Saavuin Tampere-talolle kahdentoista tuntumilla ja piilotin Lidukasta ostamani takin naulakkoon. Ajattelin, että jos joku haluaa varastaa sen kauheuden niin siitä vaan. Lounastin Tuhto-ravintolassa. Ruuan maksoin Black Friday:na ostamalla NoHo-lahjakortilla. Olin kuitenkin maksanut lahjakortista täyden hinnan. Lounas oli melko perustasoinen.

Lounaan jälkeen käväisin pikku ostoksilla Muumi-kaupassa. Ostin myös käsiohjelman Taru Sormusten Herraan, vaikka nämä alkavat olla hieman tyyriitä. Seuraavaksi tutustuin Muumimuseoon. Muistaakseni olen lapsuudessa nähnyt kolmiulotteisia kuvaelmia Metso-kirjaston alakerrassa. Näitä oli museossa runsaasti. Lisäksi oli maalauksia ja piirroksia. Yleisesti ottaen museo on hieno. Aikahan siinä kului mukavasti. En ehtinyt varata ajoissa väliaikatarjoilua niin hommasin sen ennen näytöstä.

Tuhdossa oli kuitenkin myös erittäin hyvä väliaikakattaus niin en jäänyt ilman sitä. Taru Sormusten Herrasta on haastavaa saada näyttämölle. Näyttelijöiden lukumääräkin on varsin pieni ja se näkyy etenkin kohtauksissa, jossa pitäisi olla joukkovoimaa. Siksi näytelmässä pyritään keskittymään vain tiettyyn osa alueeseen, joka oli tässä tapauksessa Frodon ja Samin matkaa Mordorin Tuomiovuoreen. Varmasti joskus kritiikkiä on saanut se, että varsin miehinen on hahmogalleria Taru Sormusten Herrasta kirjassa, niin tähän peilaten voi pitää erikoisena, että Galadrielin rooli oli annettu miehelle. Tosin naisilla oli hobitin rooleja.

Tuomas Kantelinen oli säveltänyt teokselle uuden ääniraidan, jonka orkesteri soitti livenä. Musiikki sopi hyvin esitykseen, mutta tuntui, että se oli todella lähellä leffojen musiikkia ja näin ei tuonut mitään uutta. Lavastus ja puvustus olivat erinomaiset. Tampere-talon isosali on varsin kookas, niin oli hyvä, että oli ruudut, jossa oli suurennoksia esityksestä. Itsekin pyrin hieman nuukailemaan ottamalla syrjäisen paikan katsomosta.

Pituutta teoksella oli väliaikoineen reilut neljä tuntia, niin tietenkin näytelmän onnistumisena voi pitää, sen että se piti kokoajan otteessaan. Pakko sanoa, että on ärsyttänyt sellaisten henkilöiden somekirjoitukset, joiden mielestä ainoa oikea versio Taru Sormusten Herrasta on Suomenlinnan produktio 80-luvun lopulla. Entä nämä nuoremmat sukupolvet. Kai niillä on oikeus nähdä näytelmä. Omasta mielestä on tervetullutta uudet versiot. Ei ne poista vanhoja. Olen katsonut myös Mahtisormukset sarjaa. Itselläni ei ole mitään pyhää suhdetta Taru Sormusten Herraan, niin hieman jopa pohdin, että menenkö laisinkaan katsomaan, mutta kyllä kannatti mennä.

Poistuin Tampere-talosta illalla puoli yhdeksän tienoilla. Hyvin vierähti koko päivä siellä.

Törmäsin tämän tyyppisiin lauseisiin Suomen Nato-prosessin aikana. Nyt tämä on tullut uudelleen pinnalle Yhdysvaltojen uuden hallinnon myötä. Klaus Härön ohjaaman leffan nimi viittaa varmaan Suomen ja Saksan aseveljeyteen, kuin myös setä Stillerin auttamistyöhön juutalaispakolaisten parissa. Kuuntelin myös Rony Smolarin kirjan Setä Stiller: Valpon ja Gestapon välissä. Härö oli tehnyt leffasta erittäin kompaktin mittaisen, niin kirja antoi paljon lisätietoa aiheesta. Suomi oli jatkosodan aikana erikoisuus, kun saksalaiset ja juutalaiset sotivat rinnakkain Neuvostoliittoa vastaan. Muutamalle suomen juutaiselle sotilaalle myönnettiin rautaristikin.

Tilanne oli kuitenkin kotirintamalla vakava. Etenkin juutalaispakolaisia Gestapo halusi palautettavaksi Saksaan. Gestapolta löytyi kuitenkin myös lista kaikista suomalaisista juutalaisista, vaikka lista ei suoranaisesti joutunut Gestapon käsiin leffan kuvaamalla tavalla. Kahdeksan juutalaispakolaista kuitenkin lähetettiin Saksaan erityisesti Valpon johtajan Arno Anthonyn ja sisäministeri Toivo Horellin johdolla. Kyllähän tämä häpeätahra elokuvan ansaitsee.

Katsoin myös dokumentin suoratoistopalvelu Maxista, joka liippaa aihetta. Dokumentin nimi on The Commandant’s shadow. Se kertoi Auschwitzin komendantin pojasta, joka tuntui olevan yhtä naiivi, kuin Poika raidallisessa pyjamassa päähenkilö Bruno. Oliko se jonkinlaista sokeutta isänsä toimiin vai aidostiko ei mitään havainnut.

Luvialla luotettiin tänä vuonna huumoriin. All Shook Up - Liekeissä - musikaalissa oli Elviksen musiikkia, mutta se ei perustunut kuitenkaan Elviksen elämään. Juoni on lyhyesti se, että nuori mies saapuu moottoripyörällä pikkupaikkakuntaan ja tästä sitten kehkeytyy monimutkainen ihmissuhdesoppa. Hyvää musiikkia ja huumoria.

Olen palastellut tämän nyt niin pieniin osiin ja kertoillut eri osista, mutta Helsingin matka koostui Titaniumin yhtiökokouksesta, Design- ja arkkitehtuurimuseosta, ruokailusta Strindbergissä, Pokka pitää - näytelmästä Aleksanterin teatterissa ja Olen yhä täällä - elokuvasta. Parempi, että laitan vain muutamia kuvia:

Kuuntelin myös äänikirjoja ja nostan nyt pari kirjaa esiin. John Boynen kirja Tarkoin vartioitu talo kertoo maalaispojasta Georgista, joka pelastaessaan keisarin veljen kuolemasta, nousee korkeaan arvoon keisarin hovissa. Tarina oli kuitenkin liian naiivi ja muistutti 20th Century Foxin Anastasia animaatiota. Tarina oli mukava ja hyvin kirjoitettu, mutta olisin toivonut jonkin yllätyksen loppuun, kuten Kaikki särkyneet paikat - kirjassa, joka on Boynen uudempi kirja.

Pirkko Saision kirja Suliko, menee Stalinin pään sisälle. Erittäin paljon pidin tämän kirjan tarinoista ja huumorista. Pirkko Saisio luki kirjan itse ja kirjailija tuli näin lähelle kuuntelijaa. Kirja ei ollut edes pitkä ja silti vaikuttava. Täytyy jossain vaiheessa kokea tämä uudelleen.

Akirassa uudelleen aktivoituminen tapahtui jännästi, kun totaalikyllästyin tapettiin. Keräillessä Akira-mangaa oli käynyt niin, että 11. kirja oli tullut tuplana. En laiskuuttani jaksanut sitä myydä, niin kokeilin miten tapetointi sujuisi sillä. Hyvinhän se sujui, mutta riitti hädin tuskin. Vanha tapetti paljastuu, jos tauluja ottaa pois, mutta olen nyt hankkinut toisen Akira-kirjan, jolla on tarkoitus jatkaa tapetointia.

Hankin myös Akira-leffan soundtrackin, joka on hyvin mystinen kokonaisuus, mutta siinä on myös musiikkia muistuttava kohta. DVD Akirasta on ollut hyllyssä hyvin pitkään, mutta otin nyt vasta pois muoveista. Jotenkin tämä oli niin vaikuttava kokemus leffateatterissa, niin olin säästellyt tätä DVD:tä. On tämä edelleen hätkähdyttävä katselukokemus.

Manga on kuitenkin huomattavasti kattavampi. Luin sen sitten leffan katselun jälkeen. Dystooppisessa maailmassa tuntuu olevan ajankohtaisia asioita.

Verrattain pitkän ajan jälkeen on mukava palata vanhoihin juttuihin, ja ehkä löytyy jotain uutta puolta näistä

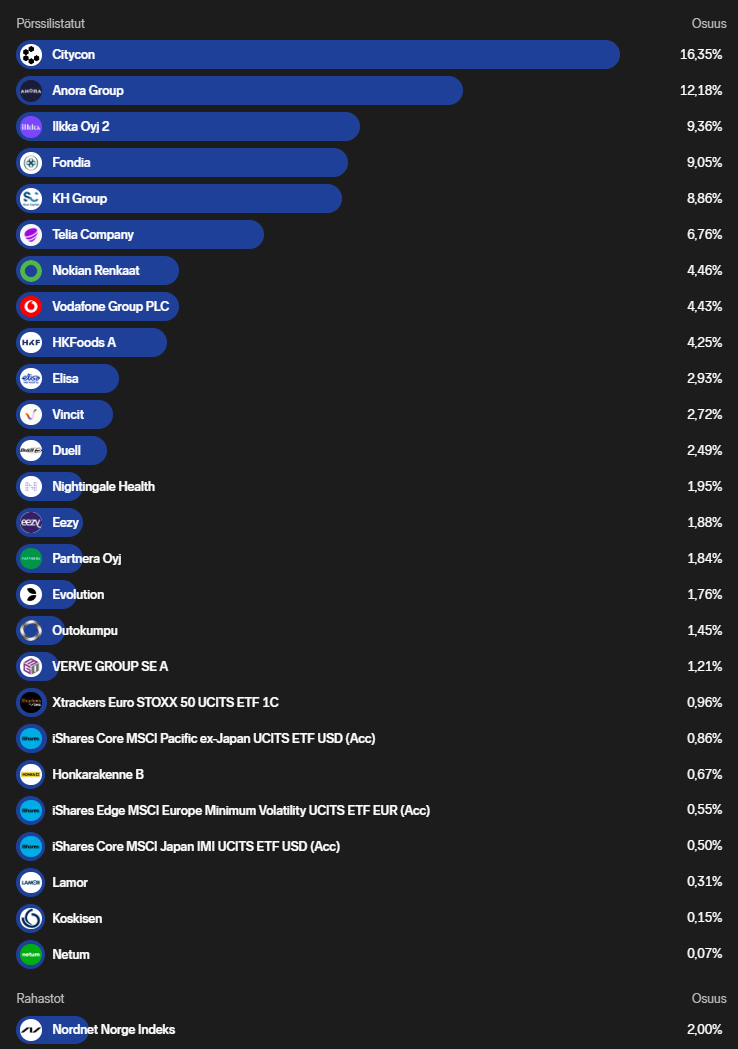

Cash: ~33%

Puuilo: ~20%

Ålandsbanken: ~10%

Sampo: ~7%

World index: ~9%

Other funds: ~9%

In addition, half a dozen negligible amounts in different companies. It was good to calculate this. There’s too much cash, but I don’t want to buy unnecessary things just because it’s burning a hole in my pocket. The future is uncertain, and it’s nice to have chips for opportune moments. Puuilo and Ålandsbanken could also be added at suitable points. I like concentration.

The portfolio has been diversified somewhat more, and free cash* accounts for one-fifth of the portfolio.

In direct stock investments and the Phoebus fund, I focus on quality investing, and with index funds, I address industry bias and geographical diversification.

I am currently considering what to do with the free cash. The next interesting day is a month away, when Berkshire’s annual meeting and Buffett’s over 4-hour Q&A session will take place. Perhaps I can get ideas from it on where things are heading and what to do.

I don’t intend to hold this much cash indefinitely; I have always had a large allocation to the market, and that has felt like a suitable strategy for me. But I can certainly wait a month (unless I make a small addition to Vaisala in the meantime).

Industry, Size, and Geographical Distributions:

*free cash = total cash - upcoming larger expenses - emergency fund

Funds in blue

Cash in yellow

Stocks in green

The weight of US stocks in the total is about 18-19%

Portfolio update for Friday evening. It’s been quite a hectic few days, and the portfolio has certainly melted down quite nicely. Or well, it’s not nice, I guess this is testing my investment strategy and belief in it, and much more. On the other hand, the world is quite chaotic, so I guess it all reflects in the market.

So, what have I been doing over the past half year or so? Well, I think I’ve acted the same way as before. I buy what I consider good companies and own them long-term. I’ve sold small portions of Konecranes when I’ve just had to realize good profits; typically, I’m really bad at this, I need to practice that too. Otherwise, I’ve been buying and continuing to diversify. I practically have a list of companies I think I’d like to own, and I pick them up for the portfolio when I have cash. All investable cash goes into the market quite quickly. Even today, I put money into stocks during big dips; was it wise, time will tell…

It seems that since the last update, the portfolio has mainly acquired Swedish listed companies. I’ve been looking at them for a long time too. This time, however, not those investment companies.

Is the portfolio over-diversified? Many would probably say yes, but I think it will grow even more. An interesting interview, by the way, on Inderes Nordic, where they interviewed the former host of Börspodden, and if I remember correctly, he said he has hundreds of companies in one portfolio… so there’s still a bit of a way to go.

I like dividends, so the portfolio’s dividend yield is 5.01%. This is naturally boosted by a few companies, most notably Mandatum (25.5%) and Nordea (16.5%).

We live in uncertain times, but we’ll move forward with this portfolio. The management of the companies in the portfolio are now my chosen portfolio managers.

Have a nice weekend everyone!

With a 233% investment rate and ALL-IN! for the weekend. A lower investment rate than at the turn of the year, just because it’s a bit higher + 20k more capital in the portfolio.

No huge changes as such. A significant increase in Duell’s position is probably the biggest single change by month-end.

So if someone asks for my view on the market (in Finland), my view is ALL-IN! There is, however, a bit of Sweden included now.

Faron approx. 84%

Cash approx. 16% I have to hold cash even though the FOMO is strong ![]()

This is the plan for now and it looks good, portfolio up 33% in 1 month, we are at ATH ![]() .

.

The customs issues didn’t ultimately stick, even though it dipped with the others and I managed to snap up 5000 more, I should have taken more at a lower price than now, but I didn’t dare.

The assumption, in light of current information, is that phase 2 results are good and should increase the stock’s value, or not, and now that there’s no pressure to raise money and the patents have been regained, potential partners cannot blackmail Faron by delaying, so presumably more intense negotiations with partners will begin, or not ![]()

My confidence is somehow too high right now, and I don’t see any weakness ![]()

UPM and Nokian Tyres are stocks I would like to see in my portfolio as long-term holdings in the future. Neste also perhaps, but the stock is now somehow in the hands of larger forces, so one doesn’t know what will happen next. These are therefore under observation.

Mandatum can be found in OP’s securities account.

Manta, oh wonderful Manta. ![]() One can’t help but wonder what returns it has already generated and dividends will continue to flow in the coming years.

One can’t help but wonder what returns it has already generated and dividends will continue to flow in the coming years.

| Name | Portfolio Share (%) | Change from Purchase |

|---|---|---|

| Evolution AB | 28.05% | 3.68% |

| QT Group | 15.64% | 38.04% |

| Harvia | 12.27% | 5.27% |

| iShares Core MSCI EM IMI ETF | 6.76% | 4.49% |

| Shell | 5.66% | 110.12% |

| Fortum | 5.23% | 12.91% |

| Nordea | 5.18% | 0.38% |

| iShares SP500 ETF | 4.58% | −6.79% |

| iShares Nasdaq Ucits ETF | 4.29% | 54.94% |

| Golar LNG Limited | 2.29% | 32.35% |

| iShares MSCI World Small Cap ETF | 1.93% | −21.12% |

| Apple | 1.62% | 164.57% |

| Cash | 6.51% |

This is a good diary-style thread to follow my own activity in the markets! The plan is progressing, and over the last year, I’ve cut down on extra companies in the portfolio. I don’t have enough time to follow so many companies, and currently, I feel quite satisfied with the number of holdings in the portfolio.

I can say that I’ve learned the hard way from Neste and Nokian Renkaat.

On the shopping list during market turmoil: EVO, QT, SP500 ETF, iShares Core MSCI EM IMI ETF.

New alternatives: Investor AB and some Europe-investing ETF index. The goal is to get the share of ETFs >20%.

Also for the OST (grandpa’s portfolio), the aim is to invest 20% of the capital in dividend payers (in which decade will OP manage to invest in foreign stocks with an OST?). Currently, the share of OST in the capital is 14.2%. Additionally, the goal is to reduce Finland’s share of the portfolio to 30% over the next five years (currently 38%).

I’ve been doing this for about five years now, and I recommend all other inexperienced investors to also write down their own investment plan in some file. It really calms the mind even when several months’ gross income melts away from the portfolio. Also, my own tendency to chase different stocks like a weather vane has calmed down.

Excerpts from my own investment strategy:

GOAL:

Retire earlier. Beat the OMXH GI (including dividends) index in the long term (+10 years) by 2%/year. The average return of the OMXH GI index over 20 years is 6.1%. In this case, the annual return requirement = 8.1%.

GENERAL THESES (copied from more experienced investors):

Forward!

Aren’t points 3 and 6 a bit contradictory?

Point 3 perhaps works better in day trading; in long-term investing, price fluctuations are part of the deal, and they shouldn’t sway one way or another.

Assuming one has chosen the right stocks for their portfolio, and the company’s performance relative to one’s own vision has not changed.

Let’s assume that Nordea is a great company in my opinion, I want it in my long-term dividend portfolio. An orange man tweets and the price drops, the company’s performance does not change. I sell at a 15% loss. I buy back at a higher price when the global situation stabilizes because the company is still great. In this case, only the broker won.

Good point, and they certainly are, undeniably. To clarify, the idea here is to practice timing purchases by trying to buy at technical support levels (EMA 200, EMA 50). Preferably in a so-called golden cross situation.

Those long-term HODL stocks (EVO, QT, Harvia, Nordea, Apple) will remain in the portfolio until at least 2030, so the -15% rule does not apply to them. SP500, iShares Core EM IMI ETF, World Small Cap ETF are included with a ‘hold until death’ philosophy.

For example, EVO has dropped -40% in one year, but I haven’t sold it because I feel the fundamentals are still sound, meaning point 10. has not, in my opinion, been realized for it. ![]()

Pension Portfolio 18.4.2025

Investment Plan: A fixed sum is invested in funds monthly, approximately 15% of net salary. ETFs are bought to balance geographical diversification if there is extra money in the account. A lump sum has been allocated to stocks, which will not be increased. Additional purchases must be made with dividends and sales. After a purchase, one must wait about a month before the next purchase. In the long term, my portfolio will mainly consist of index funds and quality dividend-paying stocks. Stocks are primarily sought from Finland so that the largest possible portion of dividends can be received tax-free into a stock savings account.

| Geographical Distribution | |

|---|---|

| North America | 49.7% |

| EU | 35.6% |

| Emerging Markets | 14.7% |

| Portfolio’s Largest Investments | Share of Portfolio |

|---|---|

| Handelsbanken USA Index Fund | 29.5% |

| OP World Index | 17.2% |

| Handelsbanken Europe Index Fund | 11.7% |

What goes up quickly can also come down quickly. Last year, the share of index funds rose from 66 percent to about 75 percent of the total portfolio in six months. Now we have returned to the situation of about 12 months ago. The reason for this is naturally the large weighting of the USA in a couple of global index funds and the EUNL-ETF found in the portfolio – in addition to a couple of USA index funds. Furthermore, emerging markets have started a pleasant decline since Trump pulled out the tariff board. I myself am expecting such stormy times for this year that I pulled out the cash reserved for special situations: the cash size in the portfolio has increased from 4.2% → 11.9%. If the shit really hits the fan, the intention would then be to buy more ETFs or perhaps even Berkshire Hathaway B shares. A small amount was already invested in global small-cap companies during the big dips of recent weeks.

I have also increased the amount of gold in my portfolio by buying a small slice of the IS0E-ETF. Just in case this trend continues – as I thought a couple of years ago.

On the stock portfolio side, the last six months have not been very commendable. The intention would be to build a dividend portfolio of quality domestic companies, perhaps mixing good dividend growers and large dividend payers. I have generally been very disciplined, trusted my own research, and tried to avoid buying companies whose business I don’t quite grasp. Well, all these principles went out the window when, in a weak moment, I impulsively bought Neste again at 13 euros – because it had previously seemed high-quality and had fallen so much. Now there’s another bright red line in the “long-term portfolio” in addition to Rinkulat – let’s try to learn from this. Regarding Detection Technology, I am not yet worried, and the China risk was known. My timing was downright magical (it slipped into the portfolio a month before the tariffs), but in the long run, I still see the company grinding out manna for the dividend portfolio with a good coefficient. The same applies to Viafin Service, which I swapped for Fortum during the tariff dip on 7.4.

My portfolio’s events for the past year are in full:

Newly Purchased: Neste (13 €), Detection Technology (14.5 €), Viafin Service (18.1 €)

Sold: Fortum (13.6 €)

There are several good Finnish companies on the watchlist, if Mr. Market were to come knocking again this year advertising Hesburger’s sales. Let’s still try to do our homework and follow Terry Smith’s simple advice, which is incredibly difficult to implement in practice.

Buy good companies, don’t overpay, and then do nothing

| Listed Stocks | Share of Stock Portfolio |

|---|---|

| Orion Corporation B | 8.8% |

| Nordea Bank Abp | 8.0% |

| Nokian Tyres Plc | 7.6% |

| TietoEVRY Corporation | 6.3% |

| Tokmanni Group Oyj | 6.2% |

| Orthex Plc | 5.2% |

| Detection Technology Oyj | 5.2% |

| Neste Corporation | 5.1% |

| NoHo Partners Oyj | 5.0% |

| Metso Oyj | 4.7% |

| Viafin Service Oyj | 4.7% |

| Valmet Corporation | 4.5% |

| Kalmar Oyj B | 4.4% |

| Marimekko Corporation | 3.3% |

| Cash | 21% |

The dividend yield of the stock portfolio is currently about 5.0%. Happy Easter to the forum community! ![]()

My portfolio is highly concentrated and based on my own views. Over more than 20 years of investing, I have sought my own investment style, and in the last 5+ years, I have found the right one for myself - research, familiarize, and emphasize. The companies that pass my filter “easily” end up in the portfolio with a very large weighting. I have also used leverage for the past 3 years.

In addition to these listed investments, approximately 10% of the portfolio’s total capital is tied up in unlisted companies.

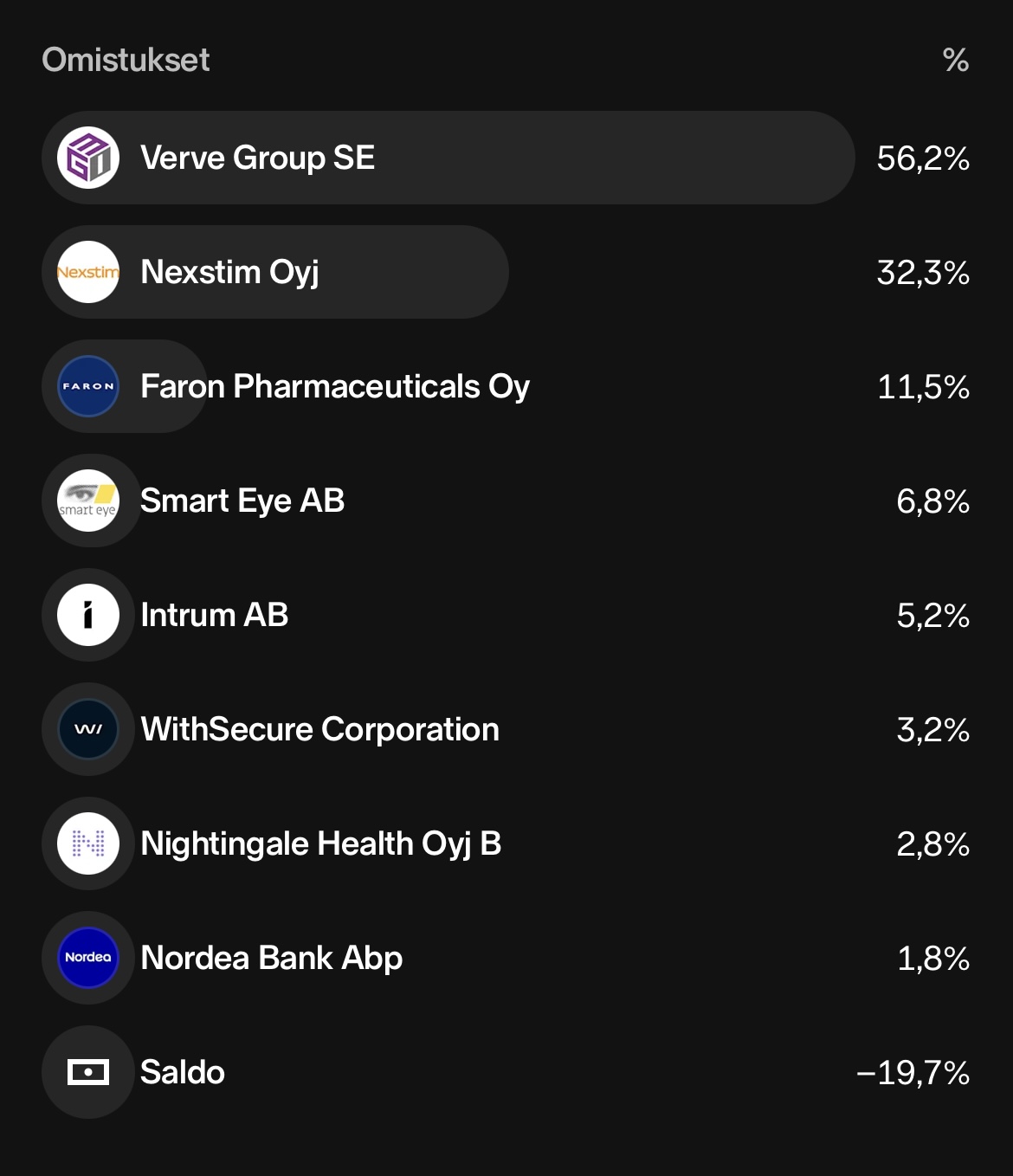

Verve: In my opinion, a ridiculously undervalued company that is unknown to most. Listed on First North in Sweden, the CEO is by far the largest owner and has continuously bought more shares over the years. It is constantly gaining market share from competitors, and the future looks good in terms of growth. It is expected to turn into a cash cow this year, as loans have already been restructured, interest rates are falling, and the business is growing.

Nexstim: A company with truly great potential, whose weighting I have already had to reduce by about 30% from my original ownership. I have strong faith in magnetic stimulation therapies and in Nexstim’s technology being the winning one in this game (e.g., Sinaptica collaboration). I missed the Revenio train back in the day, and I believe this will be Revenio 2.0.

Faron: By far the riskiest stock in the portfolio and with a fairly large weighting. Some shares were bought for the trading portfolio now that a large Hong Kong seller offloaded its ownership (over 3 million shares). Half of the long-term portfolio shares were bought at one euro. I have discussed this actively with my contacts, and they (cancer research experts) have strong faith in it. I admit that my own analysis has not played a strong role in Faron’s case, as it is not my core area of expertise.

Smart Eye: Has long had strong potential that has not materialized. Now, Design wins have also started to materialize into revenue, and the share price is very low compared to before.

Intrum: The debt collection company is undergoing a major transformation into a “capital light” company, where not all non-performing loans are bought onto its own balance sheet anymore. If the restructuring goes through (which I believe it will) and the company regains its profitability, a new flourishing period is ahead. Rubio as CEO has done everything he promised, and I have strong faith in him!

Here is the current portfolio in its entirety. It is known that there are many holdings, which goes against general guidelines. I will not add new holdings even if a new, more appealing target is found.

Sometimes I have had certain principles about where I wouldn’t invest, but after struggling in the investment field for a few years, I’ve had to abandon those principles. The goal, however, is to consistently generate profit while keeping risks under control.

Currently, out of 48 stocks, 33 are in profit and 15 are in loss. Sales losses/gains from past years have also been taken into account. For example, Neste is well in profit after the new company, but due to its history, it is in the loss column. Dividends have also been considered in the calculation, with dividend tax accounted for as an expense.

The portfolio’s P/B is 1.26, where the B-component is calculated using the number of shares at the last financial statement and the current equity. The current share price is used for the P-value. The exchange rates of the dollar, Swedish krona, and Brazilian real against the euro have been taken into account. Therefore, without the recent decline in the dollar, the figure would be lower. For a few cases, half-year report data has had to be used. Efforts have also been made to account for the company’s own shares, different share classes, hybrid bonds, and non-controlling interests in the calculation. The possibility of error exists, but it should be highly accurate.