Medistim has been in the portfolio since the beginning of the year and has been mentioned in previous portfolio reviews

What I believe makes the company very attractive is its recurring revenue. The company sells sensors that can be used 50-100 times depending on the sensor, after which they need to be replaced. Currently, recurring revenue varies between 65-75% of total revenue. Ideally, it would fall below 60%, which in a good scenario would mean that equipment sales are increasing.

It’s also good to note that revenue comes from leased devices sold on a per-operation basis, and Medistim also acts as a distributor in Scandinavia. So the breakdown is not purely equipment / sensor sales.

The company also has two different types of products: flow measurement and imaging. As I understand it, the products are modular, and often a customer might start by purchasing the flow function and later add imaging. In addition, the company has introduced new software to support decision-making in the operating room, which I believe increases competitive advantage and pricing power. This way, they have also been able to tackle the high price, meaning it can be purchased in parts or a leasing agreement can be made.

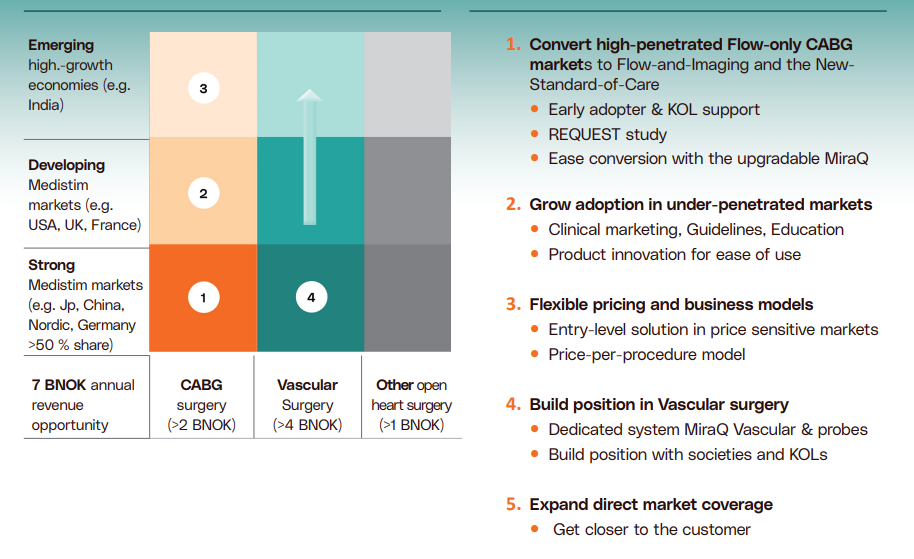

In Q2, an interesting point about M&A was also raised. Management sees better potential in organic growth, for example, by moving to direct sales instead of using a partner.

And there seem to be quite good plans for organic growth.

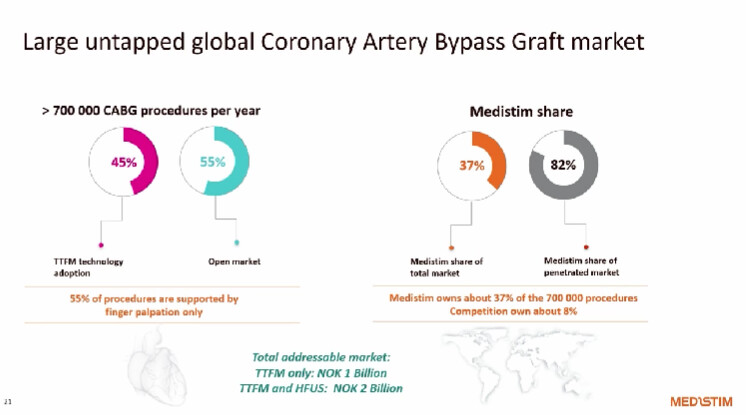

The company has a 37% market share in cardiac, but there is significant potential for growth in vascular.

I am attracted by the company’s pricing power and strong market position. So far, I believe management has navigated the company well, even through a somewhat challenging period, from which there are now indications of recovery.

A few good articles about the company: