Tuomo Vähäpassi defends the necessity of SPACs in Kauppalehti towards the end of the Purmo article:

(Paywall)

According to Vähäpassi (correcting Kauppalehti’s “Vähäpässi” error), there are many companies in Finland that could have significant value creation potential with the support of additional funding, and for which going public through a shell company would be a more sensible process than a traditional IPO.

Is anyone here attending the AGM in person? I’m abroad on a business trip myself and couldn’t quickly find any mention of a remote participation option. I’m mainly interested in the CEO’s review—to see if anything has changed in the talk now that the deadline is so close, or if the same old tape from previous reviews is playing once again.

Swedish peer Creaspac announces that after a 36-month search, it will return money to investors. Despite many negotiations, a suitable acquisition target was not found.

What does that exit actually mean in this context? If a target company is found and it is merged into the SPAC, then the target company’s previous owners’ holdings are converted into SPAC shares. And since these are publicly listed, an exit can be made by selling them on the stock exchange. Or have I somehow understood this whole SPAC setup completely wrong?

A SPAC buys shares from, for example, the founder. The founder receives part cash instead of shares in the new company. At the same time, the pot intended for investments decreases. That’s how I understood it.

Lifeline SPAC I is organizing a Press Conference regarding the Combination today, July 5, 2024, at 1:30 p.m. at Event Studio Eliel in Sanomatalo, located at Töölönlahdenkatu 2, 00100 Helsinki. The event can also be followed via a live webcast.

At the press conference, Lifeline SPAC I’s Chairman of the Board Timo Ahopelto, CEO Tuomo Vähäpassi, and CFO Mikko Vesterinen will present the Combination. Canatu’s CEO Juha Kokkonen will present Canatu’s business operations and background, as well as Canatu’s key figures. The language of the presentation is English.

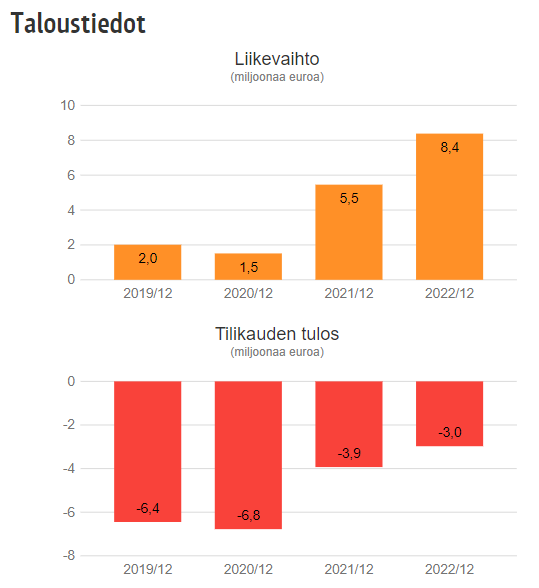

Revenue last year was €13M and the result was slightly in the red. “Performance” from previous years below:

At first glance, a €230M market cap sounds a bit steep. The 2027 target is €100M in revenue and €30M in adjusted operating profit. I don’t understand anything about the technology myself, but in light of the numbers, I’ll leave it to the more eager investors for now.

I’ve been thinking along the same lines myself. Now, in a frantic rush, trying to read up on the company, figuring out if I need to sell something to get cash, or what the deal is.

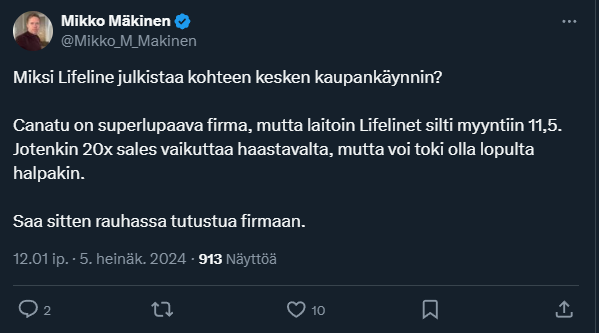

Isn’t that more like 10x sales based on this year’s forecasts, since according to management €10–11.5M has already come in during the early part of the year and the target is €20–25M?

P/S is in the same range as QT’s right now, and the growth is much faster.