VAC Spacin jälkeen seuraavaa pukkaa pörssiin. Teknologia ja kasvu fokuksessa, 70% merkintäsitoumukset kerätty. Lifeline Ventures -osakkaat häärivät taustalla, kuten SPAC:in nimestäkin voi arvella

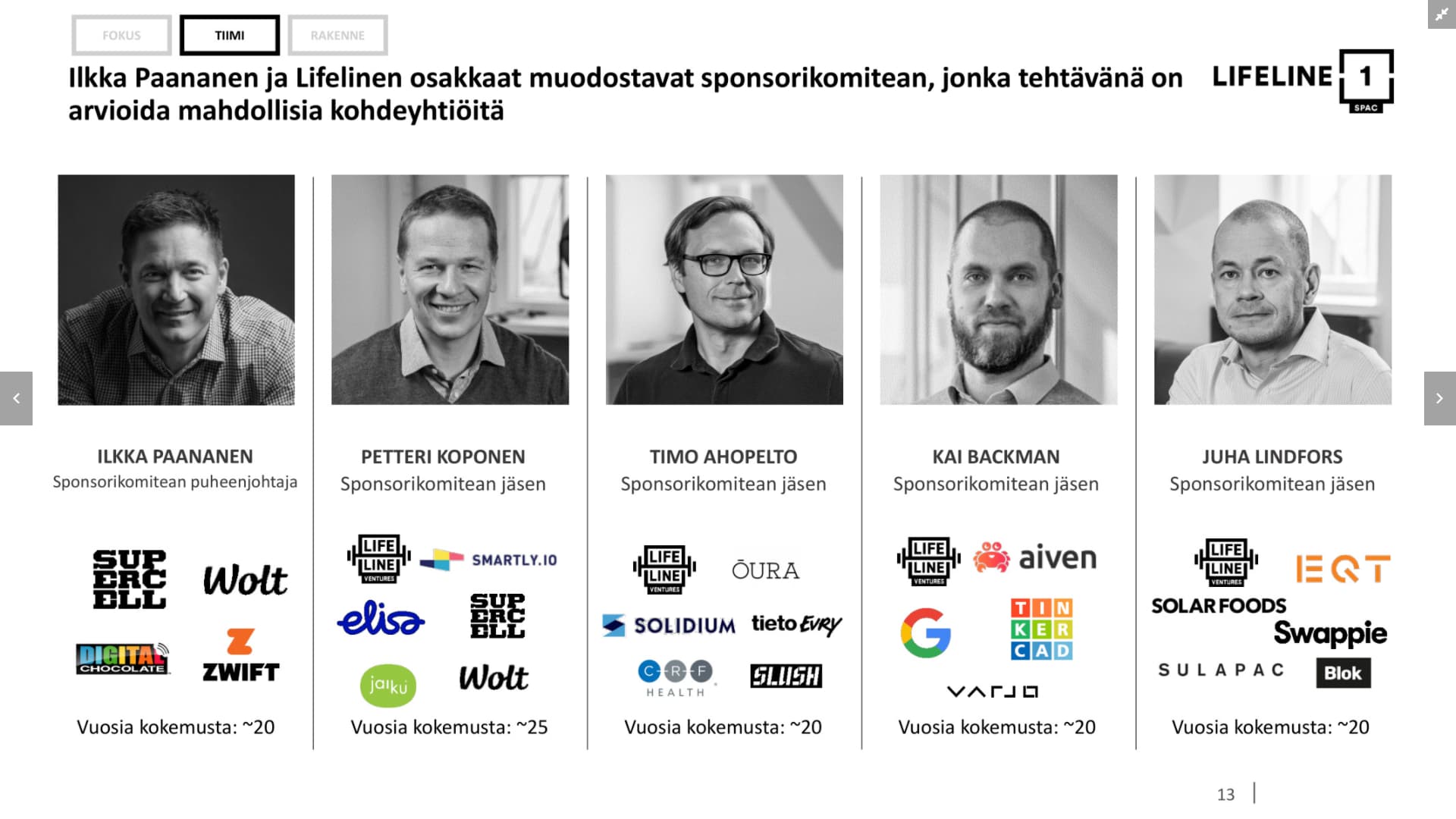

Yhtiön sponsoreina toimivat pääomasijoitusyhtiö Lifeline Venturesin osakkaat,

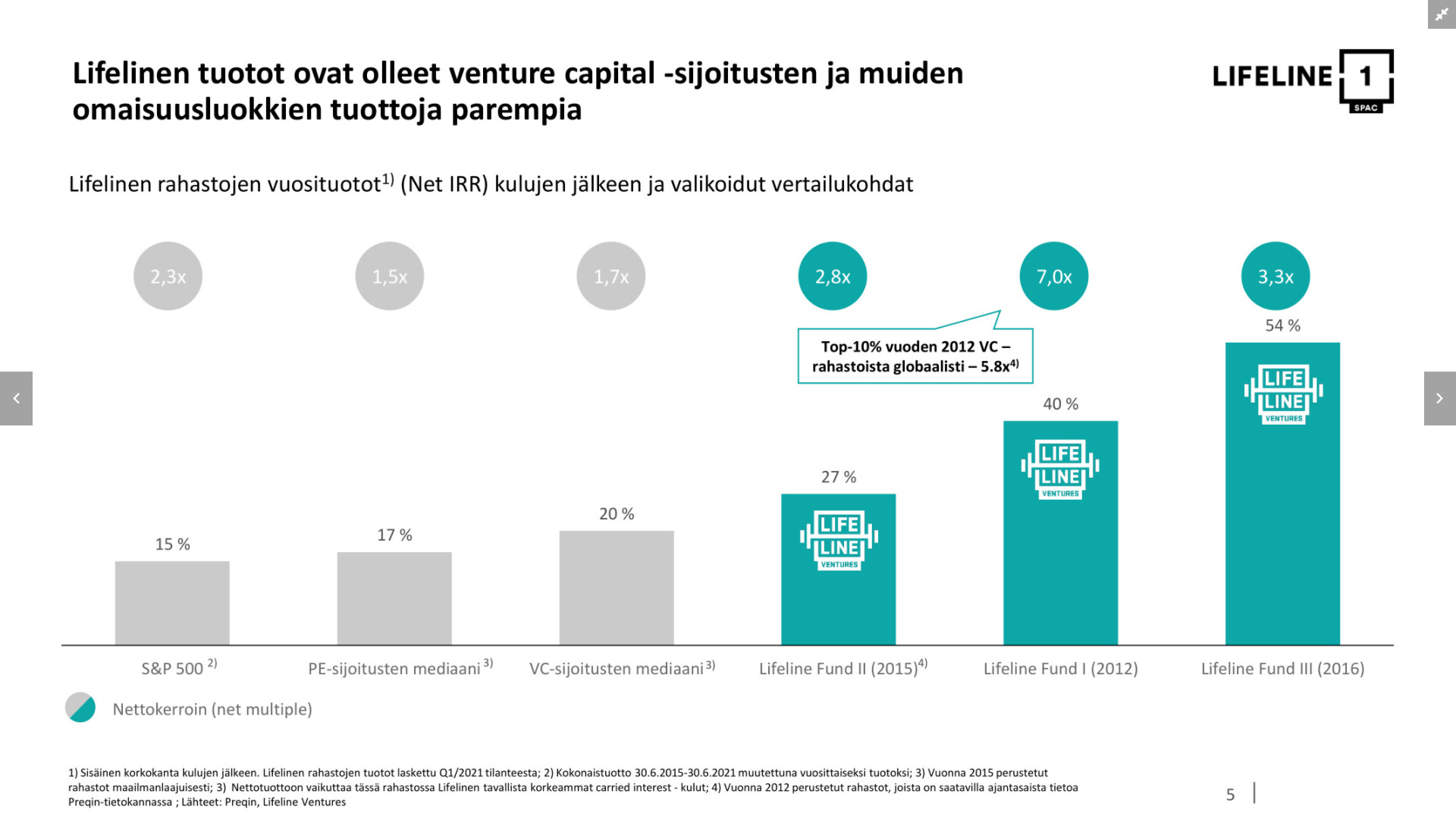

Lifeline SPAC I on vuonna 2021 perustettu osakeyhtiö, jonka ainoana tarkoituksena on kerätä pääomaa Listautumisannilla, listautua Nasdaq Helsingin säännellyn markkinan SPAC-segmentille ja yhdistyä listaamattomaan yritykseen asetetussa 24–36 kuukauden määräajassa.

Ahlström Invest B.V., G.W. Sohlberg Ab, Keskinäinen työeläkevakuutusyhtiö Varma, Mandatum Asset Management Oy, tietyt Sp-Rahastoyhtiö Oy:n hallinnoimat rahastot, Rettig Group Oy Ab, Visio Varainhoito Oy ja tietyt WIP Asset Management Oy:n hallinnoimat varat (yhdessä ”Ankkurisijoittajat”) ovat antaneet Listautumisannissa merkintäsitoumuksia, joiden nojalla ne ovat sitoutuneet tietyin edellytyksin merkitsemään tarjottavia osakkeita yhteensä 68,9 miljoonalla eurolla tarjottavien osakkeiden merkintähintaan. Ankkurisijoittajien merkintäsitoumukset vastaavat 68,9 prosenttia tarjottavista osakkeista olettaen, että Listautumisanti merkitään kokonaan.

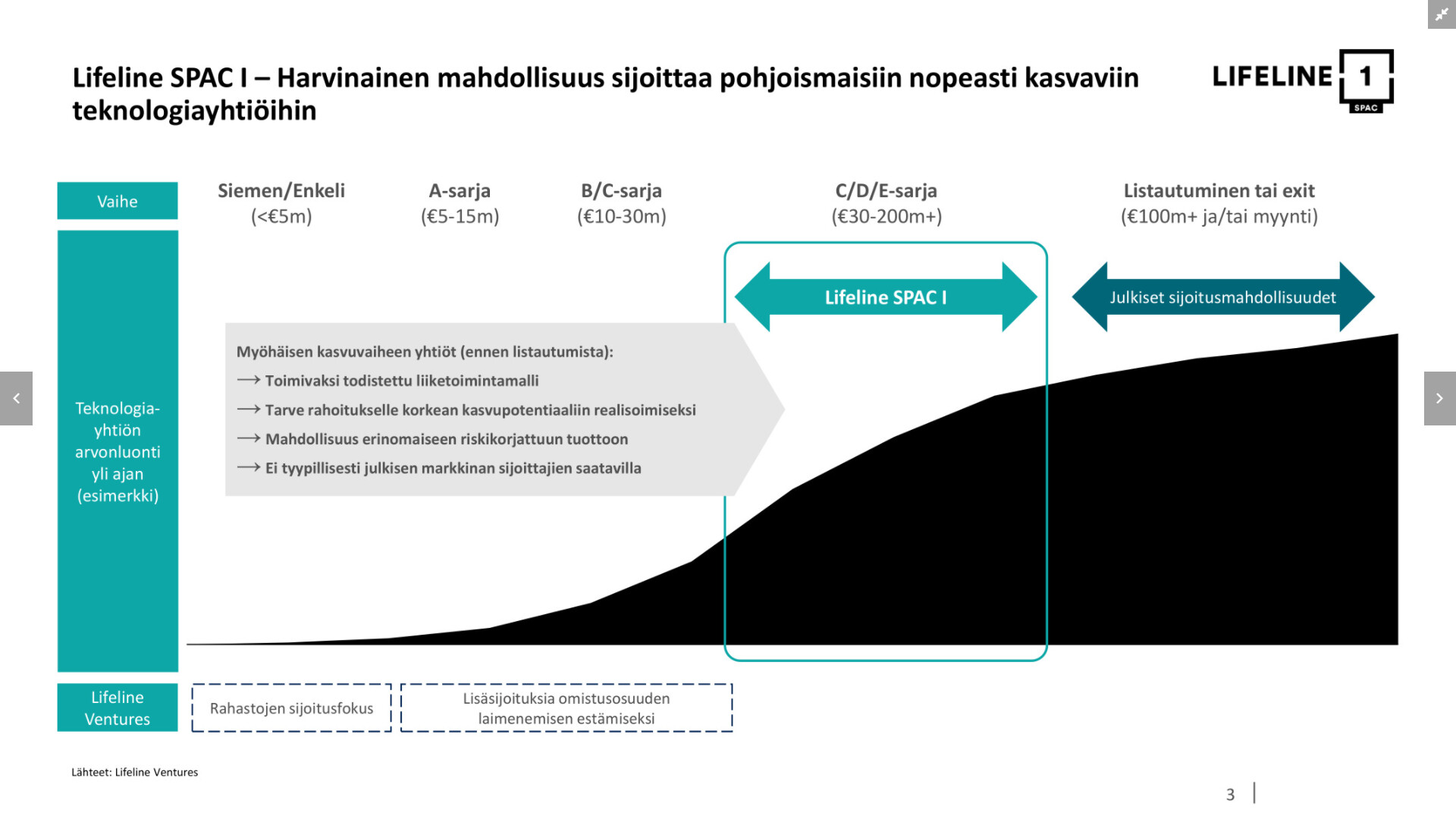

Yhtiön strategiana on ensisijaisesti tunnistaa listaamaton, teknologiasektorilla toimiva korkean kasvupotentiaalin yritys ja yhdistyä sen kanssa. Kohdesegmentteihin kuuluvat esimerkiksi yritysohjelmistot, terveysteknologia, ilmastoteknologia, digitaaliset kuluttajatuotteet ja -palvelut sekä robotiikka ja laitteisto. Nämä teknologiasegmentit ovat globaalisti laajoja, ja niillä on lisäksi erittäin vahvat kasvunäkymät.

Yhtiö pyrkii valitsemaan kohdeyhtiöehdokkaikseen teknologiapainotteisia myöhäisemmän kasvuvaiheen yhtiöitä, joilla on toimivaksi todettu liiketoimintamalli ja jotka tavoittelevat korkeaa kasvua. Esimerkkejä tällaisista ovat muun muassa yhtiöt, jotka pyrkivät lisäämään kasvuaan kehittämällä markkinointiaan tai pyrkivät maantieteelliseen laajentumiseen, pyrkivät laajentamaan tuotekehitystään tai muulla tavalla merkittävästi kasvattamaan toimintaansa. Yhtiön sijoitusstrategian mukaiset kasvuvaiheen yhtiöt vaativat tyypillisesti vielä operatiivista ja muuta kehitystyötä ennen kuin niiden voidaan olettaa tuottavan voittoa sijoittajilleen, mutta korkean riskin vastapainona on tyypillisesti mahdollisuus saavuttaa korkeampia tuottoja pitkällä aikavälillä.

https://www.lifeline-spac1.com/fi/itf-tiedote/

https://www.lifeline-spac1.com/fi/

Lifeline Ventures, sieltä saapi osviittaa mihin tämän SPAC:in taustaihmiset ovat rahaa sijoittaneet

https://www.lifelineventures.com/