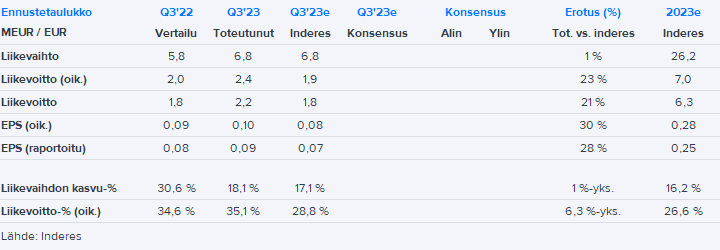

Lemonsoft’s Q3 results clearly exceeded our cautious expectations. Organic revenue growth was -1% in line with our expectations, and revenue from acquisitions was slightly higher than expected. The earnings beat came entirely from the cost side, and the company has clearly maintained strict cost discipline recently. Operating cash flow was significantly weaker than the profit, but according to the company, this was affected by a pricing change during the review period, which caused accounts receivable to increase temporarily. Thus, cash flow should be clearly better again in the future, and the pace of capitalized R&D investments was also slightly slowed down during the quarter from the levels seen earlier in the year.

At first glance, the report leaves a fairly positive feeling compared to the cautious expectations. At 1 p.m., there is the Lemonsoft webcast, and before that, Jan-Erik’s interview will already be recorded for InderesTV.

Yeah, it was a bit annoying to see that KL news story, as the figures were completely off and then they draw entirely wrong conclusions I hope nobody made their investment decisions based on that..

Edit: I also sent them a correction request regarding the matter.

Yes, exactly. These happen a bit too often on the KL forum, and there’s always the danger, of course, that hasty conclusions (sales/purchases) might be made based on incorrect reporting. At least in this instance, those headlines were as botched as they could be…

Atte has written a new company report on Lemonsoft.

The company’s profitability clearly exceeded our cautious expectations, which in part demonstrated the company’s ability to deliver good results even in a weaker market. In the short term, the company’s growth outlook remains uncertain, but with the upgraded earnings forecasts, the stock’s valuation already receives clear support from the current earnings level. Thus, we see the risk/reward ratio as attractive, as in the medium term, we see good potential for the company to accelerate its earnings growth through both a pickup in organic growth and acquisitions.

A press release from Lemonsoft regarding its partnership with FreightOpt. While not significant for the share as a standalone news item, it is a step aligned with the strategy to strengthen the overall offering provided to customers.

“Lemonsoft’s strategy focuses on providing customers with a comprehensive software and service offering, both directly through Lemonsoft and via selected partners in specific areas of expertise. The partnership with FreightOpt brings Lemonsoft a step closer to a comprehensive logistics offering for its manufacturing and wholesale customers. The goal is to begin offering FreightOpt as an integrated solution for Lemonsoft’s ERP customers during the first half of 2024.”

Lemonsoft Oyj | Inside information | 28.03.2024 at 18:36:00 EET

The Board of Directors of Lemonsoft Oyj and CEO Jan-Erik Lindfors have mutually agreed that Lindfors will leave his position as CEO immediately. The Board has initiated a search process for a new CEO.

The Board of Directors of Lemonsoft Oyj has appointed Kari Joki-Hollanti, the founder of Lemonsoft Oyj and the Group’s Chief Development Officer, as interim CEO. He will start in this role immediately. In addition to the interim CEO position, Joki-Hollanti will also continue to perform his duties as Chief Development Officer.

Lemonsoft announced on Thursday that the company’s Board of Directors and CEO Jan-Erik Lindfors have mutually agreed that Lindfors will step down from his position as CEO immediately. The Board has initiated the search process for a new CEO.

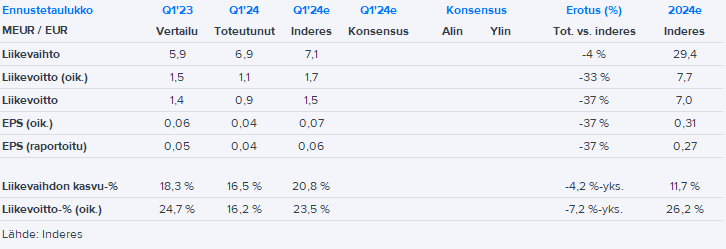

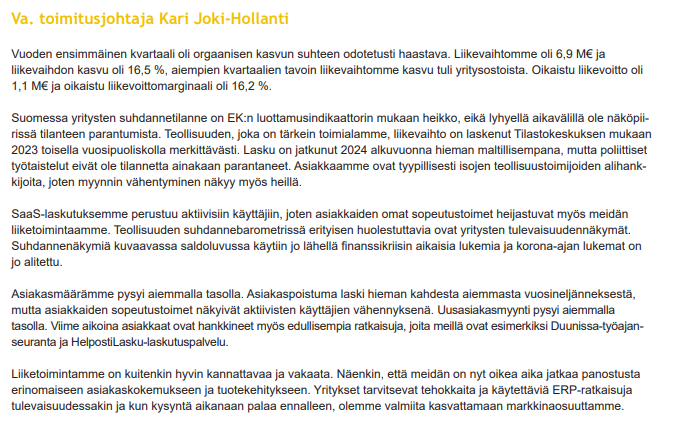

A soft start to the year for Lemonsoft, and the earnings performance for the start of the year fell quite significantly short of our expectations.

Organic growth was negative at -1%, while our expectations were around zero. The impact of the Finvoicer acquisition on growth in the early part of the year was also slightly smaller than our expectations. On the earnings side, the CEO’s termination resulted in additional costs for Q1, but profitability remained somewhat soft in the early part of the year otherwise as well. The weakness of the Finnish economy is currently reflected in Lemonsoft’s customer base, which is detailed in this concise review:

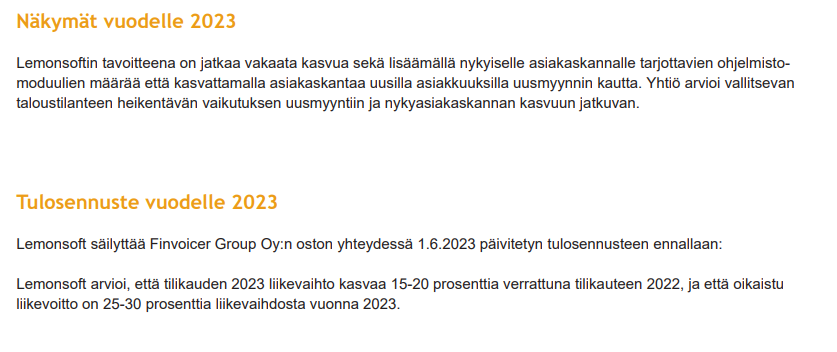

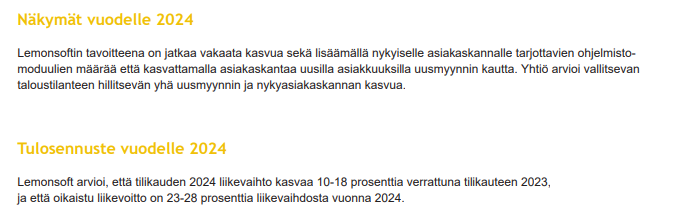

Performance needs to improve towards the end of the year to reach the guidance, which was kept unchanged. Finvoicer will still provide an inorganic boost for Q2, but after that, organic growth should also be accelerated.

@Atte_Riikola has published a new company report on Lemonsoft.

Lemonsoft’s year got off to a soft start, and the unchanged outlook requires a clear pick-up in organic growth toward the end of the year. However, no clear signs of improvement are yet visible in the market situation, so there is a risk of a profit warning for the remainder of the year. The stock’s valuation is not particularly demanding, provided the growth rate picks up in the coming years. In the short term, however, we see the risk/reward ratio as neutral and maintain a wait-and-see stance regarding the stock.

It was also quite a “nice” surprise when I went to the company’s website that day to check the shareholder list; virus warnings started popping up on my phone and the phone froze.

Lemonsoft has apparently been the victim of a data breach. 11 gigabytes have been taken, apparently including, for example, social security numbers. The Data Protection Ombudsman has received over 100 notifications from different companies regarding this matter. Around the 12:30 mark, the discussion on the topic begins: Spotify or episode 71 here: https://tietosuojapodcast.libsyn.com/

Lemonsoft has been in a shopping mood again, and here are Roni’s comments on it.

Lemonsoft announced on Monday that it is acquiring Applirent Oy, a software company specializing in ERP (enterprise resource planning) for the rental industry and equipment management. This is a strategic acquisition that strengthens the product portfolio, through which Lemonsoft expands its offering to companies engaged in the rental business. The transaction is relatively small in size and has no impact on Lemonsoft’s outlook for the current year. It also has no immediate impact on our view of the stock, and we will include this transaction, as well as the recently announced Atmotics Oy acquisition, in our forecasts by the Q2 results at the latest.

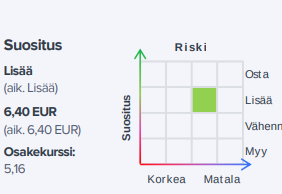

We reiterate our Reduce recommendation for Lemonsoft but revise our target price to EUR 6.4 (prev. EUR 6.0). We have added the small product portfolio-complementing acquisitions made by the company in June-July to our forecasts. In our view, both arrangements look like strategically sound acquisitions, and the reasonable purchase prices paid also provide the conditions for value creation. Looking ahead to next year, the stock’s valuation seems slightly stretched in our opinion, supporting waiting for a better risk/reward ratio.