This sector is one of LeadDesk’s clear strategic customer areas. Of course, the company already has, in my estimation, a reasonable market share in the Nordic public healthcare and social services (Sote) sector relative to its size. LeadDesk has stated that following the Zisson acquisition, it has dozens of public healthcare and social services operators across the Nordics, such as health centers, welfare districts, dental clinics, and ambulance services. Zisson specifically had a significant share of customers in this sector. The core target customers in this sector probably consist of some 50-60+ organizations in the Nordics, plus smaller buyers on top of that. LeadDesk’s position is strong particularly in Norway and Finland, which limits the potential somewhat (meaning Sweden and especially Denmark). In Sweden, more is done in-house with proprietary systems. In Denmark, there would be potential given the current small presence, but it’s difficult to estimate how easy it is to start gaining a larger foothold there.

The HUS contract was in the range of 1.1% of annual revenue, and it is definitely on the larger end, while smaller contracts are around ~0.3% of annual revenue. I can’t give a more precise picture of exactly what might be coming up for tender in the next few years. I would highlight the public healthcare and social services sector as a very significant sector where the risk of disruption is also relatively lower. In my opinion, it is a growth driver, but because of the already reasonable market share, I wouldn’t elevate it to a massive growth driver. Of course, it’s also good to remember that LeadDesk’s business in general is built from relatively small streams.

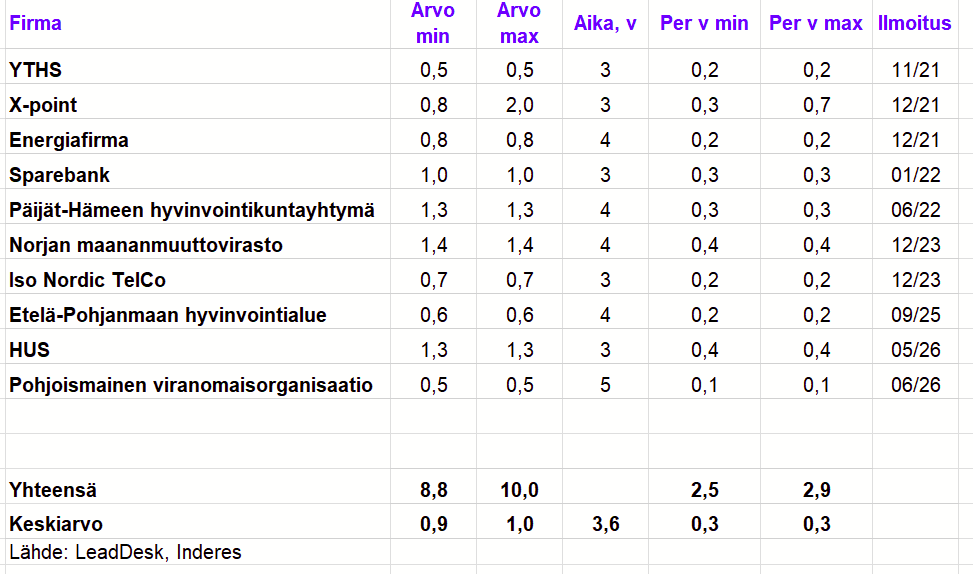

Here are the customer deals announced by LeadDesk in recent years for context.

I will also include a question about this in the next interview.