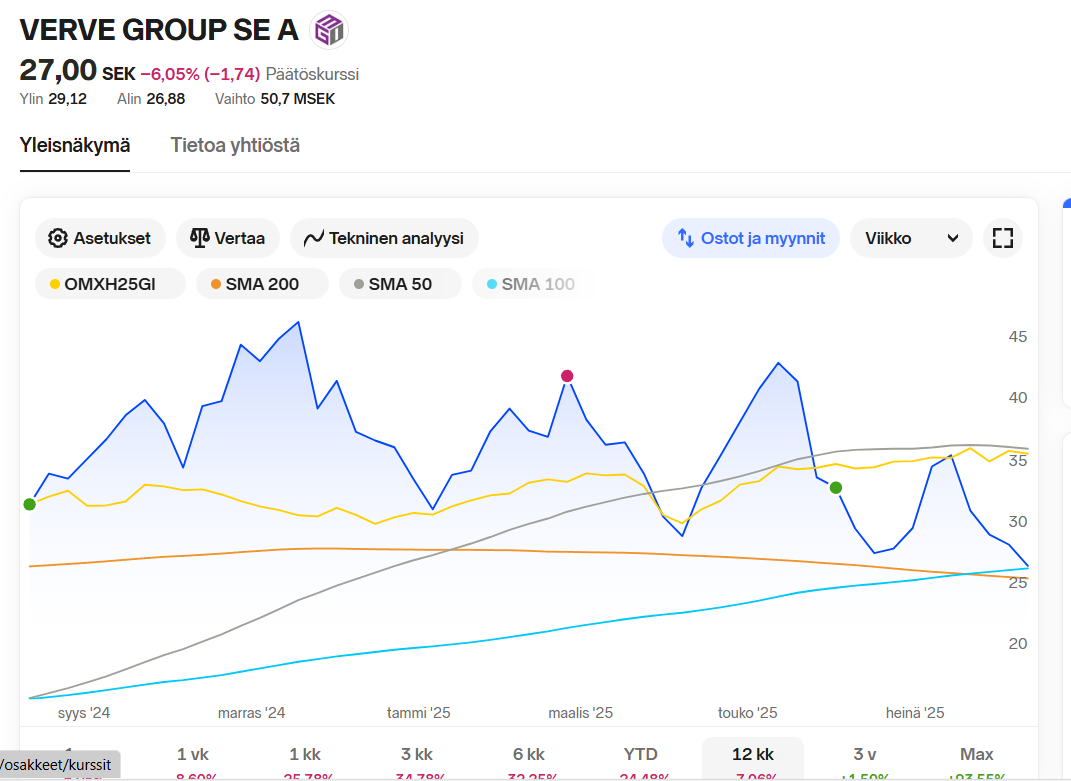

If we again take a look at the famous longer timeframe, then there’s nothing special about this latest decline . Some technical analysis genius could draw some lines and explain why the stock price is going on a rollercoaster ride according to some technical analysis law.

In layman’s terms, this is known as the so-called “EVO” curve, with which some people once made easy money with EVO

The company has been affordable at prices around 45 and ridiculously affordable at these prices starting with two. I don’t know of another excellent company in any stock market that has been so clearly and long-term held as a market’s (in terms of valuation) “spittoon”. Peer companies have reported good Q2 figures, so there’s no reason to assume Verve wouldn’t, at least regarding revenue. Operating profit is another matter, where there is some quarterly fluctuation. Insiders have been continuously accumulating, though not now as the quiet period is on.

Edit. There’s nothing brutal about such a decline . Except perhaps for those paper hands who jumped in as newcomers right at the previous interim peak.

If the rumor turns out to be true, or well, in any case, the shorts were let off the hook incredibly easily. Trading already over 15 million shares when there were 25 million shorts.

Would you perhaps like to buy this $20 bill for $17.50 USD? Oh dear, I would have hoped for a bit of backbone from the sellers.

Edit: the company itself has not commented on the rumors in any way, so this could still turn out to be a hoax.

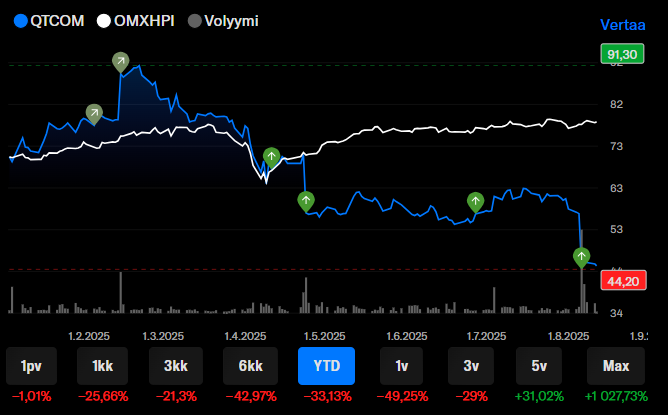

If I had to guess how companies in this sector are doing, I would think they are only going in the other direction. However, I have followed it a bit, but they have still managed to surprise me a little.

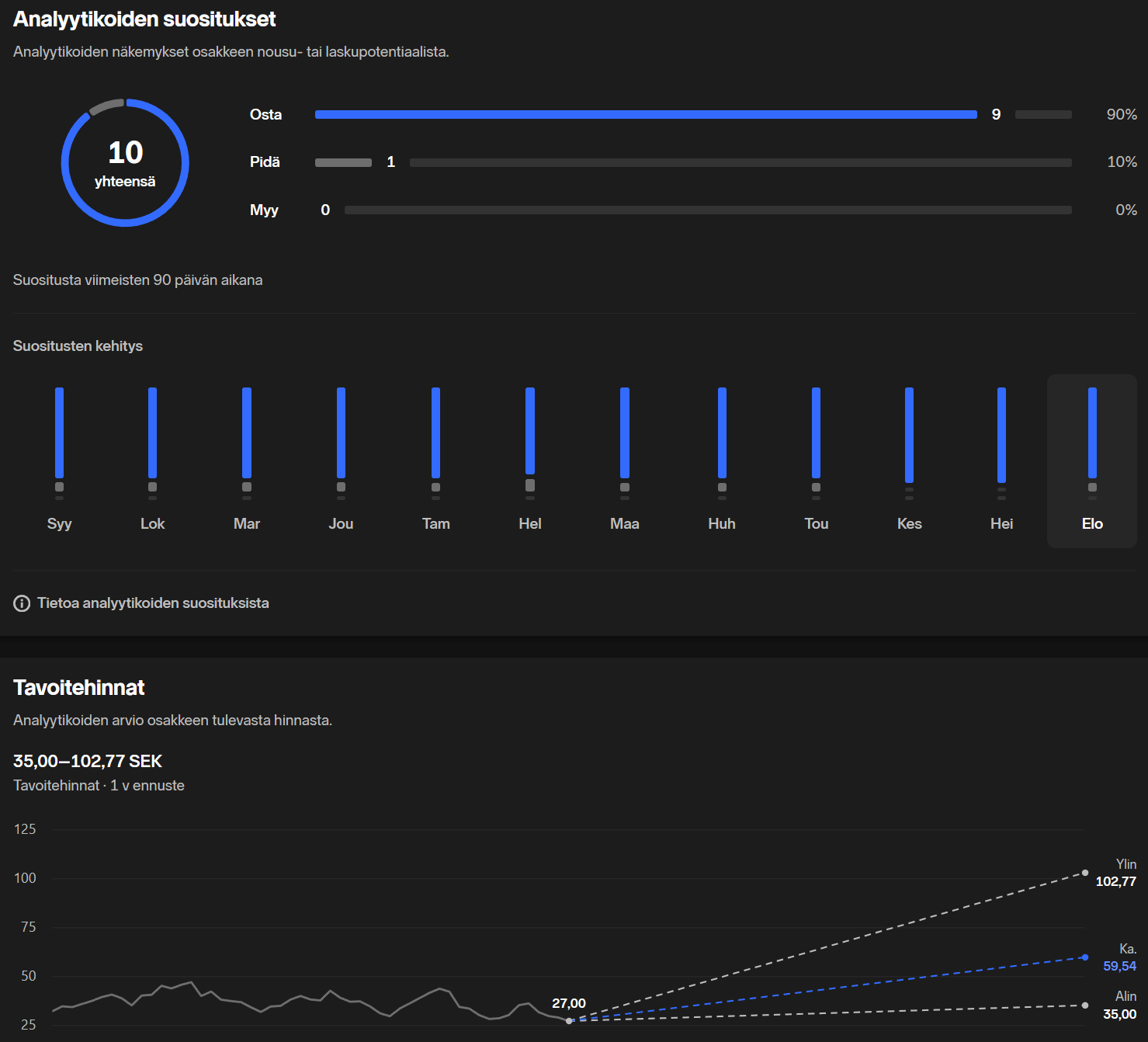

Analysts also seem to be giving BUY recommendations, including Inderes.

I’ve been a bit surprised why this doesn’t appeal to the Red Eye crowd. It’s not found in their top or alternative picks, their fund, or even by the analyst who analyzes the company.

Gartner has now come firmly onto my radar after the biggest dip. I can’t bring myself to believe that artificial intelligence can replace Gartner’s outputs, which are largely based on interviews and surveys, as well as the analysts’ substance in sniffing out things that don’t yet exist in the data utilized by GenAI. In addition, Gartner is a kind of “nobody gets fired for buying IBM” card for management and decision-makers; it’s difficult to make a mistake in the eyes of other decision-makers by acting as Gartner advises, including how to approach AI. On top of these are the valuable conference events, which provide a good reason to go on a business trip with colleagues; these events are perhaps a kind of bubble for a certain group.

Forbes does list other challenges, such as internal culture and sales difficulties, which are harder to assess. However, my finger is on the buy button, waiting for the decline to start turning around; I’m ready to bet that artificial intelligence will not replace Gartner.

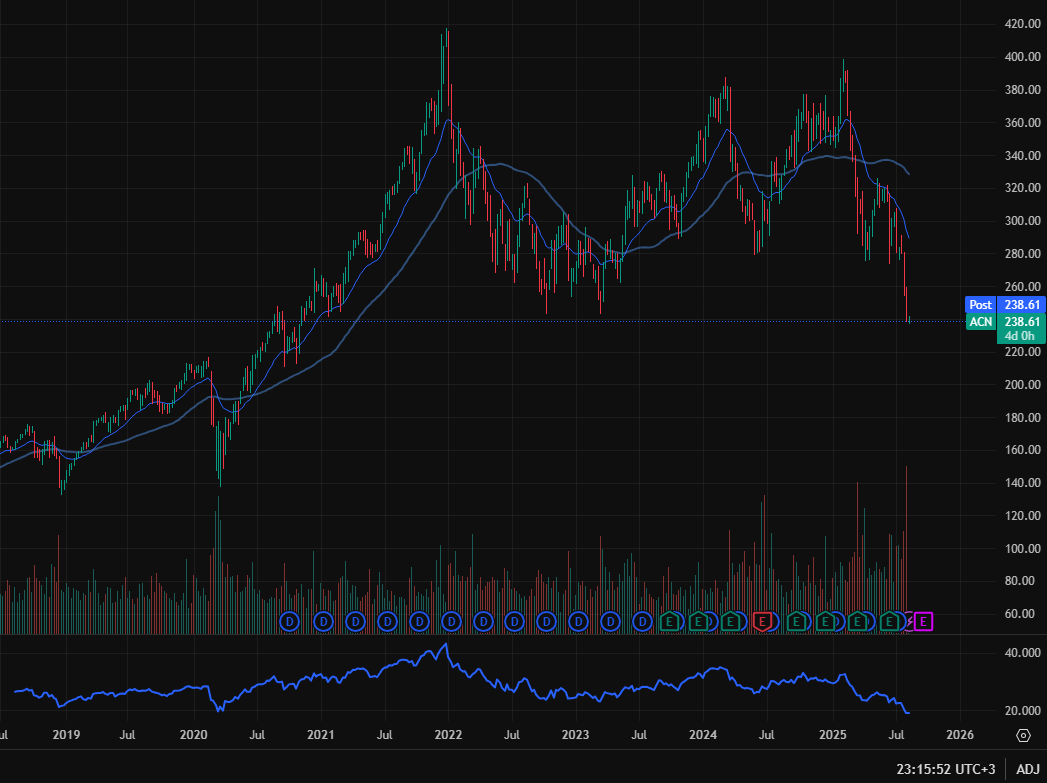

A similar fate has also befallen Accenture and Adobe, apparently due to AI fears. The buy button is itching with these too; I believe Adobe’s services will only improve with the help of artificial intelligence (but so will costs), and Accenture will get to do the same outsourced work as before, but in the best case, will succeed more efficiently. PE ratios have been pulled down to historically low levels.

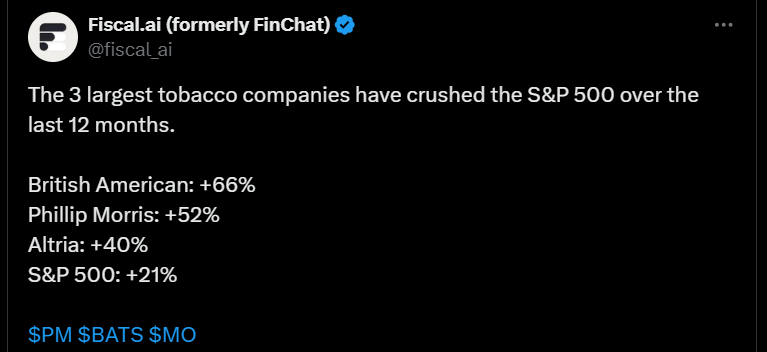

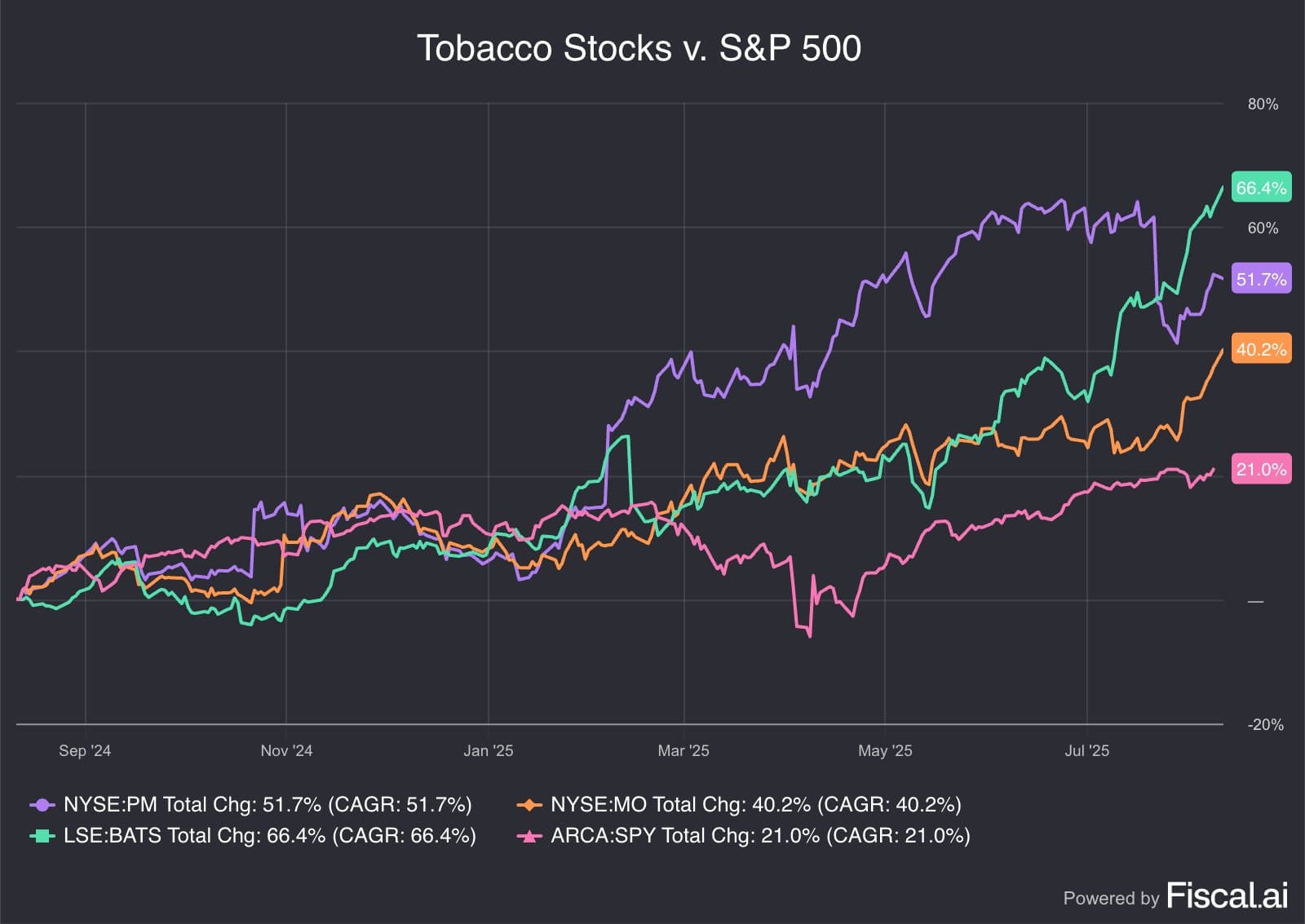

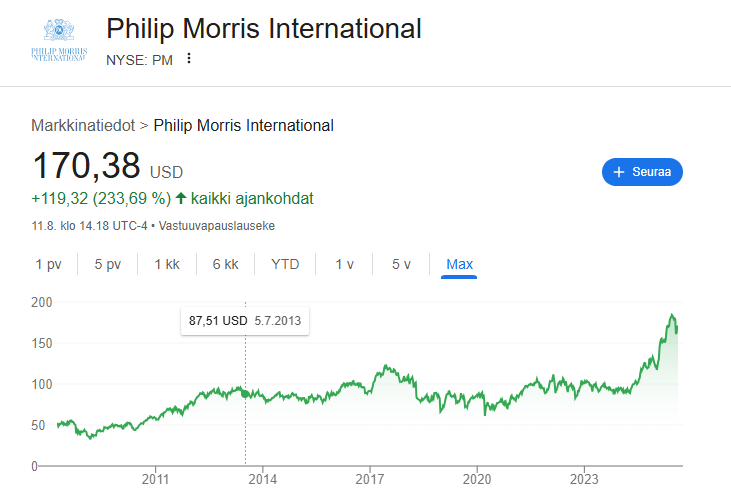

Tobacco companies’ growth nowadays seems to come from products that contain no tobacco at all, i.e., all sorts of nicotine liquids and nicotine pouches. For example, at Philip Morris (found in my portfolio), about ~40% of last year’s revenue already came from these non-tobacco products, and the trend is growing.

The products are fine and literally “addict” their customers.

Even the heaviest regulation can be conveniently circumvented, as long as the product contains nothing related to the tobacco plant. Of course, various countries are now waking up to the fact that these need to be reined in more carefully. Tobacco laws do not directly apply to these.

They are packaging new products for a new generation and pushing the ‘tobacco is dangerous’ agenda, so to speak, on the side of the ‘good guys’. The product is addictive, and a moat can be found in distribution channels and the sale of basic cigarettes. However, it is still a very profitable business that can finance the development of new products and reward owners with dividends and share buybacks.

I would personally take such companies off the stock market if I were the main owner. They have been languishing in the pariah class with low valuations, even though they have risen for about a year now.

It’s worth noting, by the way, that over 36,000 shares appeared on the sell side at 18 euros in the morning auction, so one of the 11 largest owners is likely trying to get rid of a larger quantity. The share price development in the coming months will therefore likely be anemic regardless of the results, unless Inderes pulls some trump card out of its back pocket.

a positive reaction after a shocking report was published. Bullero finds it difficult to understand why Kamux doesn’t stop destroying value in Sweden and Germany. Just an announcement about it would make the stock price jump up properly.

These low-volume stocks in Helsinki are amusing. Roni’s and Petri’s excellent analysis arrives for reading, and the markets have already made their own conclusions, and the target price has already been left behind like a home station for someone who fell asleep on a train. A target price is a target price, and there’s already been enough talk about it and staring at it here. Stock picking for these low-volume stocks certainly requires constant scrutiny. Furthermore, it’s pointless to try to grab any larger position when the liquidity is as thin as a cobweb.

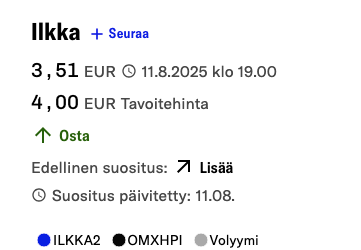

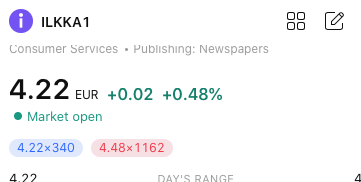

Meanwhile, Ilkka: " hold my beer"

Thanks, getting to know the company is a bit easier again, and my post is slightly more idiotic

TPI Composites has been on a steep decline, especially in recent days. Yesterday, the confirmation of Chapter 11 came, meaning, at least for the current owners, the final nail in the coffin.

I’ve held this pile of junk for about 4.5 years since I spotted it in January 2021 from this Arvopaperi article (paywall).

A few maneuvers along the way have reduced the losses, but I still paid 5-6 thousand euros in tuition fees!