Sellas- and the momentum is accelerating![]()

10 Likes

American Copart has collapsed drastically from its peaks of just over a year ago, from over $63 to today’s approximately $28. Today it’s looking at about an -8% hit as the company announced a CEO change (no specific reason was given). The CEO who previously led the company successfully during times of crisis is making a comeback.

The cycle has been against Copart, as auto insurance companies have been making losses and are now looking for savings. It has been more profitable to repair cars instead of scrapping them, so auction volumes have decreased on Copart’s website. In the midst of a poor cycle, Copart’s main competitor has even managed to gain market share, so the sector’s “biggest and brightest” is now being hit from two fronts.

A general bogeyman for the industry is the future of autonomous cars, which would lead to a decrease in the number of accidents and the volume of total-loss scrap cars potentially collapsing. On the other hand, these cars will contain more sensors and sensitive electronics, so when a crash does occur, will insurance companies be more likely to write them off? Additionally, increasing extreme weather phenomena should ensure that there will be enough car wrecks in the future as well.

Personally, I am interested in Copart’s traditionally excellent net profit margin (which has been around 33%), large cash position, lack of dividends, recent significant share buybacks, and substantial land ownership (a moat, as they own 90% of the land for their scrap yards, with quite low maintenance costs and good locations).

One could guess that the downward trend and volatility will continue at least through July.

30 Likes

Slightly off-topic, but Copart auctioned off our totaled moped for a pittance (a few dozen euros), and if I had bought it back, I would have made a profit by selling the parts. I just didn’t bother to go pick up the wreck for the sake of a few hundred bucks. The company won’t survive with that kind of trading.

4 Likes

I’ve been following this since 400 bucks. I just haven’t bothered to hit the buy button. Instead, I’ve been filling my portfolio with all sorts of “quality goods” from TEMU that no one else seems to be able to sell either ![]()

11 Likes

Maybe it didn’t count as news today ![]()

![]()

Scanfil supports TOMRA in the roll-out of the Polish deposit return system

Scanfil has played a key role in scaling up the production and implementation of TOMRA’s reverse vending machines for the Polish deposit return system (DRS).

6 Likes

I was looking at my notes, and the (Finnish) portfolio was up a total of +44.71% on January 18, 2024. Now that same portfolio is +25% without any major changes, so there’s still no reason to cry too much…

Kemira and Terveystalo are weighing the most into the red, and I haven’t added to these positions lately.

Edit: meaning we are only talking about the portfolio performance, not realized profits

4 Likes

Robotics and automation are likely among the most significant sectors whose growth prospects will improve substantially with AI development over the coming years, and this development is only going to accelerate. In recent days, companies linked to robotics have gained momentum in the US, and many stocks appear to be forming a bottom.

I believe the sector will grow over the next few years, offering excellent investment opportunities. Personally, I am also particularly interested in the industry’s supply chains—from magnet companies and bearings to “pick and shovel” manufacturers, such as our own Incap, which could well benefit from future growth in robotics and especially the automation industry in both the industrial and defense sectors.

I have been collecting robotics-related stocks on my watchlist since last autumn and intend to delve deeper into them over the next few months. The trend is only in its early stages, but I believe growth will accelerate forcefully within a couple of years, and there could very well be a few so-called “tenbaggers” on the list. Several stocks from the list are already in my portfolio, although I haven’t built a clear robotics tilt yet. Attached are the watchlists—please feel free to suggest if anything interesting is missing.

I think there should be, but I’m pressed for time. I was surprised that a clear thread touching on this topic hadn’t been created already. If someone starts a thread, feel free to copy my lists.

46 Likes

Agreed. I just have no clue about the industry, I know Tesla! Shouldn’t a dedicated thread be started for this topic?

3 Likes

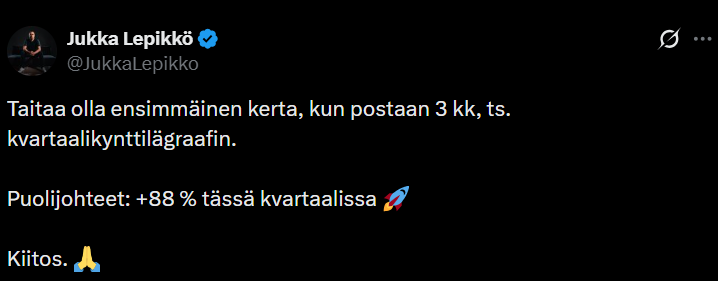

Jukka Lepikkö, semiconductors and the three-month candle ![]()

https://x.com/JukkaLepikko/status/2072059960389738782

7 Likes

Coffee is mooning!

Luckily, I have enough hoarded coffee from sales left in the cupboard that I can consider myself to be long.

31 Likes

We have been more so waiting for the price of the pack

to drop in Finland. In Sweden, you can get coffee for half the price compared to Finland.

12 Likes

On the rise again, though with a small turnover of about 5,250 euros. ![]()

![]()

7 Likes

The star performer Revenio continues its journey downwards. A few years ago, I was looking to snap up Revenio at the €15 price point. It didn’t quite hit that and instead bounced about 2x higher, only to return much lower than where I originally thought of jumping in. Now that time has passed, Revenio doesn’t look as attractive to my eye at the current lower price as it would have been picked up from the previous bottoms at €15 (had it ever dipped there). Now, I’ve had to adjust my target buy price to below €10. On the other hand, there are so many attractive cases everywhere that I wouldn’t necessarily put my next stake in Revenio even if I could get it for €9. There are targets to be found that are, in my opinion, much more reasonably priced. However, as others rise and Revenio falls, the situation may change…

Some arrangements/splits etc. have certainly been made in the past and the chart likely doesn’t give the right picture, but as a final lighthearted remark, there seems to be a nice gap to be closed around €0.23.

5 Likes

The bogeyman is likely the upcoming share issue in the autumn. The purpose is apparently to raise another €80m for an acquisition. This would mean a 25-30% dilution at a price of €12 per share.

But how much of that share issue is already priced into the current stock price?

2 Likes

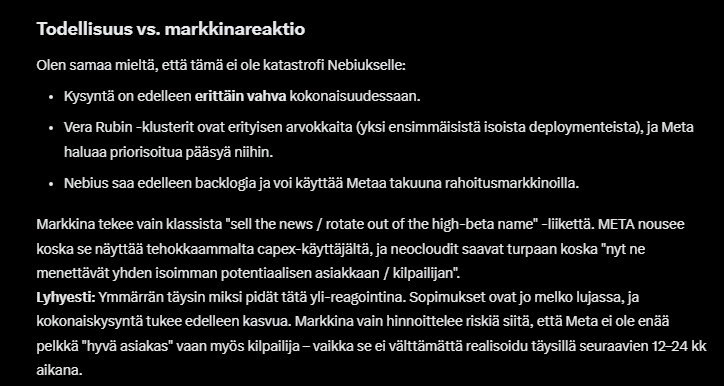

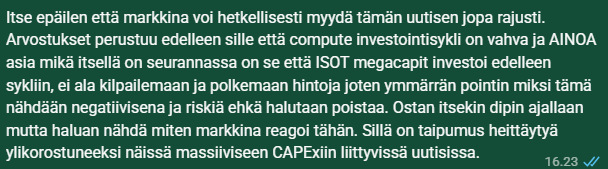

If anyone is wondering about the sudden big -16% dip in NBIS today, here is the reason. The market (NBIS owners) does not want a new competitor selling compute on the market, especially one that is a major part of the CAPEX cycle and a large customer of Nebius regarding excess compute. META therefore intends to sell its surplus compute and will then be a direct competitor to MSFT (Azure) and AMAZON (AWS), as well as Nebius and other neoclouds.

I had a long conversation with an AI about this immediately after the news broke. Meta jumped about +6%, while others fell at the same time. Here is part of that conversation.

’

The cornerstone of the entire AI cycle is that the massive CAPEX cycle continues and the mega-caps finance the cycle. That is why the market doesn’t like it at all if there are even hints that the cycle could be ending/fading. I have personally highlighted that the CAPEX cycle has been one of the most important reasons for me to stay strongly long in AI stocks, and I believe this is also the case for the big players. Any uncertainty immediately causes rising volatility.

27 Likes

dLocal up about +11% today. It has seen a brisk rally recently, up 36% from the May lows.

One explanation for today’s jump would be UBS’s price target hike:

Investing.com - UBS upgraded DLocal Limited (NASDAQ:DLO) to Buy from Neutral on Wednesday and raised its price target to $20.00 from $16.00.

The firm cited a combination of strong growth trajectory, improving operating leverage and potential for re-rating as market confidence rises following a series of solid results. The company’s momentum is reflected in its impressive 56% revenue growth over the last twelve months, reaching $1.21 billion. Growth is expected to be supported by increasing global digitalization and lower e-commerce penetration in emerging markets, expansion into new geographies and deeper client relationships leading to higher share of wallet.

5 Likes