I don’t have quite that sharp a top tier in my own portfolio, but by holding the likes of Admicom, Easoria, Evolution, Qt, Harvia, Smart Eye, and Talenom, I’ve still managed to reach some quite respectable loss figures during the start of the year.

6 Likes

Safe haven Pallas Air rocketed +13.79% on a down day. AI and robot hype is starting to show in the share price.

Trading volume was a staggering €66.

P.S. Contains sarcasm.

17 Likes

Good heavens, what a rocket, I’m going to have to trim even more soon! ![]()

3 Likes

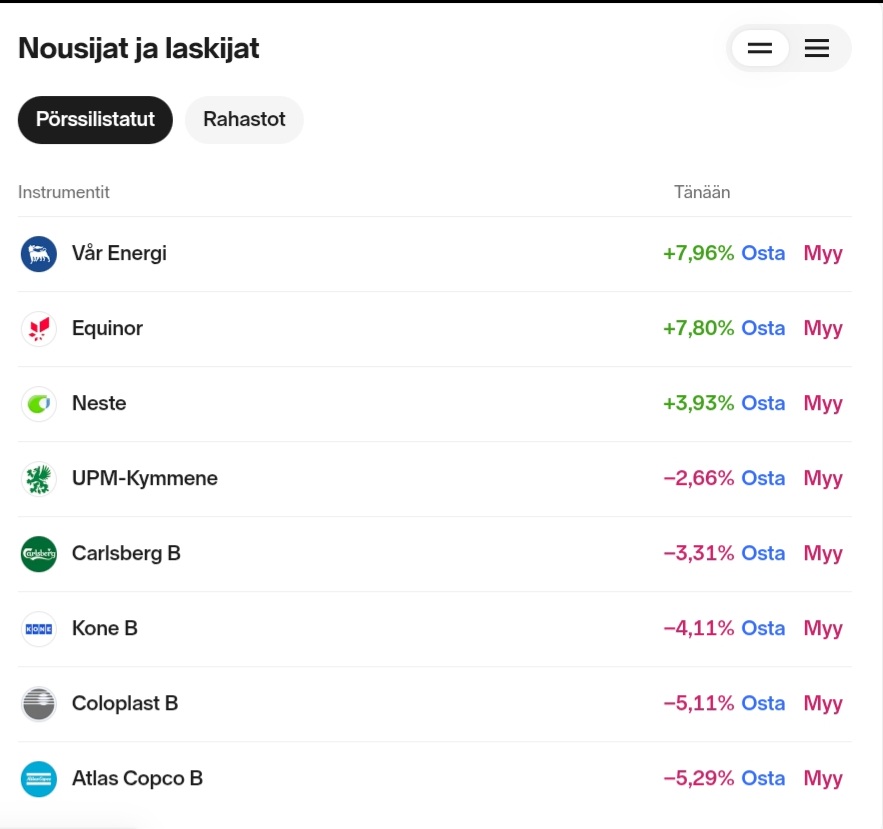

Energy is booming, other sectors are in steep decline. I’ve been looking at additions to Atlas Copco and Coloplast, and from Finland, Vaisala would be of interest.

4 Likes

Luckily, I didn’t get too arrogant:

Even with small percentages, a fall from a great height is still a lot.

e:

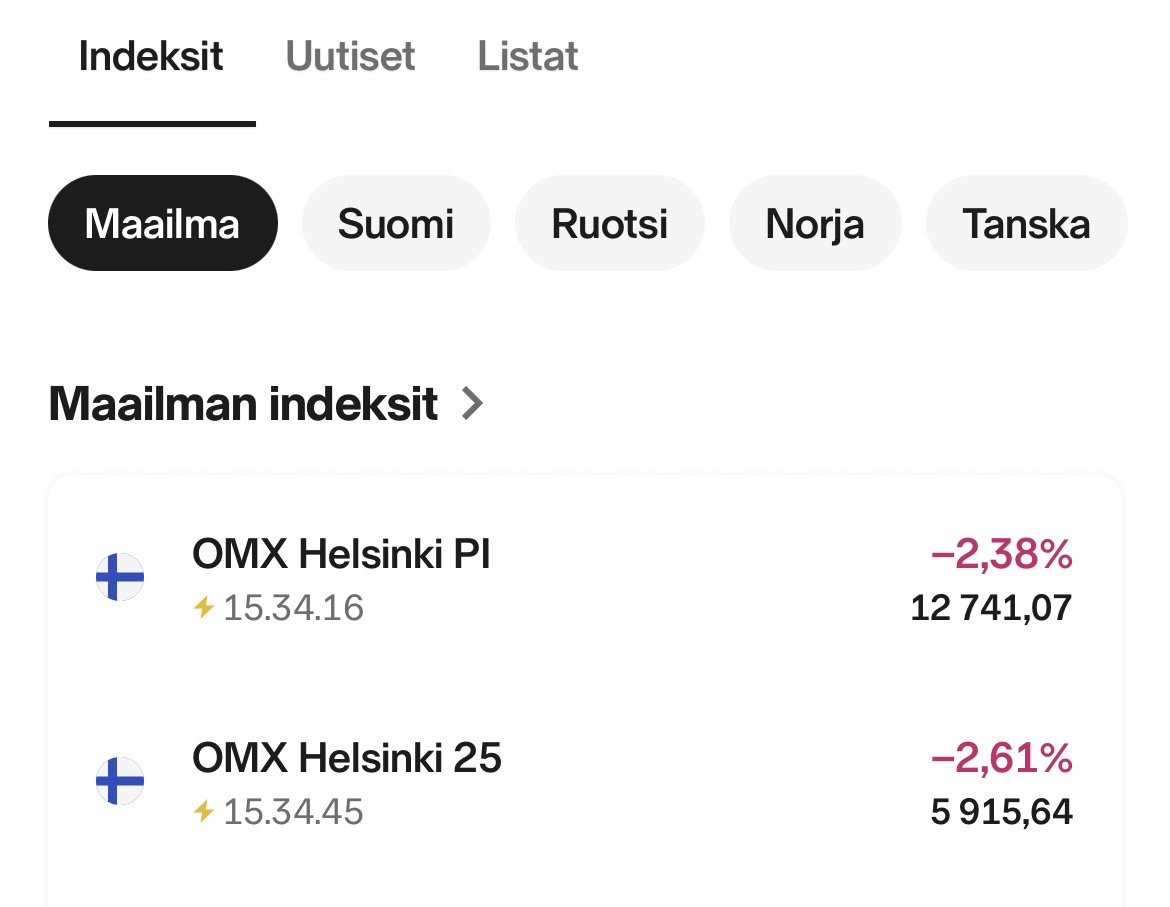

The topography is quite something everywhere right now. ![]()

4 Likes

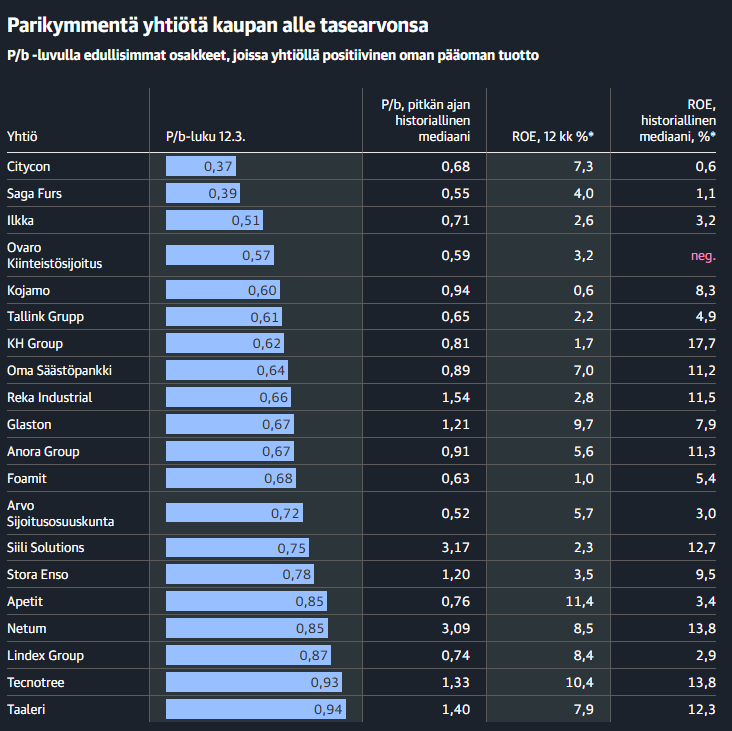

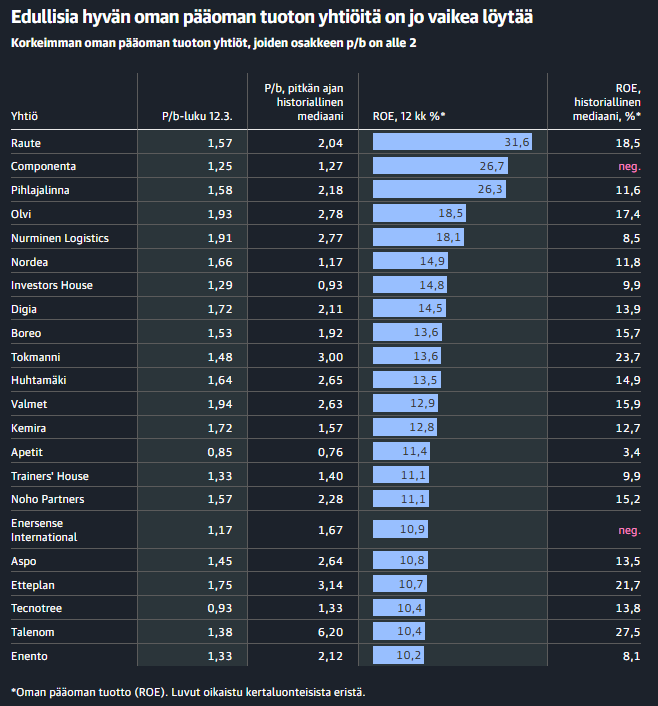

Kauppalehti, as is its custom, reminds us that there are several Finnish companies trading below their book value, perhaps some for good reason.

Companies that appear cheap when measured by return on equity are listed below. In a weak market, discount tags are being slapped on thinly traded stocks quite rapidly. Of course, there might be “slight” uncertainty regarding quality and growth prospects at the moment.

14 Likes

There is currently no doubt about the strongest player in the GPU and AI Cloud sector. The lower-than-inflation interest rates on convertible bonds and the Nvidia collaboration were strong indicators that institutions are interested in Nebius.

17 Likes

After pre-market jitters, the stock’s reaction once actual trading began has been positive. At least one company in the portfolio is in the green on a day like this - at least for now. ![]()

8 Likes

Add a ruler analysis to that, and we’ll get an estimate of the company’s remaining lifespan. Two or three years? I’ve always been amazed how anyone can earn a single penny with these dividend-free schemes.

3 Likes

30 Likes

7 Likes

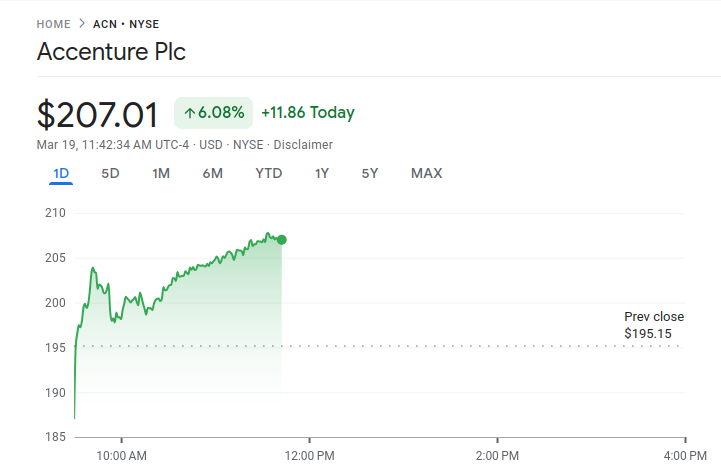

This got me thinking. Dispelling doubts from investors’ minds can take a long time, even years. This doesn’t only apply to Accenture, but to the entire IT services/consulting/software sector right now. The suspicion has been thrown out that artificial intelligence, agents, anti-gravity second brain bumtsibums, and what not (development is progressing rapidly) will disrupt everything.

Companies in these sectors naturally deny this (executives are paid for it), and even the good numbers from several companies in recent quarters have not fully convinced investors. The problem is also that no company’s current value is based on one quarter’s results. For an investor to get their money out of a company with a ~10% required rate of return, cash flows still need to come in, preferably at a growing pace, for 30-50 years. If something increases its capabilities 10x in a few years, no matter how small a threat it is today, it will become an enormous threat within 5-10 years.

Even in a good scenario (where disruption proves to be milder than feared), it may take time for the evidence to be convincing, even if companies adapt. For example, it often takes a while to recover from short attacks, even if the company ultimately has a clean slate. Of the companies I follow, for example, Axos Financial (formerly Bofi) fell victim to Hindenburg in 2015. The bank’s stock only properly surpassed those levels after 2018. In contrast, router company Ubiquiti recovered from similar treatment within six months during 2017.

24 Likes

Sivers Semiconductors -20% today. Let’s see if my timing for buys and sells was successful. I bought on Tuesday, sold yesterday, and bought back today.

On X, Serenity highlighted this as an undervalued company:

https://x.com/aleabitoreddit/status/2033466880661606646?s=20

2 Likes

One of Super Micro’s (SMCI) founders arrested, reportedly sold a small number of chips to China.

The stock price will not like this.

10 Likes

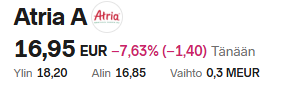

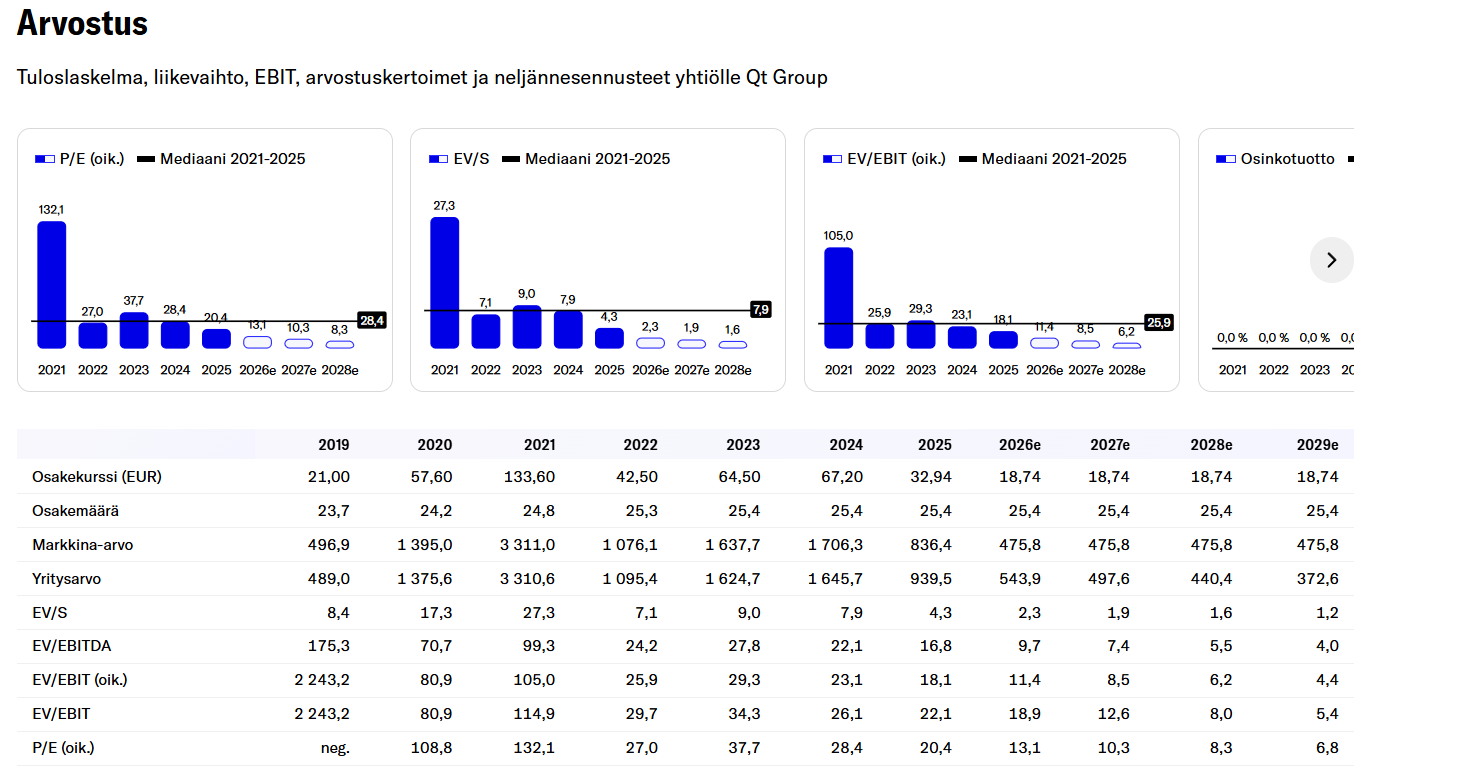

How low will Qt Group’s valuation go? What are your thoughts: is it starting to be “clown-level” (ridiculous)?

22 Likes

I don’t know about that, but it still doesn’t appeal to insiders. So why not?

27 Likes

With dramatically falling earnings, the P/E is only 27. Sounds like a joke.

2 Likes

It’s worth noting in your comment that QT’s depreciations are practically purely goodwill depreciations resulting from acquisitions, which are not made in IFRS accounting. So, if you look at the earnings estimates of Inderes and other analysts, these goodwill depreciations are adjusted out. For example, EBIT (adj) is practically EBITA, and EPS (adj) is earnings per share without these goodwill depreciations. So, it’s not very sensible to look at reported EPS.

8 Likes

Well, I suspect that the actual realized P/E at the current price would be higher than our bullish analyst’s forecast P/E of 27. However, there seems to be a valid reason for the adjustment. The adjusted P/E, with my own (perhaps even too) pessimistic forecasts, is 18-19. Maybe this could be a joke level, but not a trash company level, which would be around €10-12. In my calculations, roughly €1 = P/E 1, €2 = P/E 2, etc.

The best guess is that reality will fall somewhere between these two forecasts, but I prefer to forecast a bit cautiously myself.

5 Likes